At sub two percent on the ten-year treasury, many investors are questioning why bother owning bonds at all. As ninety percent of the returns are derived from the starting interest rate, it’s fair to assume that bonds will indeed offer measly returns going forward.

While it’s not realistic to expect the returns of the last thirty years to continue, I still see great merit to holding bonds in a diversified portfolio. The strongest argument I see is that bonds should provide dry powder not if, but when stocks see their next serious decline.

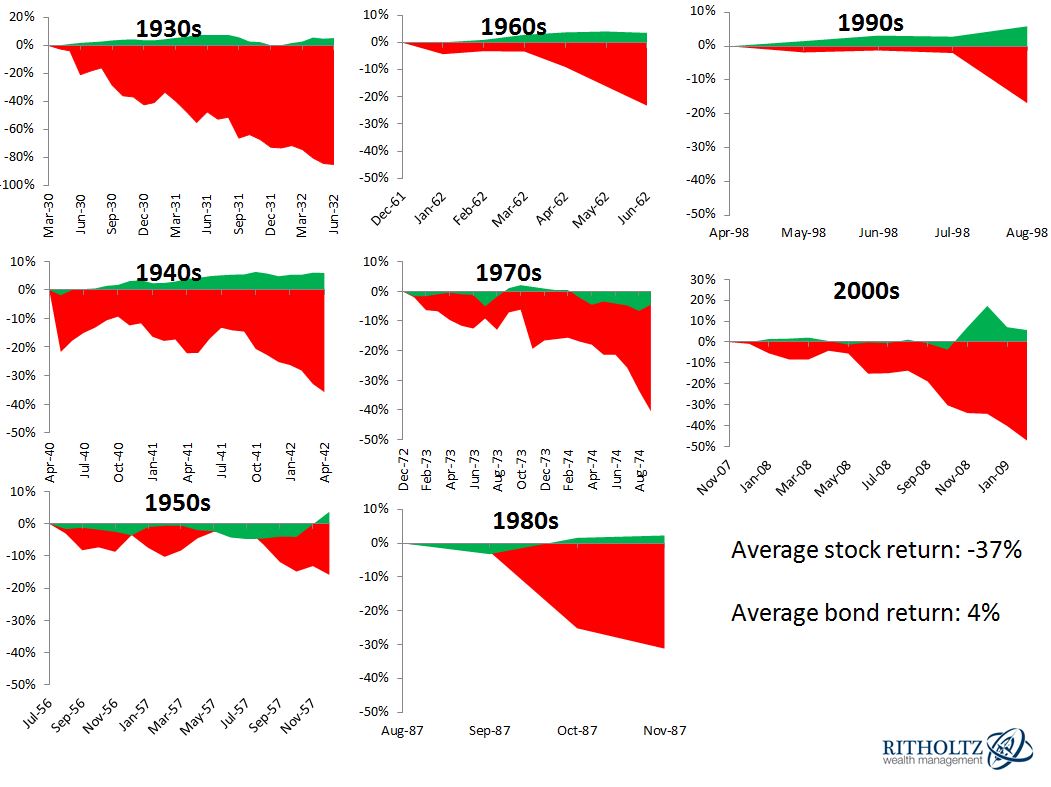

In a post last week, I reviewed the biggest drawdowns for the Dow in each of the previous eleven decades. Taking this a step further, I want to incorporate how *bonds performed during these selloffs. Below in red are the drawdowns stocks experienced and green represents the returns for bonds during that time. The average stock drawdown was -37%. Over that same period, the average return for bonds was 4%. The 1970s were the only decade where bonds did not deliver a positive return (real bond returns were significantly worse).

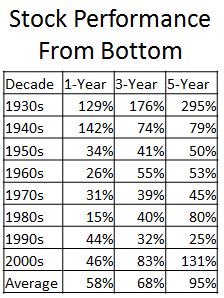

Not only did bonds provide some stability while stocks fell, but more importantly, they provided investors with dry powder to rebalance into stocks as they went on sale. Look at the table below, which shows 1, 3 and 5-year returns following the bottom of the worst drawdowns of the last eight decades. These declines proved to be a gift from god for people that were able to take advantage of them.

Finally, while there is certainly a risk that bonds deliver lousy returns going forward, I view the chances of significant nominal drawdowns as pretty far down the list of concerns, regardless of what the Fed does. Even as the ten-year yield soared to 15% in 1981, the nominal drawdown was just 16%. To put this into perspective, the Dow has fallen sixteen percent in just a month ten different times.

Like literally every other asset class, there are risks worth considering for bonds. However, when weighed against the potential reward, I believe bonds are critical to the long-term success of a diversified portfolio.

*Bonds are a portfolio consisting of the following :(data provided by DFA’s Returns 2.0)

One-Month US Treasury Bills (7.5%)

Five-Year US Treasury Notes (12.5%)

Long-Term Corporate Bonds (30%)

Long-Term Government Bonds (50%)

[…] Why invest at bonds at these interest rate levels? (Irrelevant Investor) […]

[…] Why you can’t really give up on bonds. (theirrelevantinvestor.wordpress) […]

[…] About Individual Bonds vs. Bond Funds (A Wealth of Common Sense) see also Dry Powder (Irrelevant Investor) • Why Uber Has To Start Using Self-Driving Cars (Climateer Investing) see also Tesla’s […]

If dry powder is important, isn’t then the question bonds vs. cash? Why am I in bonds, which have the associated risk/downside, when I could be in cash (short term instruments, whatever) without that downside? The marginal benefit of bonds vs. cash is so small, at current yields, that one can argue it just isn’t worth it. Sure, yields can go lower, providing upside on the bonds, but that is a different thesis/strategy vs. having dry powder. The option/opportunity cost for dry powder (bonds vs. cash) is extremely cheap – with that said, it has been cheap for quite some time, and could stay cheap for much longer, BUT, one who exercises that option has left very little on the table, certainly nothing material in terms of financial security/wealth.

[…] Dry Powder (theirrelevantinvestor.wordpress) […]