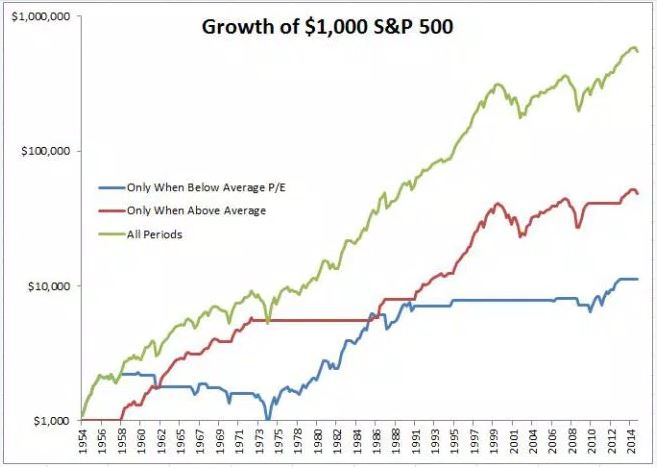

Last week I asked the question “what if you only invested in stocks when they were cheap?” The chart below got a lot of scrutiny, understandably so. It’s hard to believe that stocks did better when they were above their average valuation versus when they were below. I’m happy to chow on some crow here, the chart below is indeed greatly flawed.

I think the message I was trying to convey got lost in translation, so I wanted to take the opportunity to address this. First of all, that was certainly not a strategy recommendation. I was really targeting the laymen who gets frightened out of stocks when they hear people saying “stocks are overvalued.” That post was not intended to be an exhaustive study on valuations, but I’ll take responsibility for the lazy analysis.

In this post I’m going to address where the previous one fell short. This is going, deeper than I usually do, but I want to right these wrongs one by one and see if I can do a little better than last time.

“Wait a minute, why would you use price-to-earnings?”

I used price-to-earnings, guilty. I should have used the CAPE ratio which is much less noisy and a better representation of the overall trend.

“Wait a minute, why did this data only go back to 1954”?

I wasn’t attempting to be manipulative, this is how far back the P/E goes on Bloomberg. The CAPE ratio goes back much further and as previously mentioned, should have been used in the first place.

“Wait a minute, the investor went to cash when they were not invested in stocks?”

This absolutely should have been invested in fixed income rather than just sitting in cash. I replaced cash with the Five-Year U.S. Treasury note. Below, the blue line shows an investor who bought the S&P 500 when the CAPE ratio was below its long-term average and bought Treasurys when it was above average. The red line shows the opposite.

“Wait a minute, how would the investor know what the CAPE ratio would be next month?”

He wouldn’t. So the above chart is flawed, suffering from a severe case of look ahead bias. I have to say, I was surprised at how different the results are once I corrected for that. In the chart below, “below average” compounded at 9.2%, while “above average” compounded at just 6%.

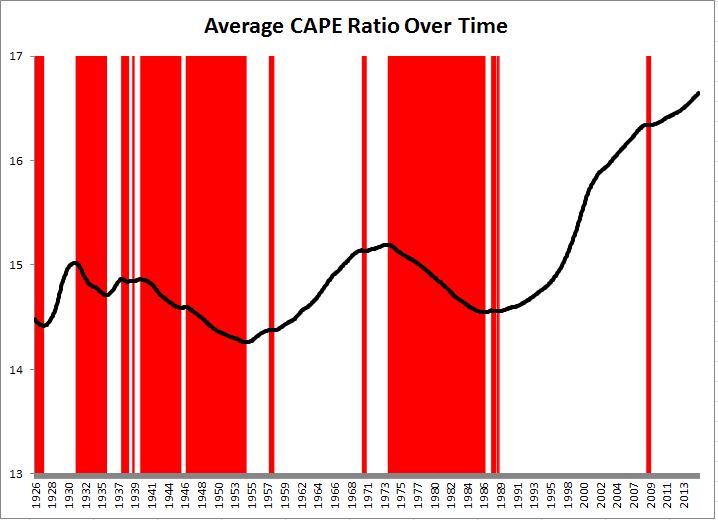

“Wait a minute, how would an investor in 1926 know the long term average CAPE ratio from 1926-today?”

Ah, they wouldn’t, so we have to adjust for that also. Here is the average CAPE ratio over time. The red shaded areas indicate when the CAPE ratio was below its average. It’s easy now to look back at the historical long term average with perfect clarity, but an investor using this in real time did not have that luxury.

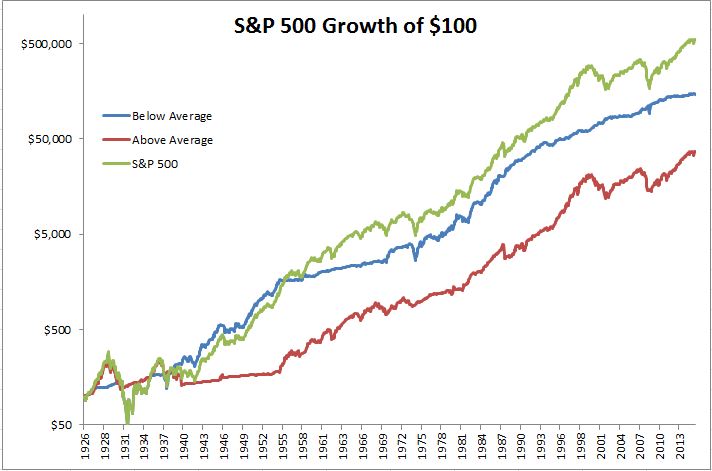

Below is the final version, hopefully absent of any obvious flaws besides the usuals (nobody has a 100 year time horizon, index funds didn’t exist in 1930, taxes, etc). If an investor were to buy stocks when they were below the CAPE ratio and shift into U.S. Treasurys when the stocks were above the average CAPE ratio, they would have earned 8.4% a year, whereas investing in stocks when they were above the CAPE ratio would have returned just 6.8% a year. You’ll notice that an investor buying stocks below the average CAPE ratio in real time actually did worse than if they had known the full historical average ahead of time.

“Wait a minute, is it possible to actually invest based on the CAPE ratio?”

To each his own, but this to me seems like a difficult proposition. While it’s true that owning stocks when they were below the average CAPE outperformed stocks when they were above average, both considerably underperformed a simple buy and hold strategy. Consider that for the last twenty years, stocks have been in the most expensive quintile 75% of the time and have gained ~445% over this period (Granted we did see two 50% drawdowns over this time). Furthermore, the last time the S&P 500 was in the cheapest quintile of valuations was 1985. I’m not sure anybody has the patience, discipline, or quite frankly the need to buy stocks only when they’re dirt cheap. AQR nails it here when talking about market-timing using the CAPE ratio.

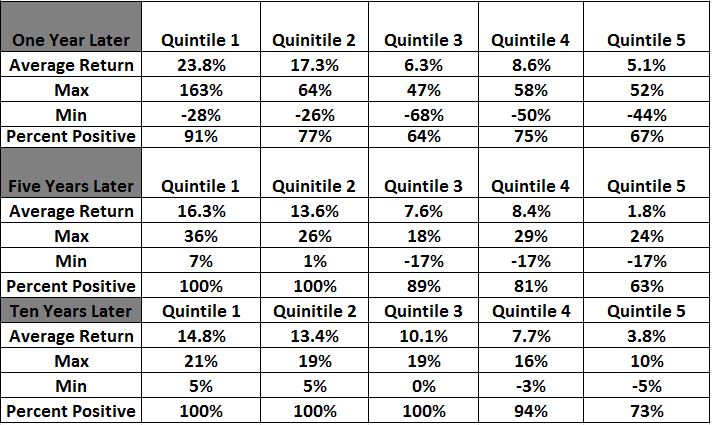

“Wait a minute, just because stocks are above or below their long-term average does not make them expensive or cheap”

Correct, so lets look at returns broken down by quintiles. I don’t think this table is a giant revelation, but in case there was any doubt, stocks have performed significantly better after they’ve gotten really cheap. Today, unfortunately we are in the most expensive quintile. Fortunately, this does not mean that stocks are doomed.

In looking at this valuation stuff, you can venture down a bottomless pit. The point I was and am trying to make is that while valuation is an important driver of long-term returns, using it as the sole basis for your investments might not be the best long-term strategy.

This is interesting stuff. Props to you for acknowledging the limitations of the original post and coming back for another look at it. Good work and thank you.