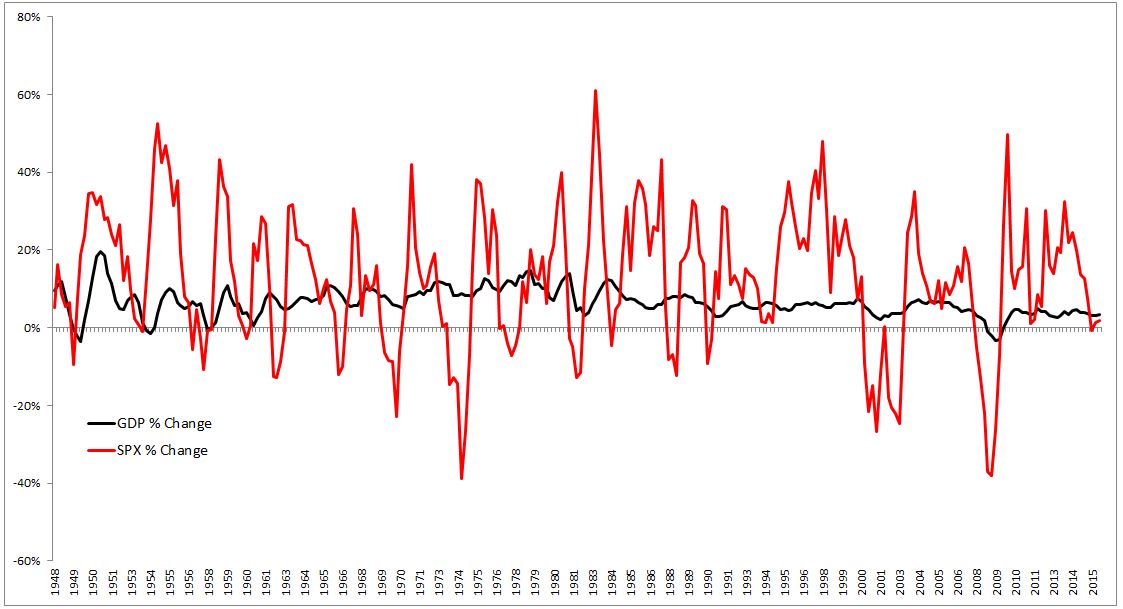

For the first time ever (going back to 1948), U.S. GDP has failed to grow at least 5% following a recession. And although everyone would prefer higher growth, the encouraging news for investors is that changes in GDP have little do with stock market returns. This surprises most people, but when you think about what drives stocks (earnings) and how much they make up of overall GDP (10%) it starts to make a little more sense.

The lack of correlation between GDP and stock returns is not only true in the United States. From 1995-2009, emerging markets grew nearly twice as fast as the U.S. Yet over this time, the S&P 500 returned 219% while MSCI Emerging Markets returned just 189%.

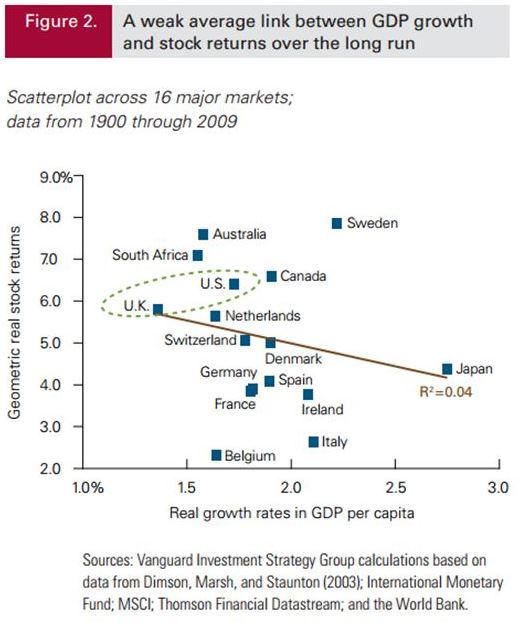

The image below shows the weak relationship between GDP growth and stock returns across 16 major markets, with an R-squared of just 0.04.

Below you’ll see that stocks are way, way more volatile than GDP. The standard deviation of U.S. GDP is 3.5%, while the standard deviation of the S&P 500 is 17.2%.

The worst y/o/y percent change for GDP (nominal) going back to 1948 is -3.5%. Looking at quarterly y/o/y changes on the S&P 500, stocks fell more than -3.5% change 46 different times, or 16% of all 273 observations. So if stocks can fall much farther than the change in GDP, it stands to reason that they can rise much farther as well.

Michael Batnick is a managing partner at Ritholtz Wealth Management. He is the co-host of Animal Spirits, What Are Your Thoughts, and The Compound and Friends. For disclosure information please see here.

Get a Full Investor Curriculum: Join The Book List

Every month you'll receive 3-4 book suggestions--chosen by hand from more than 1,000 books. You'll also receive an extensive curriculum (books, articles, papers, videos) in PDF form right away.