The Great Northern Expedition was one of the largest exploration endeavors in human history. The grueling state sponsored trip, which lasted ten long years (1733-1743) and covered thousands of miles, cost one-sixth the annual income of Russia.

During this campaign, the St.Peter, led by Danish cartographer Vitus Bering, was shipwrecked on what would later be known as Bering Island. With resources running low, the men set out to find food, which was relatively easy at first. In The Island of the Blue Foxes, Stephen Bown wrote:

The men would sneak up on sleeping or unsuspecting animals, pounce upon them, and club them…Soon the otters became attuned to this new predator, man, and became wary of approaching humans. The easy hunting of the early days soon became very challenging. The men had to organize nocturnal scouting expeditions even through ferocious and unpredictable snowstorms to get close enough to attack beached otters. Before the year was over, they had to hike four to six miles to get enough food, and by February 1742 they had to hike as far as twenty miles down the beach.

What once was easy turned into something quite difficult.

Daryl Morey, General Manager of the Houston Rockets was ahead of the curve when it came to assembling an NBA roster. Using quantitative analysis before it was popular, he developed methods that went beyond just eyeballs and gut. He had an edge to approaching the draft, but edges are ephemeral when money and survival are on the line. In The Undoing Project, Michael Lewis wrote

He could even pinpoint the moment when he felt, for the first time, imitated. It was during the 2012 draft, when the players were picked in almost the exact same order the Rockets ranked them. “It’s going straight down our list,” said Morey. “The league was seeing things the same way.”

Eric Rosenfeld, an LTCM trader, once said “We’d go to put on a trade, but when we started to nibble the opportunity would vanish.” Long-Term Capital Management built models that didn’t account for their own existence. And the models worked great for a while, until their billions of dollars beamed a giant light on this market inefficiency. As Benoit Mandelbrot once said, “The trend has vanished, killed by its own discovery.”

Easy pickings don’t last very long in life, in sports, or markets.

Ben Graham liked buying stocks that were selling for less than one-third their net working capital. This simple but effective style of value investing worked in the 1930s and 1940s and for a while after that. But then it got harder as competition moved in.

In the 1950s, Alfred Winslow Jones would go long a basket of cheap stocks and short a basket of expensive stocks. And this too worked well for a while, but then it got harder as competition moved in.

Most of the hedge fund titans came into the business in the late 70s or early 80s, when nobody wanted stocks. They weren’t exactly shooting fish in a barrel, but there was much less competition than there is today. Not to take anything away from Paul Tudor Jones, but the stuff he was doing in his early years wouldn’t work in today’s league. According to the SEC, there are over 9,000 hedge funds that collectively manage $3.6 trillion. The easy pickings disappeared a long time ago.

In the fall of 2017, more than 120 hedge funds had sprung up solely focused on crypto currencies. Today, the easy pickings come and go at light speed, and the big money has to constantly find different competitive advantages to stay ahead of the pack. This is why alternative data has become such a big business. Harvard isn’t building almond farms because they think it will outperform cashews, they’re doing it because what used to work for them stopped working a long time ago. Competition has pushed them way out on the esoteric curve.

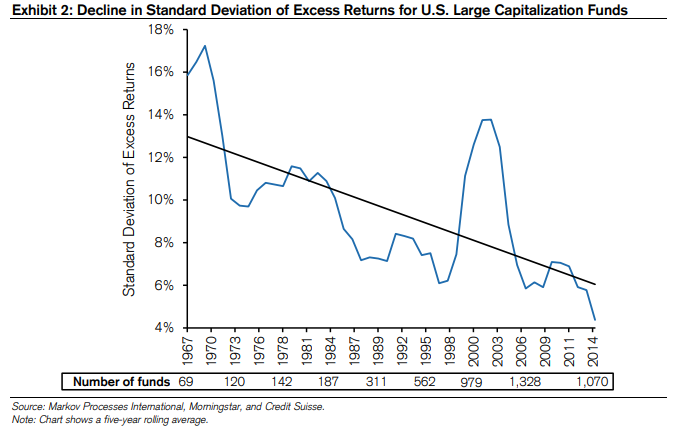

It’s not that the talent inside hedge funds and college endowments has declined, in fact, they have the exact opposite problem. They’re too smart and there are too many of them. Michael Mauboussin calls this the paradox of skill, which says that as skill increases, luck becomes more important in shaping results. One of the best ways to visualize the increasing competition is by looking at the standard deviation of excess returns for U.S. large cap funds.

As retail investors have become less active, there is less amateur money to pick off, and the only ones left at the table are the ones using satellite images and high-speed computers. And the results haven’t been pretty. From ZeroHedge.

For much of 2017, hedge funds – most of which again underperformed both their benchmark and the broader market – complained that they were not generating alpha for one reason: there was no volatility. Well, they got their wish in spades last month when after months of record low, single-digit VIX, equity vol exploded 47% resulting in a 3.9% slide in the S&P 500 and as 10-year yields backed up to 2.86%.

And so with volatility spiking, and what every commentator saying it was a “stockpicker’s market” hedge funds surely had a blockbuster month, right?

Well, no, quite the opposite in fact because according to the Bloomberg Hedge Fund database, in February hedge funds posted an overall drop of 2.19%, wiping out all of January’s gains, and leaving them flat for the year. Yes, somehow the month that all hedge funds were waiting for lead to widescale losses and last month ended up being the worst month for hedge funds since January 2016, when they slumped 2.57%.

The smartest investors have to scrape and claw for the ephemeral edges. The rest of us, who have no business playing this game, would be wise to go the other direction. Do less. You’re not going to achieve excess returns by reducing portfolio turnover, but while Harvard is planting almonds and Renaissance Technologies is doing god knows what, the rest of us can do just fine by chasing patience, an edge that can never be arbed away.

Source:

Hedge Fund Suffer Worst Month Since January 2016, Greenlight Dead Last