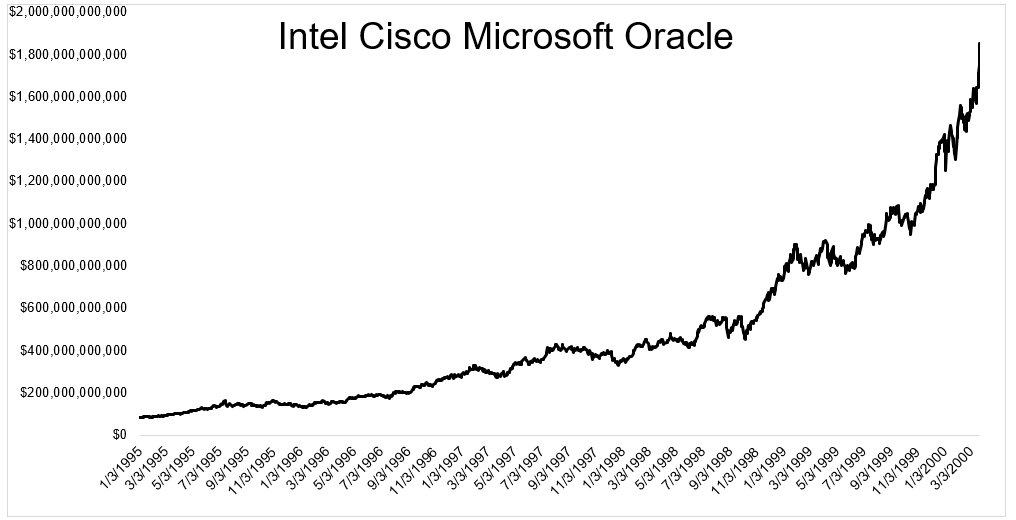

In the beginning of 1995 Intel, Cisco, Microsoft, and Oracle, were worth a combined $83 billion. One giant bubble and five years later, they had grown to $1.85 trillion. As a group, these four stocks gained 2150% over this time, or 80% a year.

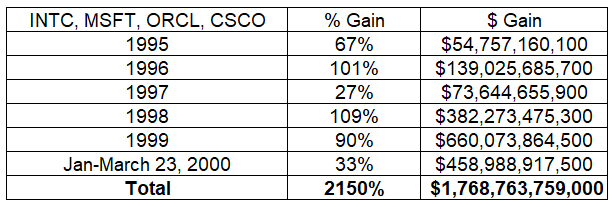

The table below breaks down the combined percentage gain and market cap gain by year. From 1995 until the peak in March 2000, these four added $1.768 trillion in market cap. Again, they were worth just $82 billion five years earlier.

Their growth was driven, to an extent, by fundamental expansion. Earnings more than quadrupled over these five years, but even still, prices got out way over their skis as investors extrapolated this growth too far out into the future. The combined four companies were trading at 100x earnings and 26x sales by early 2000.

There were plenty of people warning about valuations during the late 90s. Jim O’Shaughnessy was one of them. In April 1999, he wrote:

Because the numbers ultimately have to make sense, the majority of all currently public Internet companies are predestined to the ash heap of history. And even if we could see the future and identify the ultimate winner in e-commerce, at today’s valuations it is probably already over-priced….No other market mania has ever produced such outlandish valuations, and I believe that when the inevitable fall comes, it will be harder and faster than anything we’ve ever witnessed.

Bubbles are crazy, especially at the end. This one was no different. The NASDAQ 100 gained 120% in the time that Jim wrote this until a year later when prices finally peaked. In the 63 days from January through March 2000, the S&P 500 market cap increased by $371 billion. More than 96% of that advance was led by these four goliaths, who added $358 billion over the same time.

On January 3, 2000, looking back at the year that was, the New York Times wrote:

To appreciate just how great a year it was for the winners, compare Qualcomm, the best-performing stock of 1999 (among those that began the year over $5 a share) with the top performers of previous years. Qualcomm rose 2,619 percent in 1999. Twelve other stocks on Nasdaq that started the year over $5 managed to climb at least 1,000 percent. A further seven issues rose at least 900 percent.

By contrast, in the first nine years of the decade, only one such stock ever rose as much as 900 percent in a year. That was Amazon.com, which soared 966 percent in 1998.

Jim was very right, eventually. These four stocks would collectively fall 77%. Other stocks got hit much harder.

- Nortel was worth $283 billion. It went bankrupt.

- Lucent was worth 285 billion. It merged with Alcatel in 2006, which currently has an $11 billion market cap.

- America Online was worth $220 billion at its peak before it merged with Time Warner. They were bought by Verizon for $4.4 billion.

- Yahoo was worth $125 billion. It was also recently bought by Verizon, for $4.5 billion.

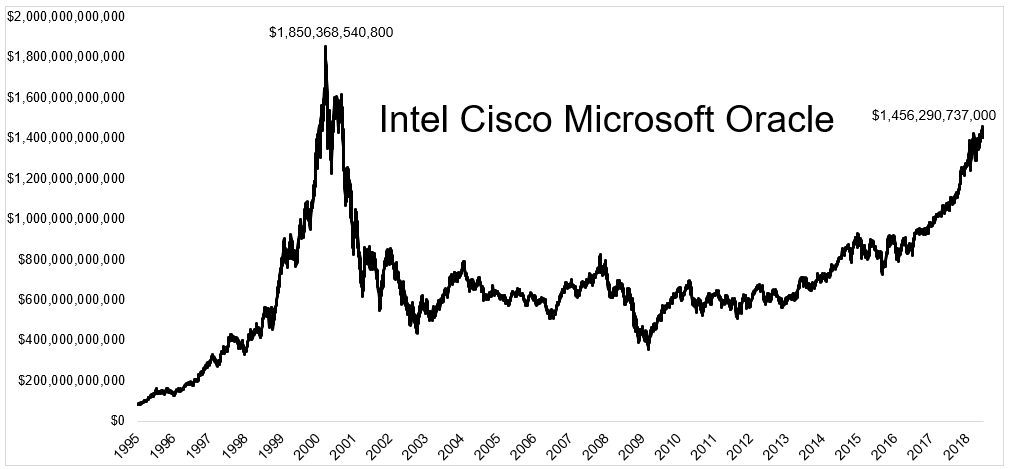

More than 18 years later, the combined market cap of these four companies is more than 20% below the 2000 peak.

Which brings us to today.

For a few years now, people have been comparing the rise of mega cap tech stocks to the late 90s. I think these comparisons are somewhat misguided.

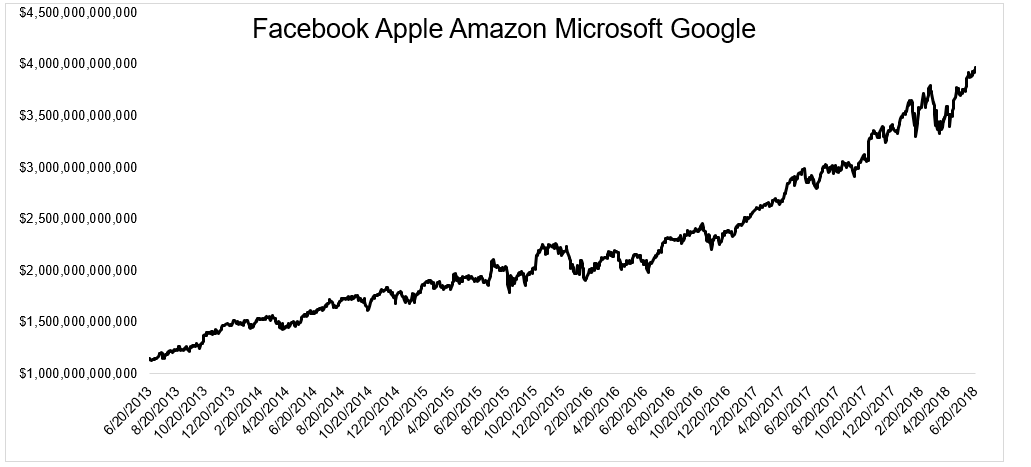

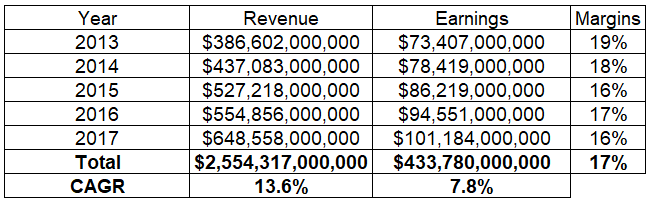

The gains have been extraordinary over the past five years, with Facebook, Apple, Amazon, Microsoft and Google growing from$1.2 trillion to near $4 trillion.

These five gained 43% last year, increasing by more than $1 trillion in market cap. Of course FAAMG is coming off a much larger base, so it’s not an apples-to-apples comparison, but they’ve compounded at 28% a year for the last five years. The four from the dot com bubble compounded at 80% a year in the five years leading up to the peak. As Michael Santoli said, “There’s crazy and then there’s crazy.”

Like the growth of the late 90s, this is also driven, by fundamentals.

Unlike the late 90s, you can justify the valuations. While these names are unlikely to show up on a deep value screen, there is a big difference between today and yesterday. These five have earned nearly half a trillion dollars over the last five years and are currently trading at 37x earnings and 5.5x sales. The four in the late 90s were trading at 100x earnings and 26x sales.

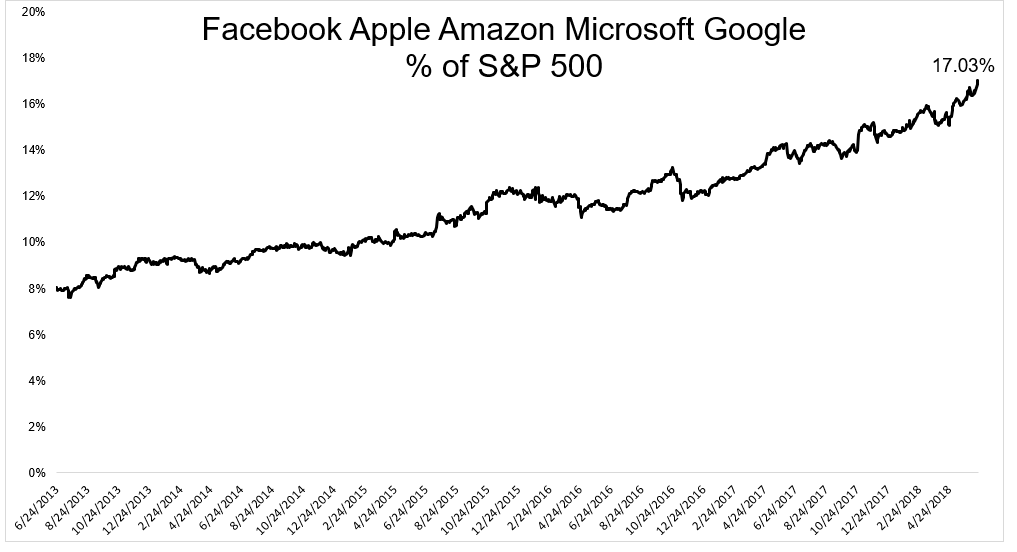

What has people concerned today, among many things, is that Facebook, Amazon, Apple, Microsoft, and Google, are becoming an increasingly larger part of the stock market. Five years ago these stocks represented 8% of the S&P 500. Today that’s grown to 17%.

Many people are blaming the rise of FAAMG on the proliferation of index funds and ETFs. In 2015, when FANG entered the lexicon, the four were responsible for the lions share of the S&P 500’s returns.

Luckily, we have people like Cliff Asness to bring some data to the conversation. He wrote, “It is true that a few stocks bailed out the cap-weighted index last year, but it’s also true in most years.”

But nothing is ever settled, and articles are still being written about how overxexposed index funds are to big tech, and that much of this vulnerability is a result of money coming into these indexes. In a recent article, the author wrote:

ETFs, however, are riskier than many investors appreciate. With cap-weighted indices, for instance, funds have no choice but to load up on stocks that are already overweight (and often pricey) and neglect those already underweight. As prices have risen, investors may become overexposed to a few large securities, such as the big tech companies which now dominate major U.S. indices. That’s the opposite of “buy low, sell high.”

Worse, the ways in which ETFs — by their design and their sheer size — are warping markets aren’t well-understood. ETFs encourage concentration in a few, liquid, large-cap stocks, creating homogenous and momentum–following markets. The focus on driving down costs requires ETFs to emphasize scale, further exacerbating concentration. Markets become susceptible to flows from a few, large, passive products.

Artificial factors, such as inclusion or exclusion from an index, forces buying and selling; this can lead to misallocations of capital. In the current equity cycle, for instance, over-weighted, liquid, large-cap stocks have benefited disproportionately from forced buying. This increases the risk of bubbles, as in 2000.

ETFs may even distort valuations outright. For one thing, they don’t analyze prices, meaning that they don’t contribute to price discovery. They arguably weaken corporate activism, as passive owners have little interest in corporate governance.

The irony here is that active funds, which still represent the majority of assets, are even more exposed to the biggest names than the index funds! From a recent Barron’s article:

Apple accounts for 3.55% of the S&P 500, and 3.63% of the average stock fund. Alphabet accounts for 3.01% of the S&P, 3.44% of the average fund; Amazon.com 2.87% of the index, and 3.4% of the average fund.

If these giants fall, index funds will not come out unscathed, but neither will closet index funds, of which there are still far too many. And the idea, or the question of “what happens when everyone sells at once?” is not worth worrying about. In every recession, people sell stocks. That’s why they fall. After the 1973-74 bear market, mutual funds had 22 consecutive quarters of outflows. People sell stocks during bear markets. The wrapper doesn’t matter.

I’m not suggesting that tech stocks are cheap just because they look like a bargain compared to the dotcom bubble. The dotcom bubble makes everything look like a bargain. But I also don’t think it makes sense to compare them to that time period and then conclude that a dotcom like collapse is coming either.

If tech stocks do fall and if the market falls with them, it won’t be because index investors are stampeding for the exits. More likely, it will happen because growth slows or a recession hits. Earnings will contract along with multiples investors are willing to pay for them.

It’s easy to blame the Fed or ETFs when things don’t go the way you hoped, but don’t allow the problem of others become fears of your own.

***

Below are the tables comparing the four from the late 90s to the five today. All data is from Ycharts.