It has been 2,555 days since gold peaked in September 2011. The S&P 500 meanwhile is within half a percent of its all-time high. Gold investors have good reason to be frustrated, as the precious metal currently sits 40% below those highs.

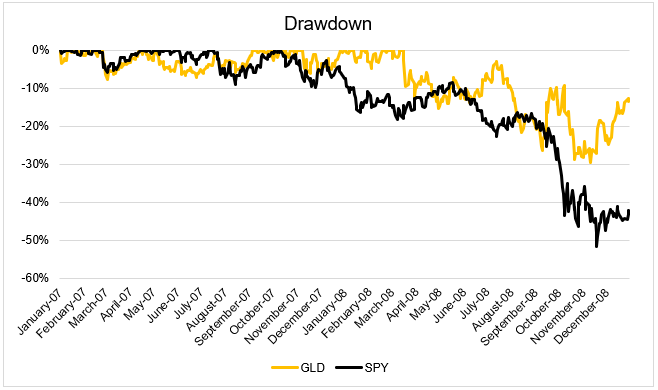

Gold did fantastically well coming out of the GFC, but like most other assets, it got hit hard in the teeth of the crisis. In late October 2008, the S&P 500 was in a 40% drawdown. At that time, gold too was down 30% from its highs earlier that year.

I’m clearly guilty of cherry picking these two time periods, but my point is probably not what you think it is. I’m not making the case that gold goes down when stocks go down and gold goes down when stocks go up. Rather, I’m saying that gold marches to the beat of its own drum, which can make it a great addition to a traditional portfolio of stocks and bonds.

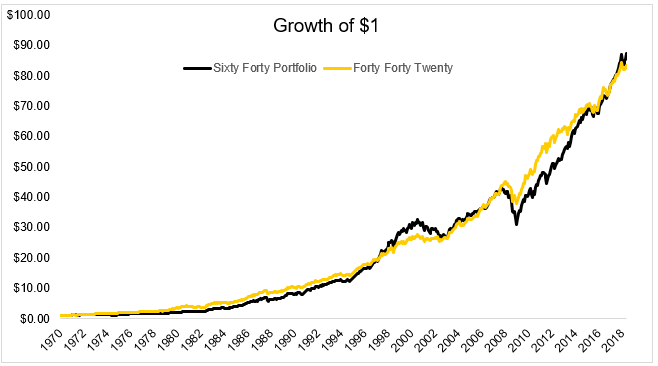

If you had a time machine to go back to 1970 and were able to see the future, you would absolutely add gold to a sixty forty portfolio of stocks and bonds.

The chart below shows the growth of $1 in a 60/40 portfolio (60% S&P 500, 40% Five-Year Treasury Notes, annual rebalance) as well as a 40/40/20 portfolio (40% S&P 500, 40% Five-Year Treasury Notes, 20% gold, annual rebalance)

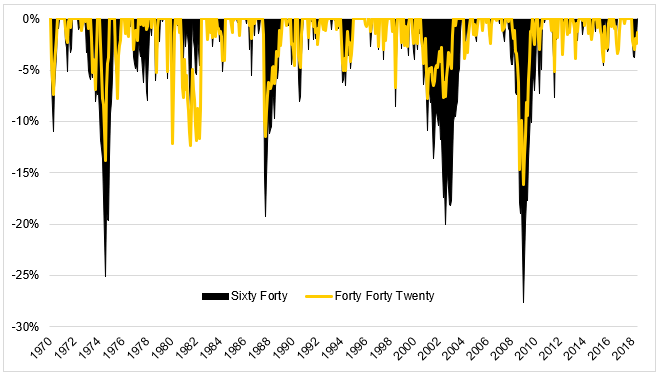

The 60/40 and the 40/40/20 end up with roughly the same terminal value, but the portfolio that includes gold had significantly lower drawdowns, especially during the aftermath of the tech bubble and the GFC.

The table below shows you some characteristics. The 40/40/20 had virtually identical returns, with less volatility and significantly lower drawdowns. The rare trifecta of portfolio management.

Like with stocks, trying to figure out where gold is going is a fool’s errand. Unlike stocks however, gold has no fundamentals. There are no earnings, dividends, cash flow, nothing. The fact that it moves on god knows what is precisely what makes it a very effective diversifier. The chart below shows the rolling 12-month correlation between gold and a 60/40 portfolio.

Everybody wants an asset that is negatively correlated to stocks when stocks enter a bear market, and doesn’t get killed when stocks do fine. Good luck finding this. Non-correlation however is very real and it can be found in gold.

Since gold peaked in 2011, a 40/40/20 portfolio is up 45%, but most investors, certainly myself included, would have had a difficult time not focusing on that one rotting slice. One of the hardest things about managing a portfolio is looking at the sum of the parts instead of focusing on the parts themselves.