The S&P 500 just experienced its worst month since September 2011, falling 6.3% in August. With such a steep decline, the investor in a classic sixty/forty portfolio might have expected bonds to provide protection to their portfolio. The negative 0.08% total return for the Barclays Aggregate Bond Index might lead them to think there’s something very wrong going on. They would be mistaken.

As I have written before, the benefits of diversification are not felt immediately. In fact, when we really need it most, bonds have often failed to deliver. Of the 33 different months (since 1976, creation of the Barclays Index) when the S&P 500 fell by at least 6%, the average return for bonds were just 0.30% less than half of the 0.66% return we’ve seen for all other periods.

Here is the good news, if you extend the time period from one month to one year, bonds have shown their true worth. Of the 100 worst 12-month periods for the S&P 500, bonds were negative along side stocks only three times. The average performance for the 100 worst rolling one-year periods for stocks was -14.2%. The average return for bonds over these 100 different periods was 8.13%.

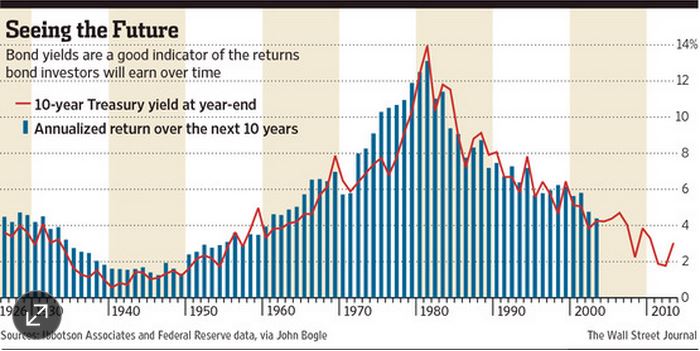

With interest rates being so low, investors holding bonds in a diversified portfolio know that the next forty years cannot look as bright as the last forty years. The math tells us that. From the Wall Street Journal: “Since 1926 he notes (Bogle), the entry yield on the 10-year treasury explains 92% of the annualized return an investor would have earned over the next decade.”

With the ten-year yielding just 2.2%, it makes little sense to think your returns will be much more than this over the next decade . However, what investors can expect from bonds, is the dry powder they may provide when stocks experience something more than a ten percent sell off. The ability to rebalance into stocks as they go on sale is one of the main reasons why diversification works over the long-term. Focusing on one-month or even one-year returns completely misses the point.

Michael Batnick is a managing partner at Ritholtz Wealth Management. He is the co-host of Animal Spirits, What Are Your Thoughts, and The Compound and Friends. For disclosure information please see here.

Get a Full Investor Curriculum: Join The Book List

Every month you'll receive 3-4 book suggestions--chosen by hand from more than 1,000 books. You'll also receive an extensive curriculum (books, articles, papers, videos) in PDF form right away.