What if stocks experience their third separate bear market in under twenty years? What would that do to the psychology of investors?

For the purpose of this exercise, please allow me to reach a little (I’ll explain later).

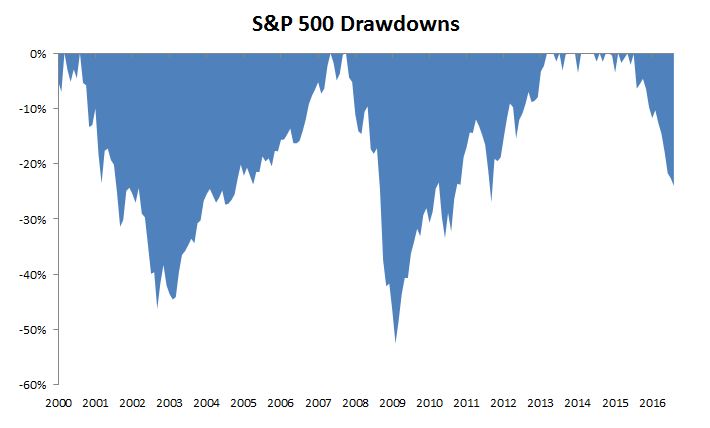

If the S&P 500 were to fall 25% from its peak over the next twelve months (~16% lower from today), it would experience its worst return over a sixteen-year period (5%) since 1931-1947. Three separate drawdowns of at least 25% in so short a period of time could leave lasting scars. Here is a visual of what this would look like.

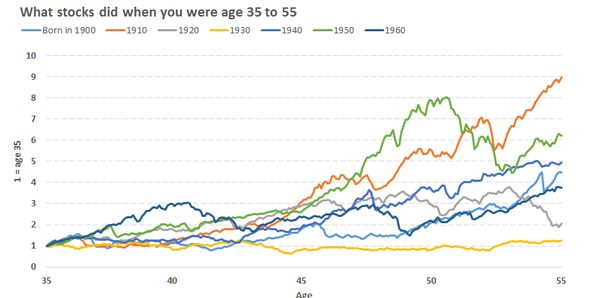

My friend Morgan Housel shared an interesting chart showing how stocks performed for investors between the ages of 35 and 55 depending on when they were born. This demonstrates the returns that stocks deliver are entirely out of our control. An investor born in 1930 had a much different experience with stocks than an investor born in 1910. As Jason Zweig says “The stock market is not going to provide a high return just because you need it to.”

If this scenario of a third bear market were to play out, the 35 year old investor born in 1965 would have seen the S&P 500 make very little progress during their peak earning years. Investing for so long without being compensated for the risk you bear can permanently damage investors’ psychology. Let’s look back to an article by Walter Gutman in 1948 from the Financial Analysts Journal (emphasis mine):

A far larger part of our potential customers are staying away from us than is good for our pocketbooks, and the reason is that the securities business has not meant security to hundreds of thousands of investors. Statistics on incomes and savings show that there are hundreds of thousands of people (at least) who do not own securities (other than Government bonds) who have the money to own them if they wanted to. For instance, the public owns about $52 billion of U.S. Savings bonds and has about $56 billion more in various time deposits. The total current value of all securities listed on the New York Stock Exchange is $65 billion. It does not take much imagination to believe that the securities business could be enlarged if the public could believe that their savings were reasonably secure in securities.

Our position as the public’s enemy has come about accidentally. We ourselves were once members of the public, and we were drawn into our profession by the allure or the terror of 1929, 1932, 1937, etc. We are children of the bull market, and our psychology cannot help be patterned by our birth.

This article was written in a time where the Dow Jones Industrial Average had not made any progress for over twenty years. Understandably so, this left people underinvested and disillusioned with stocks (The Dow would gain nearly 200% over the following decade).

They say that beauty is in the eye of the beholder, so are markets. Our views are shaped by what we buy, when we buy it, what just happened and what we hope to happen that never does.

It might be disconcerting that returns are unpredictable and unreliable, but investors would be best served focusing on what they can control. Allowing fear and greed to interfere with whatever plan you have in place is all but guaranteed to lead to under performance, not just of the market, but of your own investments.

**

The point of this post is clearly a mental exercise, but for volunteer policemen, here are some obvious caveats.

1) I’m assuming (not predicting) the S&P 500 falls an additional 17% over the next 12 months.

2) I’m totally cherry picking (using a 16-year period)

3) I am assuming index fund returns only. Obviously, there are all sorts of different strategies and investors are not limited to U.S. cap weighted indexes.

4) Total return changes everything. The worst 30-year total return for the S&P 500 turned $1 into just $9.51, compounding at 7.8% a year for thirty years.

5) I’m not comparing now to the Great Depression era, I realize the vast differences. It was the lasting psychological impacts I was interested in.

[…] Luck has a lot to do with your lifetime market returns (Irrelevant Investor) […]