Fama and French wrote “The Cross-Section of Expected Stock Returns” in 1992, unveiling their three-factor model. They expanded on CAPM, which boils down stock returns to just one factor, beta. Fama and French took this a step further, finding that the vast majority of a stocks returns can be explained not just by beta, but by size and book-t0-market as well. Twenty-three years later Igor Gonta, CEO of Market Prophit has found the fourth factor, and that factor is us.

Here’s how it works: Market Prophit ranks financial tweeters based on the accuracy of their tweets. According to S&P Dow Jones, their index provider, Market Prophit “uses quantitative algorithms to rank and score financial pundit/blogger performance based on the accuracy of their stock market commentary and track record of predictions.”

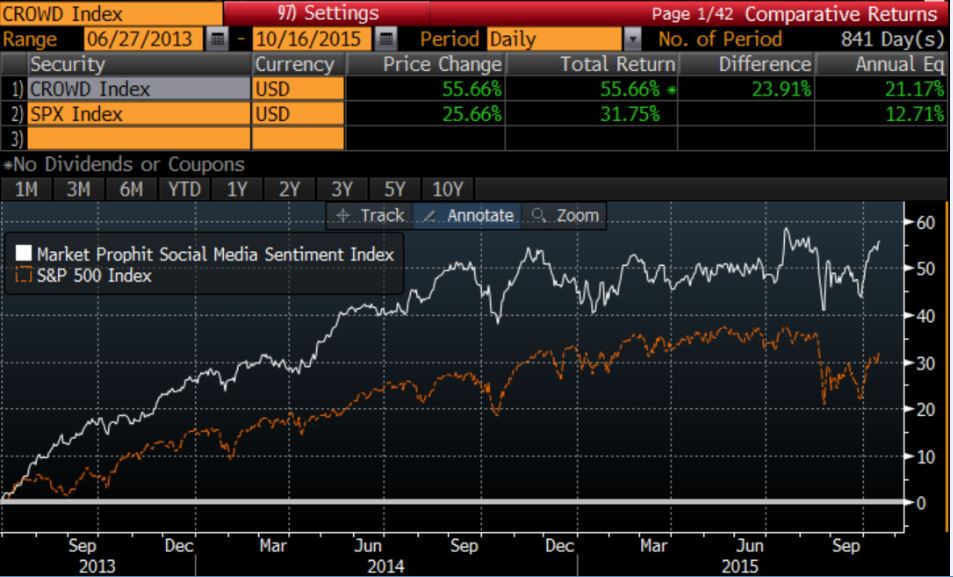

You might be thinking this sounds pretty silly, but get this. The index was launched in May 2015, but has data going back to July 2013. The index excludes ETFs, penny stocks and any stock that has a market cap of $1 billion or less. The performance has been nothing short of spectacular.

Will CROWD be another case of a great looking back test that doesn’t work in real life? We’ll see, there certainly will be some real life obstacles, taxes, borrow, etc. I’m excited to see who rolls out the ETF and how many assets it will attract.

Seems like causality could go the other way, people tweet and stocks go up. Didn’t see how many “bloggers and tweeters” they follow, did you? Lastly, this reminded me of Bringing Down the House, the MIT card counters – keep track of the conditions and then make a play.

Nice post Mike

Michael Batnick is a managing partner at Ritholtz Wealth Management. He is the co-host of Animal Spirits, What Are Your Thoughts, and The Compound and Friends. For disclosure information please see here.

Get a Full Investor Curriculum: Join The Book List

Every month you'll receive 3-4 book suggestions--chosen by hand from more than 1,000 books. You'll also receive an extensive curriculum (books, articles, papers, videos) in PDF form right away.

Seems like causality could go the other way, people tweet and stocks go up. Didn’t see how many “bloggers and tweeters” they follow, did you? Lastly, this reminded me of Bringing Down the House, the MIT card counters – keep track of the conditions and then make a play.

Nice post Mike

Interesting article Michael. Have you read The Wisdom of Crowds by James Surowieki? This “fourth factor” reminds me of the ideas in that book.

Nope, will put it on my list. Thanks for reading, Joseph.