“There is nothing new in Wall Street. There can’t be because speculation is as old as the hills. Whatever happens in the stock market today has happened before and will happen again” – Jesse Livermore

Long before Cliff Asness wrote his dissertation on momentum, Alfred Cowles and Herbert Jones discovered that stocks tended to move in the direction in which they came from. In “Some A Posteriori Probabilities in Stock Market Action” from 1937, they say:

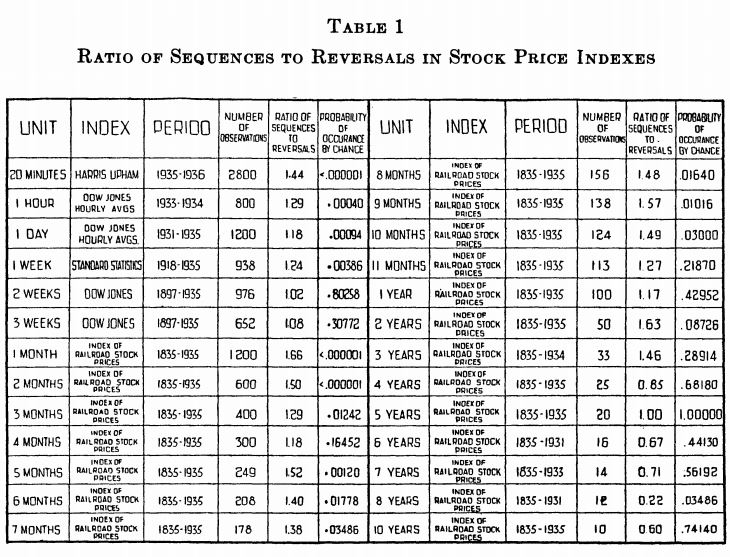

“It was found that, for every series with intervals between observations of from 20 minutes up to and including 3 years, the sequences outnumbered the reversals, For example, in the case of the monthly series from 1835 to 1935, a total of 1200 observations, there were 748 sequences and 450 reversals. That is, the probability appeared to be .625 that, if the market had risen in any given month, it would rise in the succeeding month, or, if it had fallen, that it would continue to decline for another month. The standard deviation fro such a long series constructed b y random penny tossing would be 17.3; therefore the deviation of 149 from the expected value 599 is in excess of eight times the standard deviation. The probability of obtaining such a result in a penny-tossing series is infinitesimal.”

The simple reason why momentum investing works is because people have a tendency to follow what’s popular and avoid what isn’t. This style, once shunned as “thoughtless” or “idiotic” has been gaining steam lately, thanks to really smart guys like Wesley Gray and Patrick O’Shaughnessy.

Michael Batnick is a managing partner at Ritholtz Wealth Management. He is the co-host of Animal Spirits, What Are Your Thoughts, and The Compound and Friends. For disclosure information please see here.

Get a Full Investor Curriculum: Join The Book List

Every month you'll receive 3-4 book suggestions--chosen by hand from more than 1,000 books. You'll also receive an extensive curriculum (books, articles, papers, videos) in PDF form right away.