Most of the time I’m writing for the laymen investor. Nothing I’m sharing is particularly actionable as I believe 99% of investors are better off thinking than acting. Traders and hedge fund managers don’t need my help, but hopefully the average investor who reads my blog is able to learn a few things about common sense investing.

Many of us who watch the market all day long take for granted our level of knowledge and it’s easy to take umbrage with a very simple message somebody is trying to convey. This post can potentially be one of those times. Before I go any further, here’s a quick story about the laymen investor.

A few years ago I recommended my friend begin investing in index funds. He told me he didn’t want to buy SPY because it was trading at over $200 a share, so instead he bought VTI, which at $100 was “half the price.” This might sound silly to you but for people who have jobs outside of finance, this seems like a reasonable thing to say. I mention this because what I’m writing today is not a portfolio recommendation, rather I am trying to explain a very simple point to young investors with literally decades of investing ahead of them. I’m going to address the power of dividends, compound interest and time.

I write this preamble to try and stem the inevitable tide of “what if you did this” responses. If you can’t read this without feeling the urge to incinerate what follows, please click away now. Thank you.

***

If you’re like most people, you contribute to your 401(k) every two weeks and only notice the stock market when the your balance falls ten or twenty percent. With the recent volatility, it might be your inclination to run and hide until the dust settles. In theory this makes sense, in reality it could be one of the most destructive actions you can take when attempting to build long-term wealth.

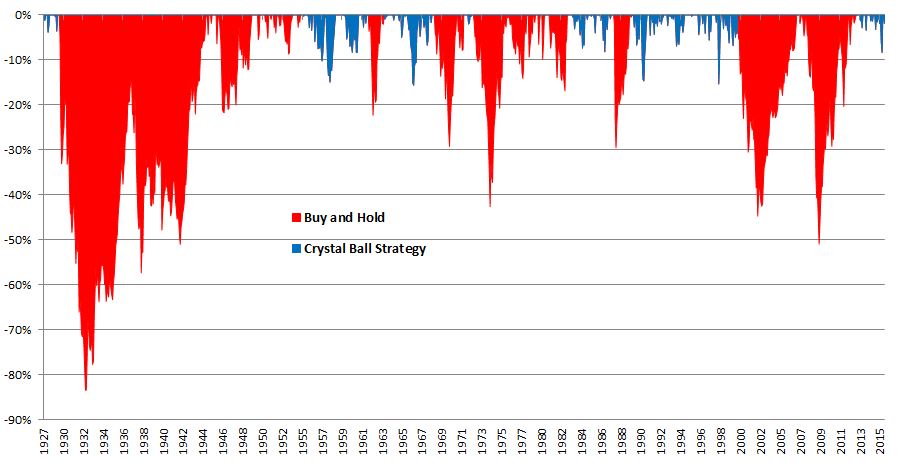

But what if there were a way to eliminate the lousy feeling of checking your account by simply avoiding every bear market? Well lucky for you it exists and I call it the crystal ball strategy. The premise is very simple: every time you know a 20% drawdown is coming, you sell at the peak and wait for the bear market to run its course. In the meantime, you invest in short-term treasury bills and only get back into stocks when they’re at the level at which you sold; no point in trying to catch a bottom, right? Look at the declines of the Crystal Ball Strategy versus a simple buy and hold methodology.

You’ll notice that the Crystal Ball Strategy isn’t perfect, it did experience a 16% drawdown in 1966 (my bad), however, it sure did a lot better than buy and hold, which got cut in half on multiple occasions.

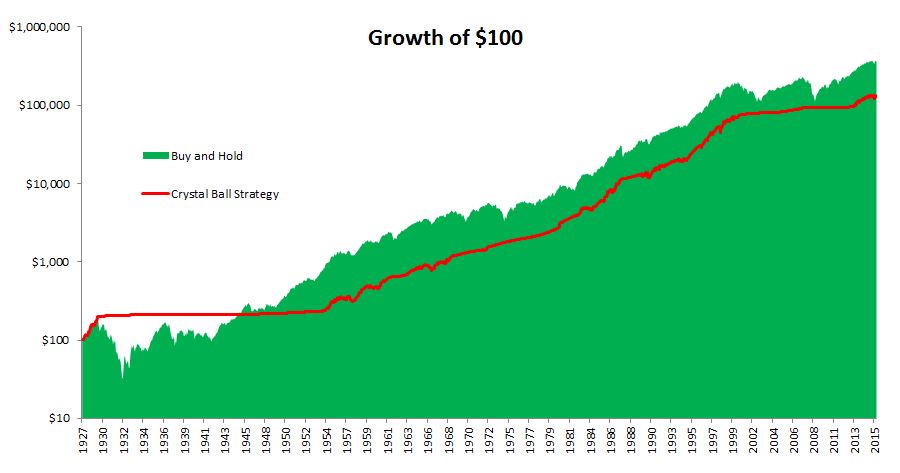

By now, it should be obvious that the Crystal Ball Strategy is a farce, nobody can identify every peak before a 20% bear market. But what might shock you is that even if you were able to avoid every 20% drop, you still would have been better off buying and holding. Buy and hold ended up with $360,856 versus $130,523 for the Crystal Ball Strategy, beating it by nearly 200%. How is this possible? The Crystal Ball Strategy kept you out of stocks 62% of the time, robbing you of the ability to leverage dividends, compound interest, and time.

Compound interest is one of those concepts that is really hard to wrap your head around. One of the best investors of all time, Warren Buffett understands this concept extremely well. Think about this, 98% of Buffett’s current net worth was accumulated after he first become a billionaire at age 56.

Another person who understands compound interest is my friend and colleague Ben Carlson. Ben wrote a post where he mentioned that the worst 30-year period for the S&P 500 was 854%. A lot of people think “wait a minute, 854 divided by 30 is 28.4% a year, that isn’t possible.” Well, they’re right that it’s not possible, but they’re misunderstanding how compound interest works. An 854% gain over thirty years requires a compound growth rate not of 28.4%, but just 7.8%. The takeaway is that whenever you run out of the market, you’re not receiving the incredible benefit of compound interest or the benefit of reinvesting dividends at bargain prices.

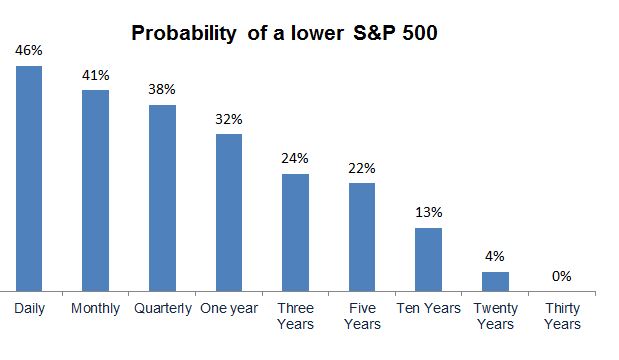

Regular people underestimate the huge advantage they have over professionals. They have nobody to report to. Most managers live and die in three-year windows. You have the ability to leverage time and compound interest. Nobody knows what future returns will be, but I can tell you for a fact that the likelihood of losses decreases with the passage of time.

So if you’re tempted to sell out of your 401(k) on Tuesday, recognize that you are likely doing your future self a big disservice. Volatility is a permanent feature of the stock market. I’ll end with a brilliant piece of thinking from my friend Morgan Housel.

Volatility is price of admission. The prize inside are superior longterm returns. You have to pay the price to get the returns. Many aren't.

— Morgan Housel (@morganhousel) January 15, 2016

***

If you ignored my warning and are still reading, you’re probably not too pleased with this post. I understand that there are legitimate ways to manage risk without having a crystal ball. However, wouldn’t you agree that 99% of investors are better off not trying to play George Soros? I mean, after all, you’ve probably worked for years and years before you mastered whatever system you’ve implemented. Wouldn’t you agree that the average person who goes to work outside of finance has no business competing with you? Is buy and hold not the best way for a young person to take advantage of the inevitable progress that the future holds?

Yes I understand that people aren’t reinvesting dividends for 90 years, and that on shorter time periods missing every 20% drawdown will probably have additive effects. Please recognize I am trying to explain a very simple concept to people who might get scared and do something stupid. I do think the majority of investors are best buying and holding through good times and bad, sue me.

How about a similar idea for those of us no longer working but having, hopefully, 20-25 years of managing our investments and not running out of money.

Why don’t you compare buy and hold to timing strategy instead of this fluff crystal ball BS? You are smart and very well read. Why are you wasting your talent? You’re better than this. You could realy help a lot of people.

Michael – this is very interesting analysis. My concern is that anytime you do an analysis over such a long time horizon 1927-2015 then buy – hold would work. However this time line is unrealistic for most people. I would be interested to know if over an average of 30-40-50 years time span this would work ?

Nice post. Following you (and Carson and Housel, etc) I’ve noticed that it’s really hard to write w/o falling into the “each case is different” trap. This post missed that by explaining an idea. Well done.