The arrival of the auto industry changed the way we lived, however like any new technology, it did not come without a cost. In 1917, Detroit had 65,000 cars on the road, which resulted in 7,171 accidents and 168 fatalities. Advances in financial technology has exploded over the last few years, and like the birth of the auto industry, it has the potential to result in a few accidents.

Although constructing a portfolio has never been cheaper, it has also never been as confusing. With a plethora of choices, from cap-weighted to smart beta, currency hedged to low volatility, to quality and dividend payers, the options can be pretty overwhelming. Perhaps it is no surprise that this has left investors’ paralyzed, with them opting to invest their 401(k)s in target-date funds, which experienced a record $69 billion in positive net asset flows in 2015.

When you open up your 401(k) lineup, it can be like reading a foreign language. And even if the only options available were index funds, it could still get pretty confusing. I want to point out a few things worth thinking about as you’re selecting from your investment menu, because the names and descriptions of the indexes can be pretty misleading.

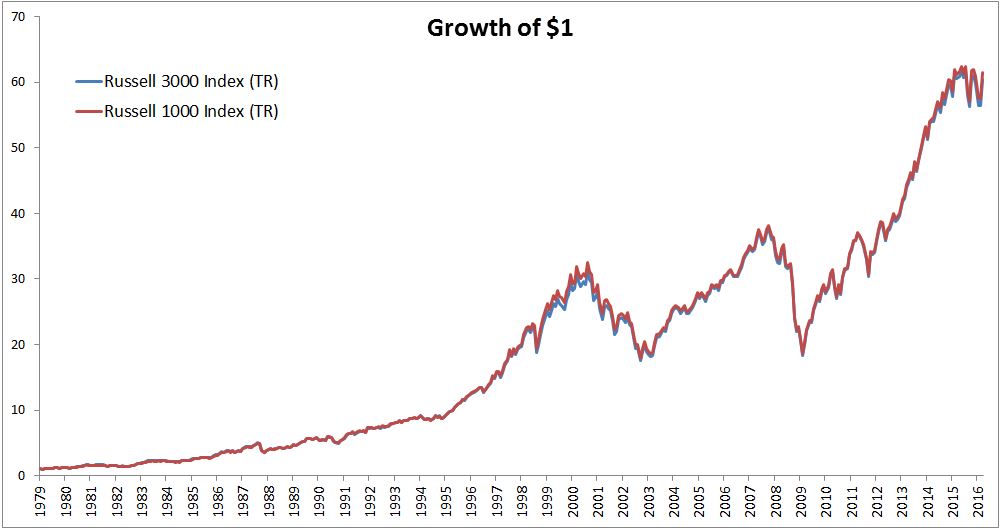

Take the the Russell 3000 for example, which provides investors with “broad exposure” to the 3000 2981 biggest stocks in the U.S. Upon closer inspection you’ll find that while it does technically provide broad exposure to the U.S. stock market, it will perform almost exactly the same as the Russell 1000, which represent the 1000 1021 largest U.S. stocks.

Since inception, the Russell 1000 has compounded at 11.69%; the Russell 3000 has compounded at 11.64%. For all intents and purposes, with a correlation of .9986, the Russell 1000 and the Russell 3000 are identical twins.

The reason why these indexes are so similar is because of their market cap weighting; which explains why the Russell 3000 is really just the Russell 1000 in disguise. The five largest stocks in the Russell 1000- Apple, Microsoft, Exxon, Johnson & Johnson, Microsoft and General Electric- are bigger than the entire Russell 2000. Patrick O’Shaughnessy weighs in on how cap weighting affects index returns:

If Exxon went up 40 percent, it would push the overall index up 1.44 percent. If Seadrill went up 40 percent, it would push the index up 0.004 percent. Seadrill would have to go up 14,400 percent to have the same impact as Exxon’s 40 percent rise.

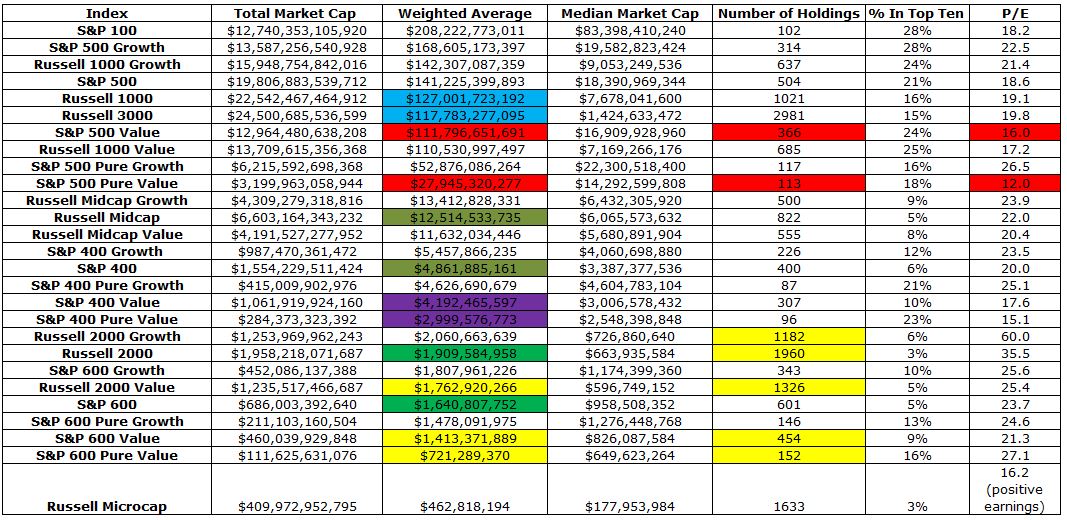

Let’s take a look below at characteristics of seemingly similar, but very different indexes (sorted by weighted average).

A few things stand out:

- Although the median market cap of the Russell 1000 is five times larger than the median market cap of the Russell 3000, what drives cap-weighted indexes is the weighted average market cap, which is very similar for the Russell 1000 ($127B) and the Russell 3000 ($117.7B).

- The Russell Midcap Index and the S&P 400 Midcap Index define mid-caps a lot differently, with the weighted average market cap of the Russell Index being 157% larger than the S&P Index. Likewise, the weighted average market cap of the Russell 2000 is 16% higher than the S&P 600, which both claim to track small cap stocks.

- Out of the 1960 stocks in the Russell 2000, 67% are in the Russell 2000 Value Index, and 60% are in the Russell 2000 Growth Index. You’ll probably notice that those two numbers equal 127%, which doesn’t make any sense. That’s because their style indexes are a “blend,” meaning a stock can appear in both the value and growth indexes.

- S&P has a cure for this; They created “pure” indexes, where stocks won’t overlap in the growth and value indexes and many stocks won’t even make it into in either index. In fact 54% of the stocks in the S&P 500 are not in the pure value or the pure growth index.

- The differences in the pure value and the “plain vanilla” value indexes are significant. The S&P 500 Value Index has a weighted average market cap of $112B, with 366 holdings and trades at 16x earnings. The S&P 500 Pure Value Index has a weighted average market cap of $28B, with 113 holdings and trades at 12x earnings .

If all these technicalities have your head spinning, you need not worry. The truth is that choosing the right allocation won’t drive returns as much as your ability to stick with whatever allocation you’ve chosen. I guess the million dollar question is “how do you arrive at the right allocation?” William Bernstein, in The Intelligent Asset Allocator has the perfect take on this:

“So how do you arrive at the allocation that will provide the most return with the least amount of risk? You can’t. But don’t feel bad, because neither can anyone else.”

You’re never going to be able to have the perfect portfolio year in and year out, but at the very least, make sure you understand what you own and why.