Stocks always have a positive expected return. With the passage of time however, these expected returns turn into realized returns and obviously they’re not always positive.

We just can’t know what the market will deliver, so it’s best to plan and prepare for a wide range of outcomes. This range is determined by a number of factors, including but not limited to the business cycle, valuations, interest rates, inflation, and the collective mood of millions of investors.

Yesterday, Research Affiliates put out a piece saying the chance of a 60/40 portfolio returning 5% a year for the next ten years is zero. Yikes. One of the reasons they, and others, have cited to lower your expectations is because of the high returns we’ve experienced in the past.

“One message that John West, head of client strategies at Research Affiliates and a co-author of the report, hopes people will take away is that the high returns of the past came with a price: lower returns in the future.”

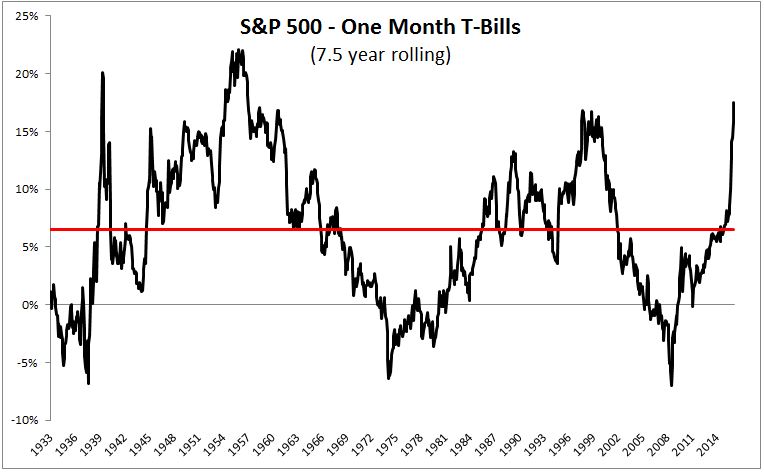

They’re not wrong, since the bottom in 2009, stocks have outperformed risk free bills by 17.5% a year, the largest spread over a 7.5 year period since 1958!

But for longer-term investors, it hasn’t been all rainbows and butterflys. Since the top in March 2000, the S&P 500 has outperformed risk-free assets by just 2.7% a year, well below the long-term average of 7%.

Part of what makes investing interesting is you can anchor to any point you’d like and craft your own narrative or choose your own adventure. I try not to focus too much on historic highs and lows and I certainly don’t spend much time thinking, “what will stocks do over the next decade.” But If we do experience low returns, behavior will matter more than ever, so I’m trying to anchor not to the bottom in 2008, or the top in 2000, but to what really matters, my future.

Investors live in multiple time-frames. I have another thirty working years, so I have to keep my eye on the ball while putting myself in a position to survive multiple one, three, five and ten-year periods. The most important thing I can do to maximize my chances for a financially comfortable future are to continue to invest, control my behavior, and let compounding work its magic.

Finally, I think this idea from a recent Jason Zweig article is a great way to think about your relationship with the market.

“Investing is always a partnership between you and the markets,” says Mr. Kinniry. In the 1980s and 1990s, when stocks and bonds alike racked up double-digit average returns, the markets did most of the work. “But now you are going to have to be the majority partner,” he says.