Yesterday I received an email that read, “If you are looking for alternative sources of stable income with a demonstrated ability to make money in a rising rate environment….” For this reason, most get trashed before opening, but once in a while, I’ll click to see what’s out there. Today, I received one from a multi-strategy fund of funds with pretty underwhelming performance, so I opened the fact sheet to see what was going on.

I’m not from the hedge fund world, but I saw a lot of brand name managers in here, ones that even I recognized. The one pager provided provided monthly returns, so I pulled them into excel to see if I could figure out why something that has done so lousy has $5 billion in assets. Since inception, this strategy has severely lagged both the S&P 500 and a simple 60/40 portfolio.

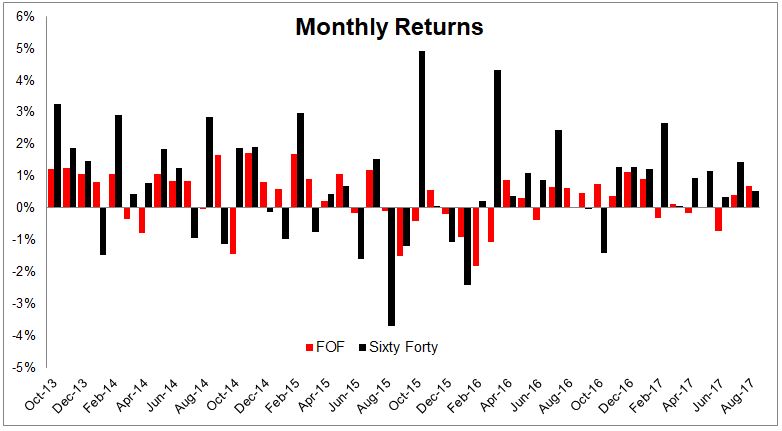

But I realized I was unfairly doing what everybody else does, which is comparing apples with butterflies. What does a multi-strategy fund have to do with stocks or bonds? I fell prey to the old all or nothing analysis. The monthly returns below, with a 0.09 correlation, show that these strategies might actually, wait for it, complement one another.

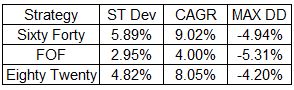

Adding a 20% allocation to this multi-strategy fund would have improved the risk-adjusted returns.

It probably wouldn’t have made a huge difference one way or the other, but adding this to a core holding certainly makes more sense than comparing it to that core holding. The table below shows the risk and return profile when you combine the fund with a sixty forty portfolio. Lower returns, but way less volatility, and a lower drawdown. By the way, the max drawdown for a sixty forty portfolio since the end of 2013 is less than 5% which is incredible, and for a different post.

Investing in this type of strategy is not something I would choose to do with my money, but I understand why others are making that choice, especially if this remains as uncorrelated to stocks and bonds when they’re falling as it has when they’re rising.

Michael Batnick is a managing partner at Ritholtz Wealth Management. He is the co-host of Animal Spirits, What Are Your Thoughts, and The Compound and Friends. For disclosure information please see here.

Get a Full Investor Curriculum: Join The Book List

Every month you'll receive 3-4 book suggestions--chosen by hand from more than 1,000 books. You'll also receive an extensive curriculum (books, articles, papers, videos) in PDF form right away.

Adding a 20% allocation to this multi-strategy fund would have improved the risk-adjusted returns.

Adding a 20% allocation to this multi-strategy fund would have improved the risk-adjusted returns.