I spend the majority of this space writing about the challenges associated with investing. I even wrote a whole book on it.

Why am I such a Debbie Downer when it comes to this stuff?

Well, maybe it’s sour grapes. Look, I tried for years to beat the market, couldn’t do it. Then over time I came around to the idea that trying to beat the market, in the words of Charlie Ellis, is a loser’s game. Then I came to realize that just getting market returns is no walk in the park.

So how hard is investing really? First we have to breakdown investing into its two simplest components. There is portfolio construction and then there is portfolio oversight.

Constructing a good enough portfolio isn’t nearly as difficult as the investment industry often makes it out to be, but overseeing our portfolio while managing our emotions is probably still harder than we give it credit for.

The average person tends to over complicate investing due to their own biases and the professional tends to over complicate it due to career risk. But investing can be as simple as owning stocks and bonds and doing it in just two products.

I’m going to show how simple it is to construct a portfolio that will get you 90% of the way there.

**This is not advice. This is not advice. This is not advice.**

You can now build an all you need type of portfolio basically for free.

For stocks, in just one product, you can get exposure to over 1,000 companies around the globe. This is available through multiple fund families for single digit basis points. For bonds, you can get exposure to U.S. investment grade bonds also for next to nothing.

You should expect stocks to outperform bonds over long periods of time, and you should expect bonds to hold up relatively well when stocks get hit. You can then take advantage of the pain by rebalancing out of bonds and into stocks.

Investors should think in terms of worst case scenarios and let the upside take care of itself. There are difficulties with staying put in a bull market and not getting sucked into the latest fad, but for the average investor who doesn’t pay much attention to the day-to-day gyrations of the market, they’re more likely to do irreversible damage during a nasty bear marker.

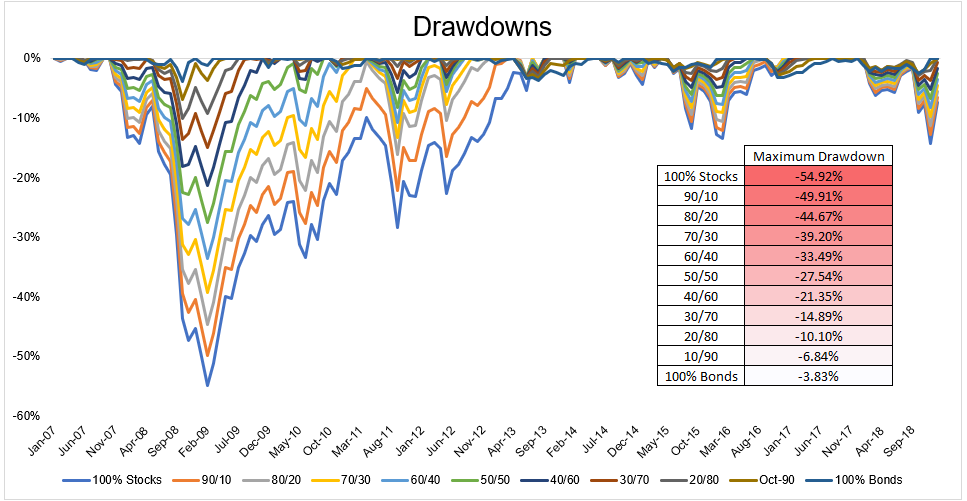

In order to find the appropriate mix of stocks and bonds we should look at the events from 2007-2009 which ought to do a decent job of calibrating our risk tolerance.

At the lowest levels in 2009 an all stock portfolio lost 55%. Percentages hide the misery so insert your portfolio amount and then try to imagine how you’d feel. What if you had a $30,000 portfolio that goes down to $13,500. Sound horrible? What if it turned into $18,000 (70/30)? Still too painful? Do this until you find a potential point of comfort. Nothing will replicate how this actually feels but if you can’t stand the idea of losing 40% in theory then you definitely can’t stomach this in real life.

*MSCI All-Country World Index, U.S. Bloomberg Aggregate Bond Market. Indexes are not available for direct investment

It’s important to look at the worst case because returns aren’t guaranteed, but risk is. If you can just find the right-ish mix of stocks and bonds, you can move onto more productive uses of time like trying to advance your career and spending time with friends and family.

Beating the market is great, it’s just that most people don’t and few actually need to in order to fund the lifestyle they want to live. So focus on things that you have control over, like how much you spend and how much you save.

Figuring out the right portfolio for you isn’t easy, but it doesn’t have to be rocket science. Worry about getting 90% of the way there and let other people worry about the 10%.