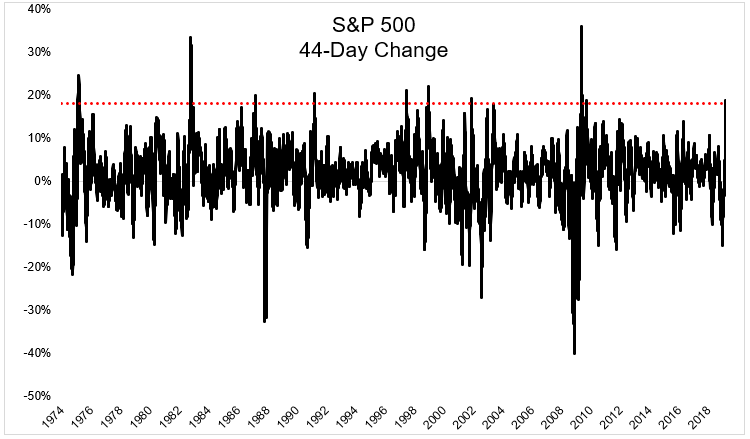

The S&P 500 just rocketed 18% higher in only 44 days. A bounce of this magnitude makes a mockery of risk management.

This is the ninth time stocks have experienced a killer vee bottom since 1970. I refer to them as killer vees because they suck for everyone. It makes buy and hold investors sweat and it makes mincemeat of most tactical investors.

The charts below show these killer vees in red. I broke this up into two time periods so we can clearly see what is going on. Just eyeballing it, you can see they occurred near major market bottoms.

The chart below shows the drawdowns for the S&P 500 with the beginning of these moves in red. On average, the S&P 500 was in a 25% drawdown (median -20%) when these killer vees started buzzing. The good news is that 8 out of 9 times marked major market bottoms (No, this does not mean there is an 89% chance this was the bottom). The bad news is 2001 was a major head fake and there is no way to know whether today is 1982 or 2001.

One of the challenges with tactical portfolio management, particularly with trend following, is that whipsaws are part of the deal. They can only be avoided by data mined backtests. In the real world, these false moves should be thought of in terms of a premium you pay the insurance company. While you never want to put in a claim, they aren’t much fun to pay either. I can’t think of anything to say other than, hey, that’s the way it goes sometimes.

Trend-following can be very difficult to employ on its own, psychologically, but it can work well in concert with a buy and hold approach. This can allow investors to potentially have their cake and eat it too. Yes, I’m talking my book here, we use a trend-following model for our clients.

Vee bottoms suck for tactical strategies, but they’re alright for the do nothing portfolio. A Jekyll and Hyde portfolio can be frustrating at times, but diversification is the hardest free lunch in investing.

If you’re interested in learning more about trend-following, I highly recommend this podcast with Meb Faber and Marty Bergin

Michael Batnick is a managing partner at Ritholtz Wealth Management. He is the co-host of Animal Spirits, What Are Your Thoughts, and The Compound and Friends. For disclosure information please see here.

Get a Full Investor Curriculum: Join The Book List

Every month you'll receive 3-4 book suggestions--chosen by hand from more than 1,000 books. You'll also receive an extensive curriculum (books, articles, papers, videos) in PDF form right away.