After doing a financial plan with Bill, and after reading Ramit’s book, I thought it would be appropriate to figure out where our dollars are going every month.

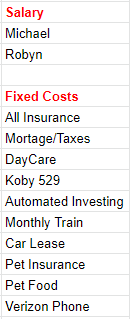

The first step was looking at our after-tax income. This is what actually hits our bank account, so net of retirement contributions.

Fixed costs are the last items that I would want to cut in case of an emergency. I could scale back on Koby’s 529, or my investing, but ideally these items stay in place indefinitely. My biggest expense by far, like most people, is the roof above our head. I included my automated investing here because I think it’s helpful to think of this as a non-negotiable bill every month. Pay yourself first.

Fixed costs represent approximately 50% of our after-tax income.

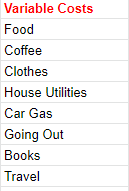

Next we covered our variable costs. I used rough but reasonable assumptions here. I don’t know exactly how much we’re spending a month on food, and I’m very fortunate to be in a position where I don’t need to know exactly what it is. Even if I’m off by 5 or 10% here, my spending is still under control relative to our income.

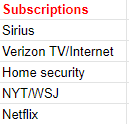

Next are my subscriptions. These are items that hit the credit card every month, and would be the first to go in case things get tight. Even if I took these to zero, which would be impossible, they represent less than 5% of our after-tax income.

The biggest takeaway for me after going through this exercise with my wife is that the fixed costs are what can get you into trouble. If you let these grow to be too large a percentage of your monthly income, the other things you do won’t really move the needle. I don’t know the right number for your fixed expenses, but less than 60% sounds about right.

I encourage everyone to figure out where your dollars are being spent. It doesn’t take too long and in the event that you do need to make changes, this can help guide you.

Michael Batnick is a managing partner at Ritholtz Wealth Management. He is the co-host of Animal Spirits, What Are Your Thoughts, and The Compound and Friends. For disclosure information please see here.

Get a Full Investor Curriculum: Join The Book List

Every month you'll receive 3-4 book suggestions--chosen by hand from more than 1,000 books. You'll also receive an extensive curriculum (books, articles, papers, videos) in PDF form right away.