I always assumed that a flat long-term moving average was more bearish than bullish. I thought that a trendless market occurs when a bull market fizzles out, right before the bear arrives. This is not the case.

Nick Maggiulli created this amazing GIF which shows the distribution of forward returns when the slope of S&P 500’s 200-day moving average is flat, higher, or lower. Bad things happen in falling markets, to state the very obvious, but a flat 200-day on the other hand, tells you very little, if anything about the forward direction of stock market returns.

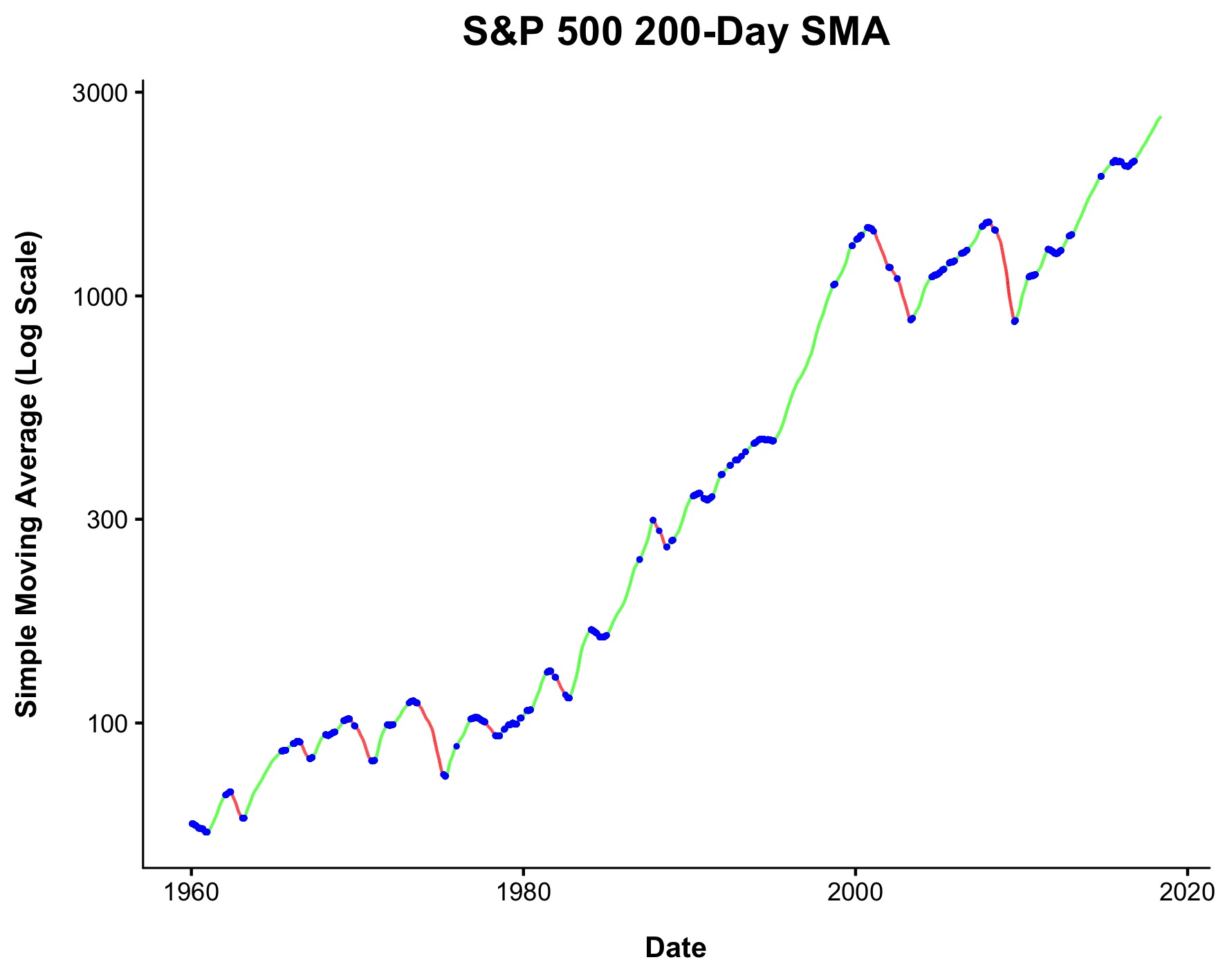

More often than not, when the 200-day moving average is flat, it’s in “resting, wants higher” mode. Since 1960, following a flat sloping 200-day, a 20% drawdown occurs just 0.5% of the time within 60 trading sessions, which is approximately three months. If we extend this to 120 sessions, or around six months, this rises to just 2.5% of the time. As you can see in the chart below, since 1960, the trend of the 200-day moving average has been higher 62% of the time, flat (blue) 17% of the time, and down 21% of the time.

Not only are returns not bad following a flat moving average, they’re actually better than average. The table below shows returns on the left (annualized), and standard deviation on the right. The good news is the curve is now flat, the bad news is it looks it’s about to head lower, which does not bode well for stocks in the short term.

On average, when the 200-day is lower, returns suck and volatility explodes in the short to intermediate term. One year later (250 days), however, returns are highest when the 200-day is sloping downward.

I don’t view the 200-day moving average as some magical line. The 180, 210, 220, or 175 day would all tell the same story. These numbers are only averages, of course, so please take all of this with a grain of salt. A long-term moving average only tells you where the market has been, not where it’s going.

Michael Batnick is a managing partner at Ritholtz Wealth Management. He is the co-host of Animal Spirits, What Are Your Thoughts, and The Compound and Friends. For disclosure information please see here.

Get a Full Investor Curriculum: Join The Book List

Every month you'll receive 3-4 book suggestions--chosen by hand from more than 1,000 books. You'll also receive an extensive curriculum (books, articles, papers, videos) in PDF form right away.