The New York Fed just updated its quarterly report on household debt and credit and things are looking

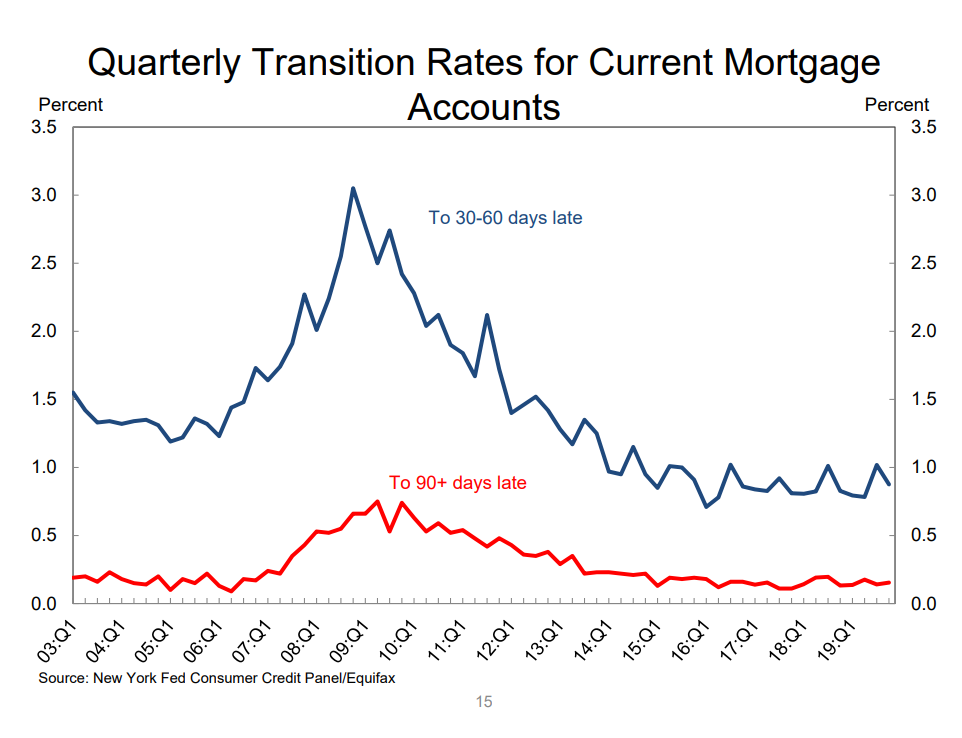

About 1.0% of current mortgage balances became 30 or more days delinquent in 2019 Q4, near the lowest level observed in the data history.

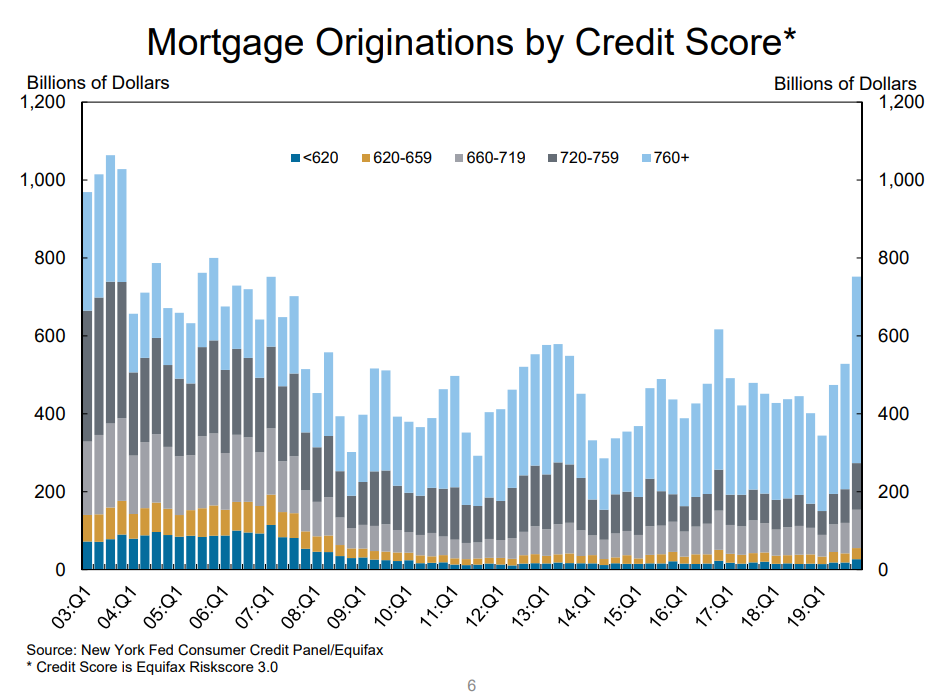

Low interest rates are hurting savers, but they’re helping borrowers. Mortgage originations soared in the fourth quarter, which was driven by borrowers with a very healthy credit history.

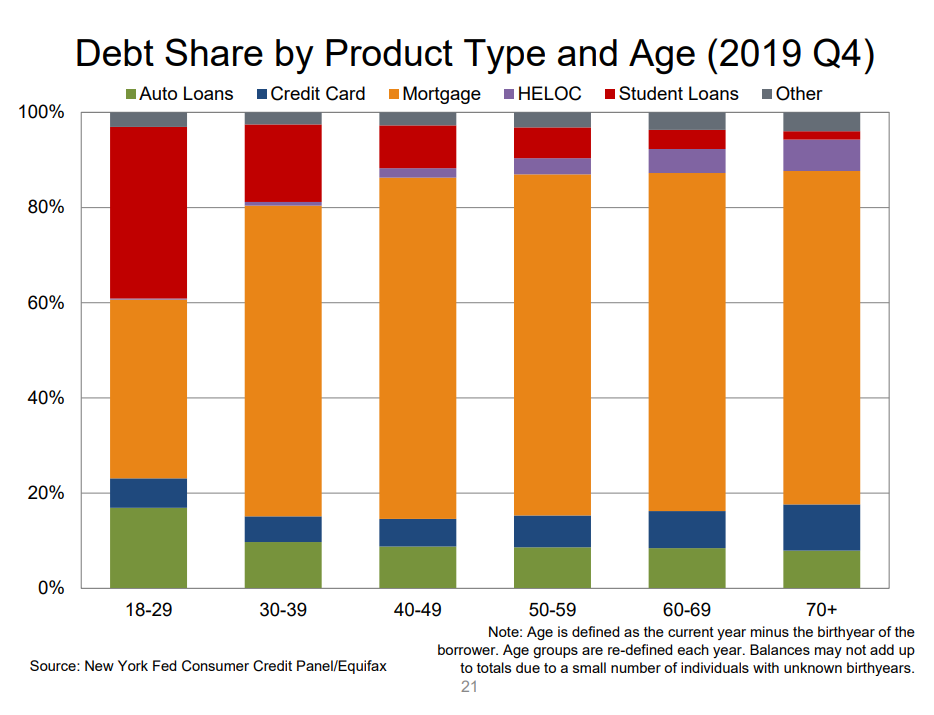

There has been a lot made over the fact that younger people aren’t moving into homes. As of 2015, the home ownership rate of millennials between the ages of 25 and 34 was 37, approximately 8 percentage points lower than the homeowner ship rate of Gen Xers and baby boomers at the same age. Things have gotten a lot better for this age cohort in the last five years.

It looks like people age 18-29 had the highest number of mortgage origination in dollar terms than any time since 2007. The same can be said for older millennials between 30 and 39.

Things aren’t all hunky dorey, as we know young people are burdened by a crushing amount of student loan debt…

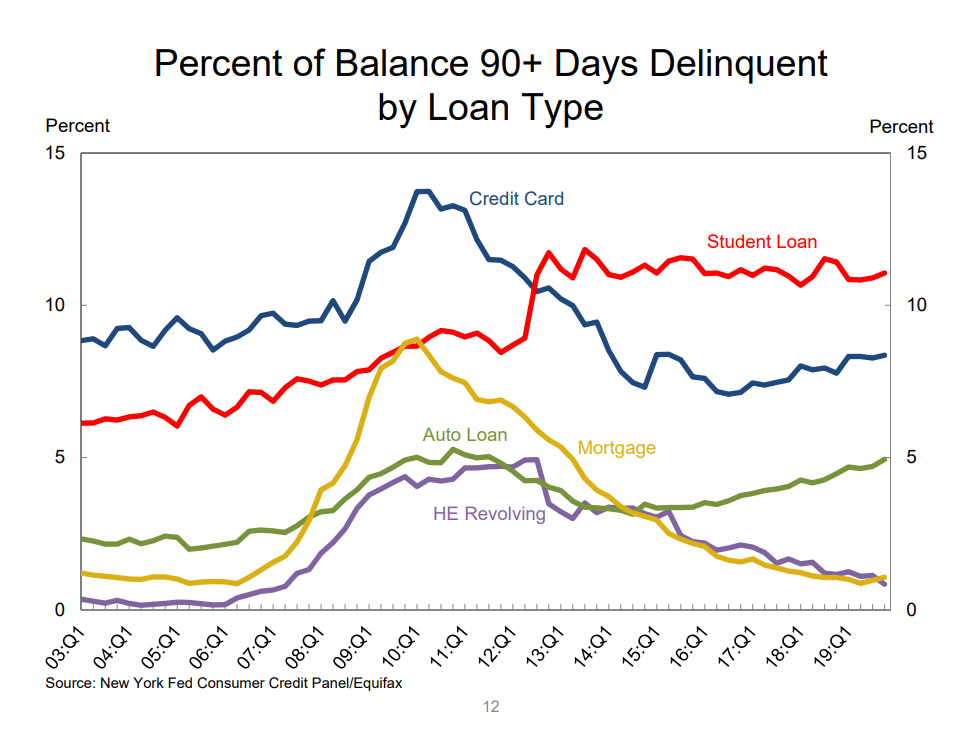

…Which is leading to higher delinquencies. Auto loans are also worth keeping an eye on.

All in all, U.S. borrowers are in very good shape.

Michael Batnick is a managing partner at Ritholtz Wealth Management. He is the co-host of Animal Spirits, What Are Your Thoughts, and The Compound and Friends. For disclosure information please see here.

Get a Full Investor Curriculum: Join The Book List

Every month you'll receive 3-4 book suggestions--chosen by hand from more than 1,000 books. You'll also receive an extensive curriculum (books, articles, papers, videos) in PDF form right away.