In March of 1955, Ben Graham was invited to speak to Congress about the stock market.

They asked him:

When you find a special situation and you decide…that you can buy it for 10 and it is worth 30, and you take a position, and then you cannot realize it until a lot of other people decide it is worth 30, how is that process brought about…what happens?

He said:

That is one of the mysteries of our business, and it is a mystery to me as well as to everybody else. We know from experience that eventually the market catches up with value. It realizes it in one way or another.

How the market catches up with value was a mystery to me until I read a paper called Factors From Scratch, by O’Shaughnessy Asset Management. I remember reading this paper and the visceral reaction I had to it.

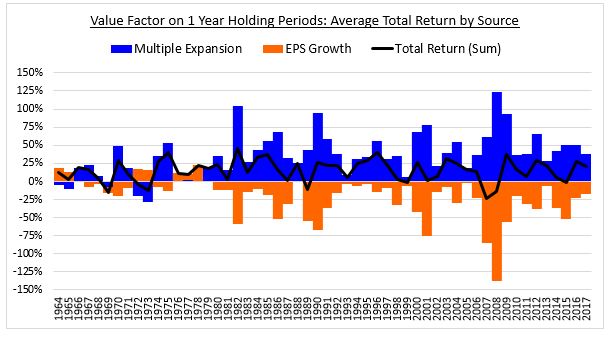

The Value factor generates its returns almost entirely through multiple expansion, shown in blue. The contribution from earnings growth in the underlying companies, shown in orange, is negative in almost every period in the chart. The narrative that value stocks are cheap because they suffer from weak growth is therefore 100% accurate—at least in the near term.

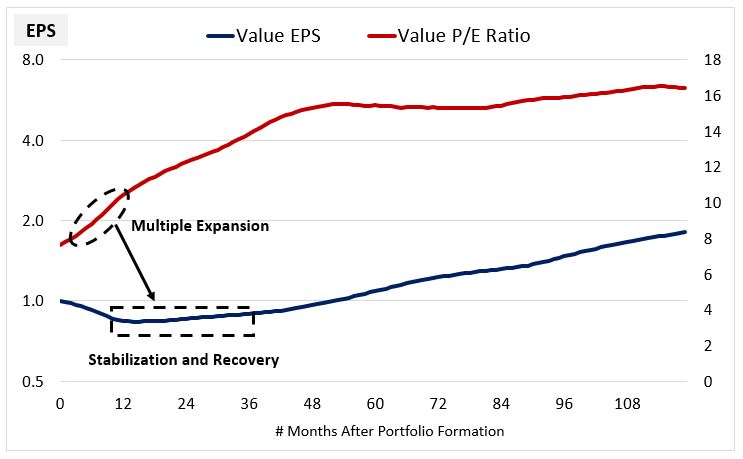

The Value portfolio’s eventual recovery to a normal market growth rate is important because it vindicates the re-rating that takes place earlier in the process. The anticipation of such a recovery is precisely what the re-rating is about–the market sees the early signs of stabilization and improvement in the earnings of Value stocks and upgrades their prices and valuations accordingly. We can see this anticipation clearly in a chart of the average PE ratio and EPS:

Unfortunately, as you well know by now, the process described above has not transpired in a very long time, leading people to once again ask, is value investing dead?

Michael Batnick is a managing partner at Ritholtz Wealth Management. He is the co-host of Animal Spirits, What Are Your Thoughts, and The Compound and Friends. For disclosure information please see here.

Get a Full Investor Curriculum: Join The Book List

Every month you'll receive 3-4 book suggestions--chosen by hand from more than 1,000 books. You'll also receive an extensive curriculum (books, articles, papers, videos) in PDF form right away.