Whenever the growing deficit comes up, you can always count on the following concerns:

We’re going to run out of money

We’re not going to be able to pay this back

We have to balance the budget

We’re destroying the value of our dollar

This is going to cause inflation

A few months ago, Ben Bernanke, former head of the federal reserve was asked,

“The money we’re printing now, will it cause inflation?”

His response, “No.”

It’s becoming more and more accepted that the line we used to draw between money printing and inflation might have been done so with invisible ink. In Stephanie Kelton’s The Deficit Myth, she said, “A deficit is only evidence of overspending if it sparks inflation.”

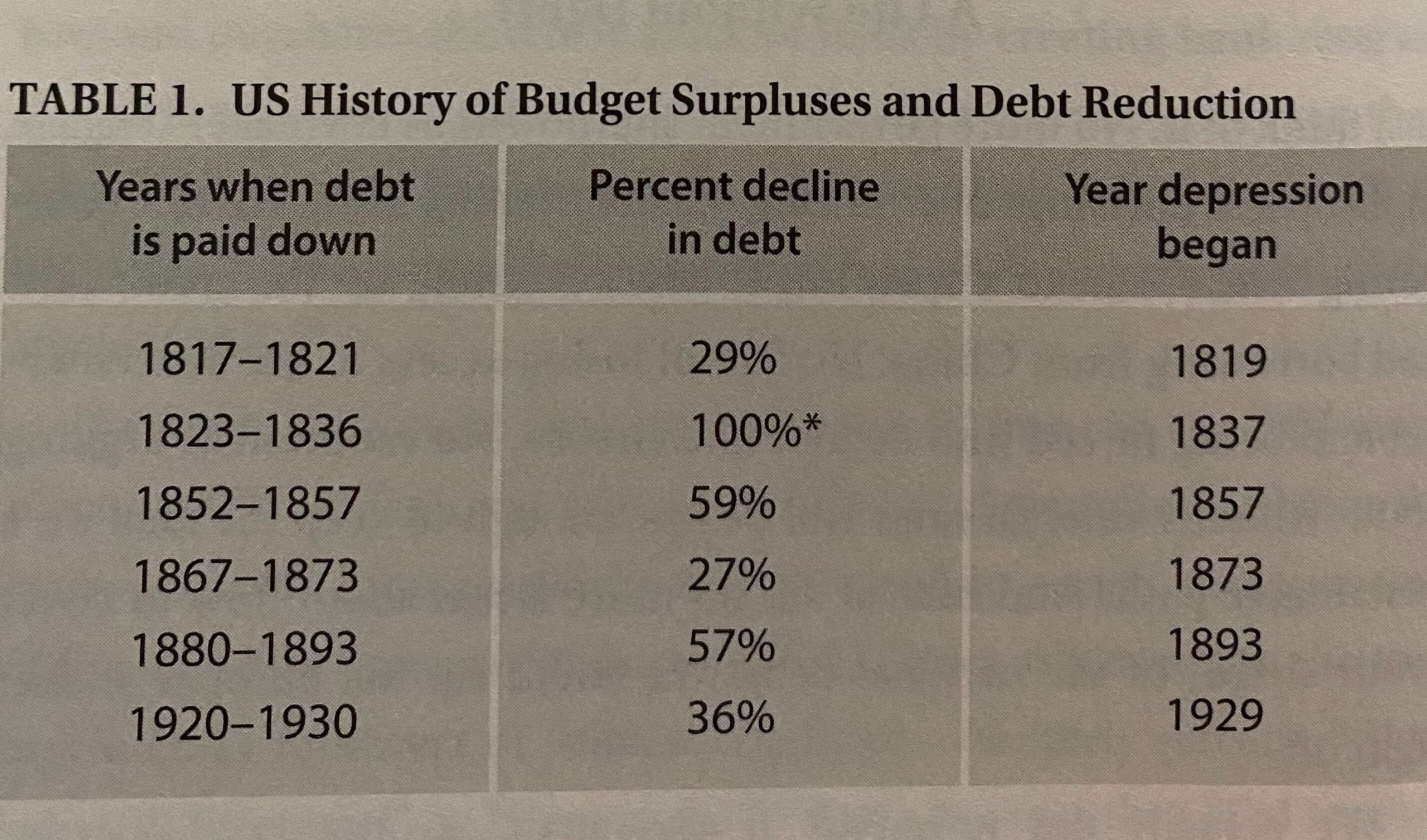

Kelton argues that not only are increasing deficits the wrong boogeyman, but it’s the opposite that should keep us up at night. The periods of history when we paid down our debt coincided with some of the worst economic regimes our country has ever experienced.

Kelton shared a table from professor Frederick Thayer who, in 1996, wrote “the US has experienced six significant economic depressions…each was preceded by a sustained period of budget balancing.”

If we’ve learned anything since the government’s response to the last crisis, it’s that quantitative easing or money printing or whatever you want to call it, does not necessarily plant the seeds for higher prices in the future. If you have any faith in how markets work, then look to our borrowing costs as a clue. If investors were really worried about the size of the federal deficit, than the costs for funding it wouldn’t be at a record low.

One of the reasons that people worry so much about the size of the deficit is because they think of the government like a household. But unlike a household, the government can create more money. Unlike a household the government can keep borrowing. And unlike a household, the bill never comes due.

Michael Batnick is a managing partner at Ritholtz Wealth Management. He is the co-host of Animal Spirits, What Are Your Thoughts, and The Compound and Friends. For disclosure information please see here.

Get a Full Investor Curriculum: Join The Book List

Every month you'll receive 3-4 book suggestions--chosen by hand from more than 1,000 books. You'll also receive an extensive curriculum (books, articles, papers, videos) in PDF form right away.