There is a lot of liquidity out there. Andreesen Horowitz announced that they raised a fresh $9 billion to invest in their venture, growth, and bio funds. Today, FTX announced the launch of a $2 billion venture fund.

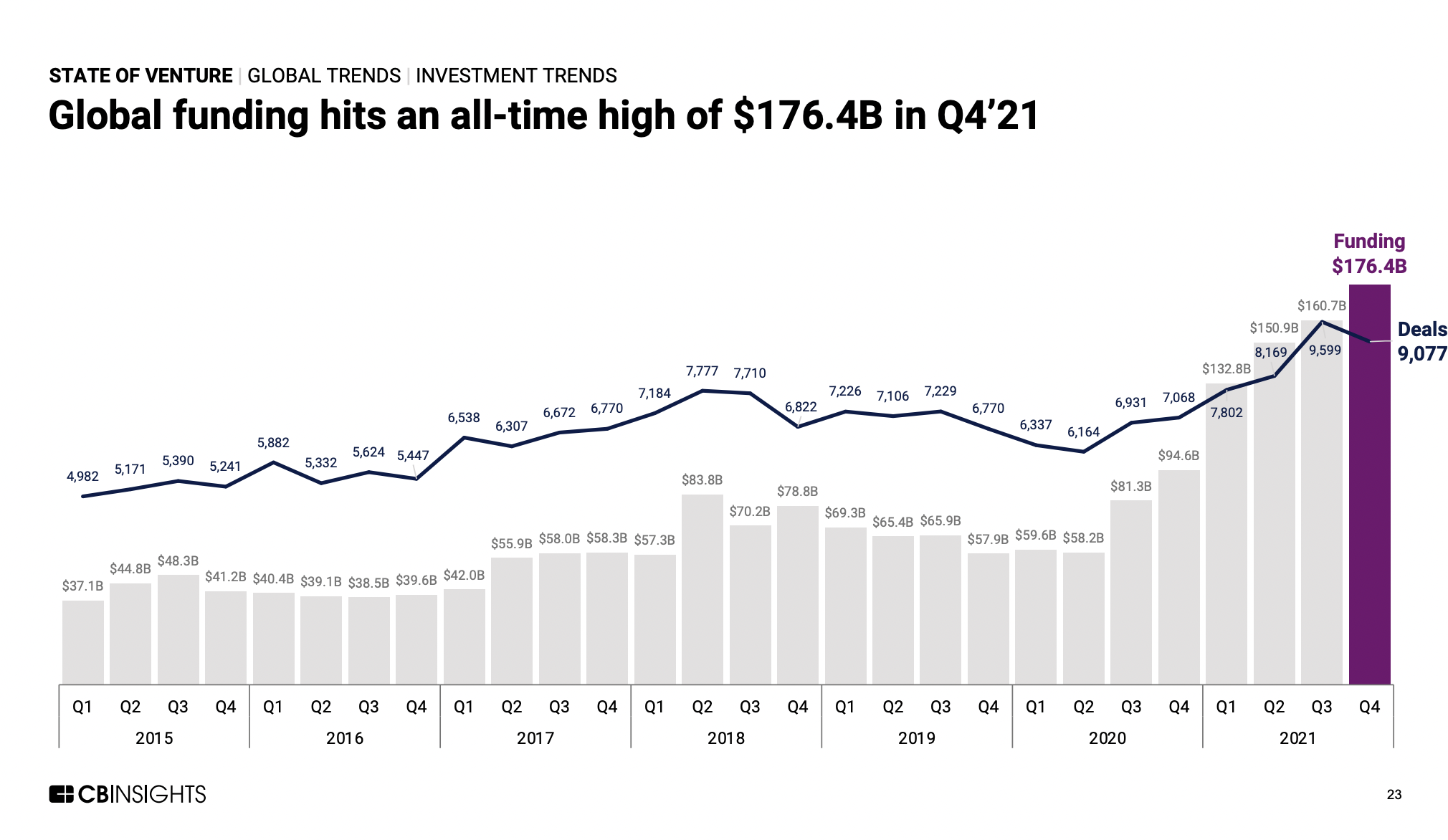

CB Insights just published their State of Venture 2021 report and all arrows point in the same direction higher.

Global funding hit an all-time high in the 1st, 2nd, 3rd, and 4th quarters of 2021.

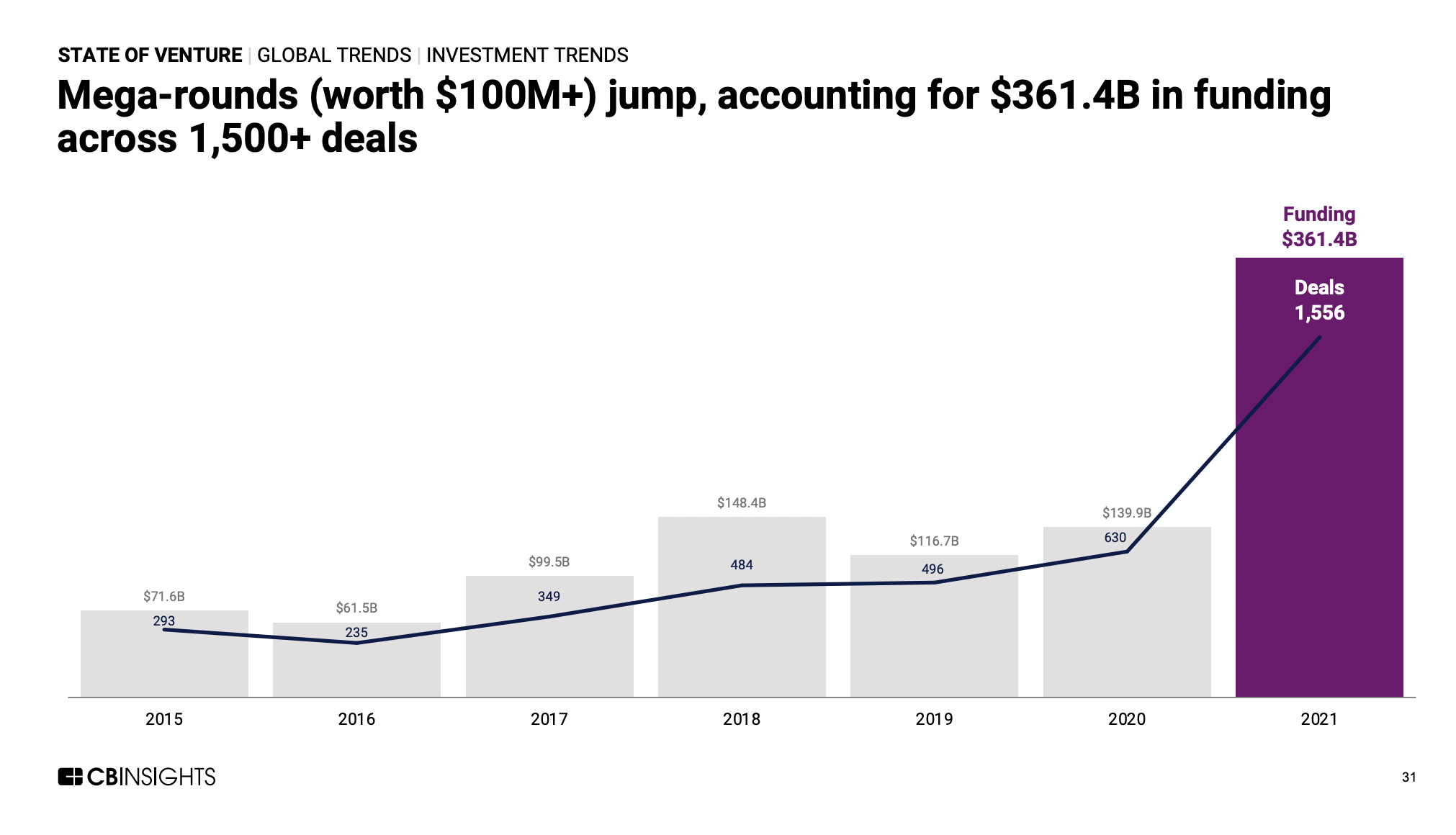

As depth and liquidity continue to build in private markets, the deal sizes keep getting bigger.

There were more than twice as many mega-rounds in 2021 than there were in 2020. Funding for these behemoths clocked in at $361 billion last year, up 160% from 2020.

Companies are raising more money these days for many reasons, the biggest one being the speed at which they can go from zero to $1 billion. The average time from first funding to unicorn status is just 55 months. Companies are moving quicker than ever before, and so are their investors. Tiger Global basically did a deal a day last year.

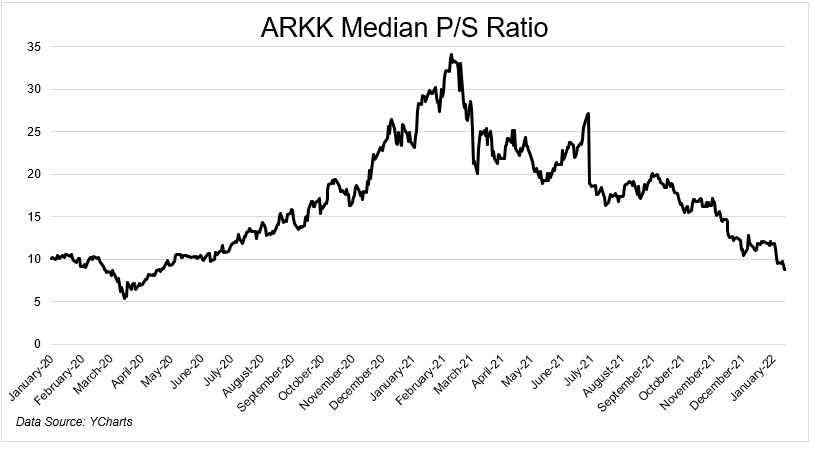

The big question I have now is, how long can private market multiples stay elevated while young public companies compress? The median ARKK holding traded for 33x sales in early ’21. Today it’s 9x.

As public market investors deal with inflation and brace for interest rate increases, they’re rethinking the amount they’re willing to pay per dollar of revenue. How long before this reaches private markets?

There is almost certainly a tipping point, but I think this dichotomy can last longer than most people think. There’s too much money chasing too few deals in private markets, and I’m not sure an interest rate hike or two will change that.*

Michael Batnick is a managing partner at Ritholtz Wealth Management. He is the co-host of Animal Spirits, What Are Your Thoughts, and The Compound and Friends. For disclosure information please see here.

Get a Full Investor Curriculum: Join The Book List

Every month you'll receive 3-4 book suggestions--chosen by hand from more than 1,000 books. You'll also receive an extensive curriculum (books, articles, papers, videos) in PDF form right away.