The world has turned upside down, or right side up, depending on your perspective. Everything that worked during the pandemic is unraveling on the other side of it.

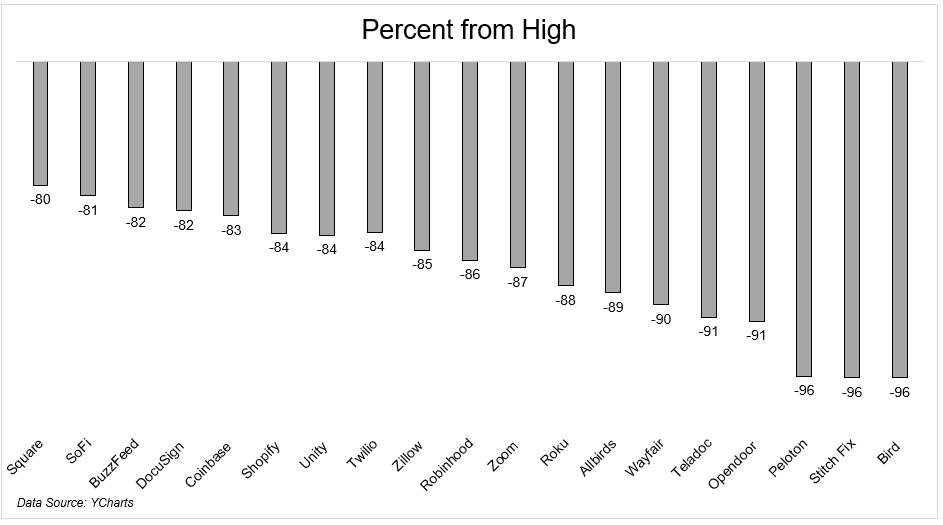

Nose bleed valuations are getting knee clubbed by a combination of high inflation and rising interest rates. These darlings of 2020 are down 80% or more from their all-time high.

It’s tempting to try and catch a bottom in exciting names that are down so much. But the chart above should be illustrative of the dangers in trying to do that.

“Teladoc is down 91%. How much worse can it get?” You might look at Peloton or Stitch Fix which are down 96% and think the gap between -91 and -96 is not that wide. You would be wrong. David Einhorn once said “What do you call a stock that’s down 90%? A stock that was down 80% and then got cut in half.” For a stock to go from down 91% to down 96% it would have to fall another 55%!!!

It’s unwise to average down into crashing growth stocks. If you’re going to play that game, it’s best to have an exit strategy. Averaging down into declining indexes tends to have a better outcome, but it can still be a painful process. There’s nothing worse than thinking a bear market is over only to have the rug pulled out from underneath your legs.

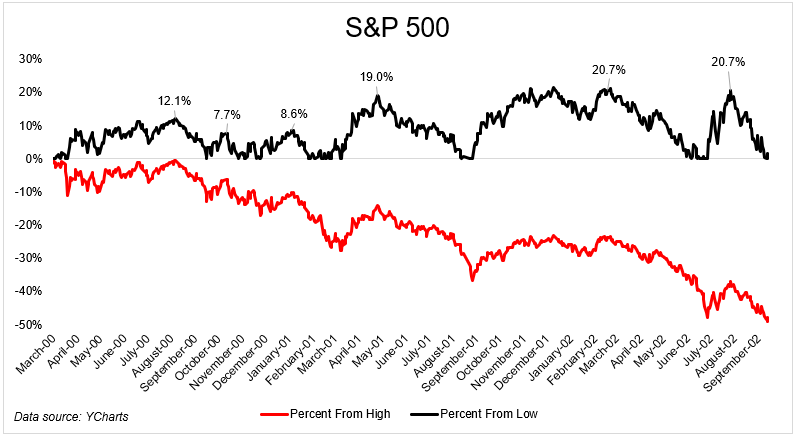

Look how many times that happened during the bursting of the dotcom bubble. Three separate ~20% rallies that would go on to make new lows. Just when you thought the worst was behind you, you got blindsided by more selling.

We just experienced an unpleasant version of this in the S&P 500 over the summer. Stocks bounced 17% from the bottom and retraced more than 50% of the losses. We know what happened next.

So, what would we need for stocks to find a bottom that sticks? We spoke about this with one of the top technicians in finance, Katie Stockton. We covered her process, market internals, and her new ETF TACK. Hope you enjoy and have a nice weekend.

Michael Batnick is a managing partner at Ritholtz Wealth Management. He is the co-host of Animal Spirits, What Are Your Thoughts, and The Compound and Friends. For disclosure information please see here.

Get a Full Investor Curriculum: Join The Book List

Every month you'll receive 3-4 book suggestions--chosen by hand from more than 1,000 books. You'll also receive an extensive curriculum (books, articles, papers, videos) in PDF form right away.