Eight days before the market bottomed in July 1932, Ben Graham wrote an article in Forbes, Should Rich But Losing Corporations Be Liquidated? In it he wrote, “More than one industrial company in three selling for less than its net current assets, with a large number quoted at less than their unencumbered cash.” At a time when the CAPE ratio was just above 5, many businesses were worth more dead than alive.

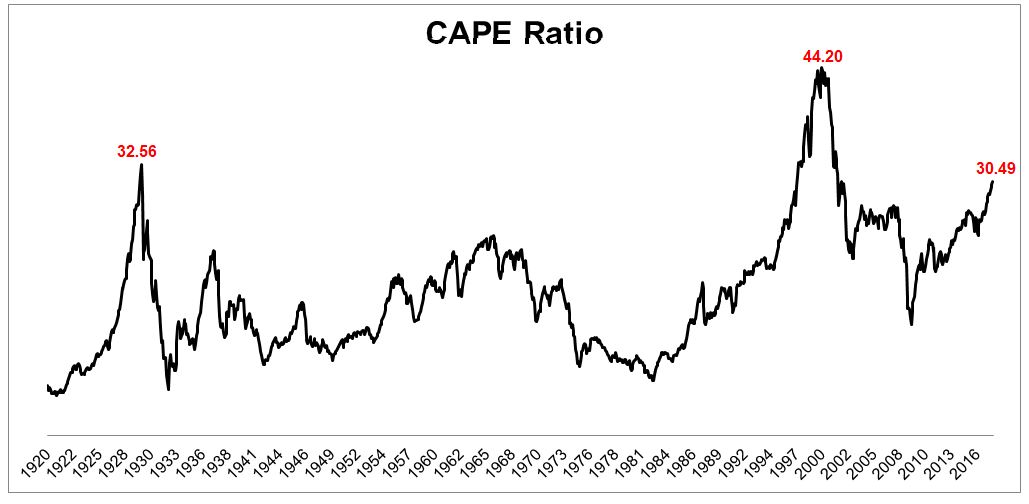

In the ten-years leading up to the crash in 1929, the CAPE ratio went from a low of 5.02 up to 32.56. Today, it’s as close to the 1929 peak as it’s ever been, with the exception of the late 1990s. “The CAPE ratio in the United States has never gotten above 30 without a subsequent market crash” would be a true statement. Perhaps misleading, with a sample size of two, but true nonetheless. So is it possible that today is 1929 redux?

What would have to happen for companies to be selling for less than their net current assets? I don’t have the slightest idea. An asset bubble built on the back of artificially low rates seems like the obvious answer, so that can’t be right, but if it is, I warned ya. But honestly, for the market to fall 90%, I’m thinking aliens, an asteroid, or another world war seem the most likely culprits.

The aftermath of the depression was a gold mine for value investors. Well, really for any investors, but for those that measured intrinsic value, it was nearly impossible to miss. From The White Sharks of Wall Street:

Here was a company being offered for sale for less than the cash in its pocket! All a fellow had to do was borrow the purchase price, buy the company, and use the company’s own cash to pay off the loan- it was like getting the company for free. Why wasn’t everyone lining up to bid against him? The answer lies partly in the psychological baggage that American industry carried out of the Depression. Despite the almost unprecedented prosperity brought by government wartime contracts, many American business leaders believed that the nation would slide promptly back into a depression the moment the war was over. A gamble on the scale that Evans was prepared to take was simply unthinkable for most of them. The engine for the deal, after all, was debt. And going into debt to finance a speculative venture- well, wasn’t that what the 1920s had been about? And didn’t it end very badly?

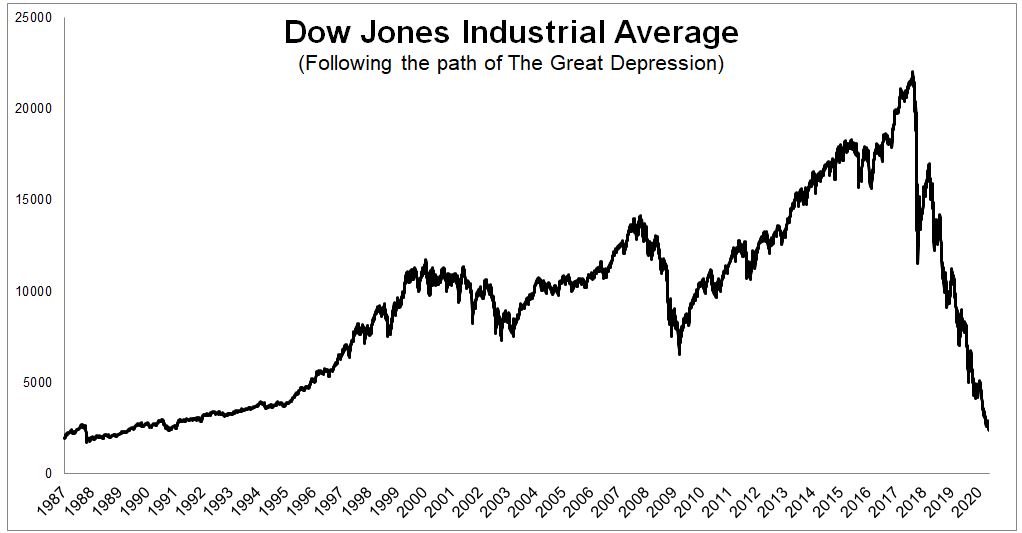

A Great Depression style crash would take the Dow back to where it was in May, 1989, wiping out 28 years of gains (not including dividends).

What would a 21st century bargain look like? Let’s use Amazon as an example. According to data compiled from Ycharts, Amazon’s net current assets are $2.061 billion. If you could purchase Amazon for this price, each share would cost you $4.29, down from the $994 its currently trading at; a cool 99.57% discount. This sounds absurd and unimaginable. The latter it is, the former it is not.

In October 2008, Jason Zweig wrote an article, What History Tells Us About the Market . In it, he shared that depression style discounts were not just a thing of the past. Charles Schwab Corp had a market capitalization of $28.8 billion, while holding $27.8 billion in cash. There were 875 other stocks that traded below the value of their per-share holdings of cash.

U.S. stocks have a valuation that is in line with two of the biggest market peaks of all-time, so if this is 1929, it will be a nightmare for this generation, and a gift for future ones. And while I can’t imagine a scenario that takes us to Dow 2,400, Dow 15,000, a 32% decline, seems well within the realm of possibility.

Josh Brown nails the mindset that we should take with respect to market risks: “We should always invest as though the best is yet to come but the worst could be right around the corner.”