“Home prices are not in a bubble. It’s not like people are collecting houses. These are first-time home buyers! The rise in prices was fueled by Covid, low interest rates, and most importantly, demographics. Are prices red hot? Yes. Is this a bubble that will pop? No.”

This has been my take on housing for the past few months on the podcast. I still stand by those sentiments, but one part of that statement is flat out wrong. This is not just first-time home buyers.

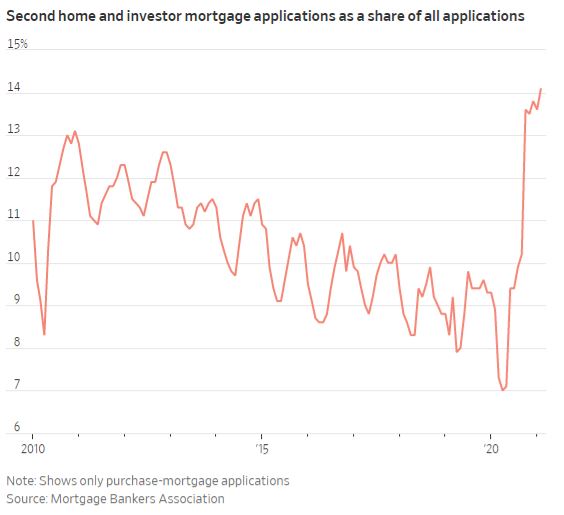

Buyers attempting to snag second homes and investment properties accounted for 14% of all purchase-mortgage applications in February, a record in data going back more than a decade, according to the Mortgage Bankers Association, a trade group.

It makes sense that second home purchases are booming. People who can afford two properties have largely been unaffected over the last year, at least from a financial perspective. These people will probably never go back to the office five days a week, so if you can work from anywhere, you might as well work somewhere with a pretty view and maybe even a pool.

I feel for first-time homebuyers who have been priced out of the market. Ben and I get a few emails every week from people in this situation who are looking for advice. Unfortunately, I think the train has left the station. There are 70 million Millennials, and only 48% of them own a home, which is the lowest of any generation. Gen-X is 69% for comparison.

Rising interest rates would likely slow the rise in prices, but I’m not convinced that it would crash the market. And even if rising rates do cause home prices to pull back, that might help with your down payment, but it would hurt your monthly payment.

We’re still so scarred from the housing bubble that people are seeing this as version 2.0. I don’t think this is the case. There’s a difference between rising prices that need to cool off and rising prices that are going to crash. Homebuyers should prepare accordingly.

Michael Batnick is a managing partner at Ritholtz Wealth Management. He is the co-host of Animal Spirits, What Are Your Thoughts, and The Compound and Friends. For disclosure information please see here.

Get a Full Investor Curriculum: Join The Book List

Every month you'll receive 3-4 book suggestions--chosen by hand from more than 1,000 books. You'll also receive an extensive curriculum (books, articles, papers, videos) in PDF form right away.