559 days ago, the fed began a rate hiking cycle that would be unlike anything the modern investor had ever seen.

The stock market saw this coming. When they finally decided they needed to fight inflation, micro-cap stocks were in a 19% drawdown. The Nasdaq-100 had fallen 16% from its peak.

The indices would fall further still as investors digested what higher rates would mean for the economy and the companies that underlie it.

The markets discounted a lot of bad news that ultimately did not come to pass: a slower economy, higher unemployment, and much lower earnings, to name a few. As a result of this and other factors, like the advent of AI, stocks had a heck of a rally. The Dow Jones Industrial Average hit a new all-time high on a total return basis, and the S&P 500 came within 2% of doing the same.

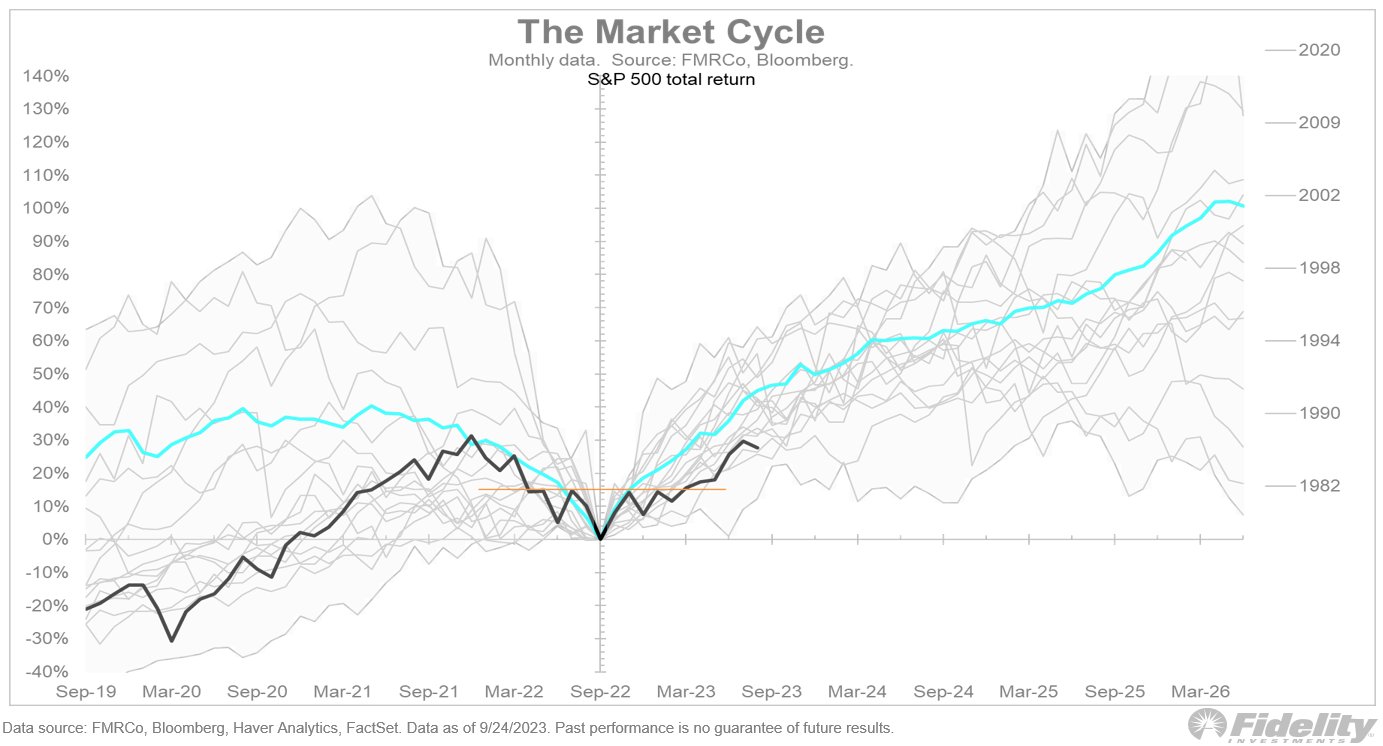

And while the rally from the lows last fall certainly feels good, it has been underwhelming relative to historical rallies off of stock market bottoms.

Jurien Timmer tweeted a chart showing where the current rally stacks up compared with previous ones. Pretty underwhelming.

To make matters worse, as everyone is painfully aware of by now, the rally has been concentrated in the mega-cap stocks. If you look under the hood, the rally goes from underwhelming to downright lousy. Small-cap stocks are flat since the Fed started raising rates. Micro-cap stocks are down 3%.

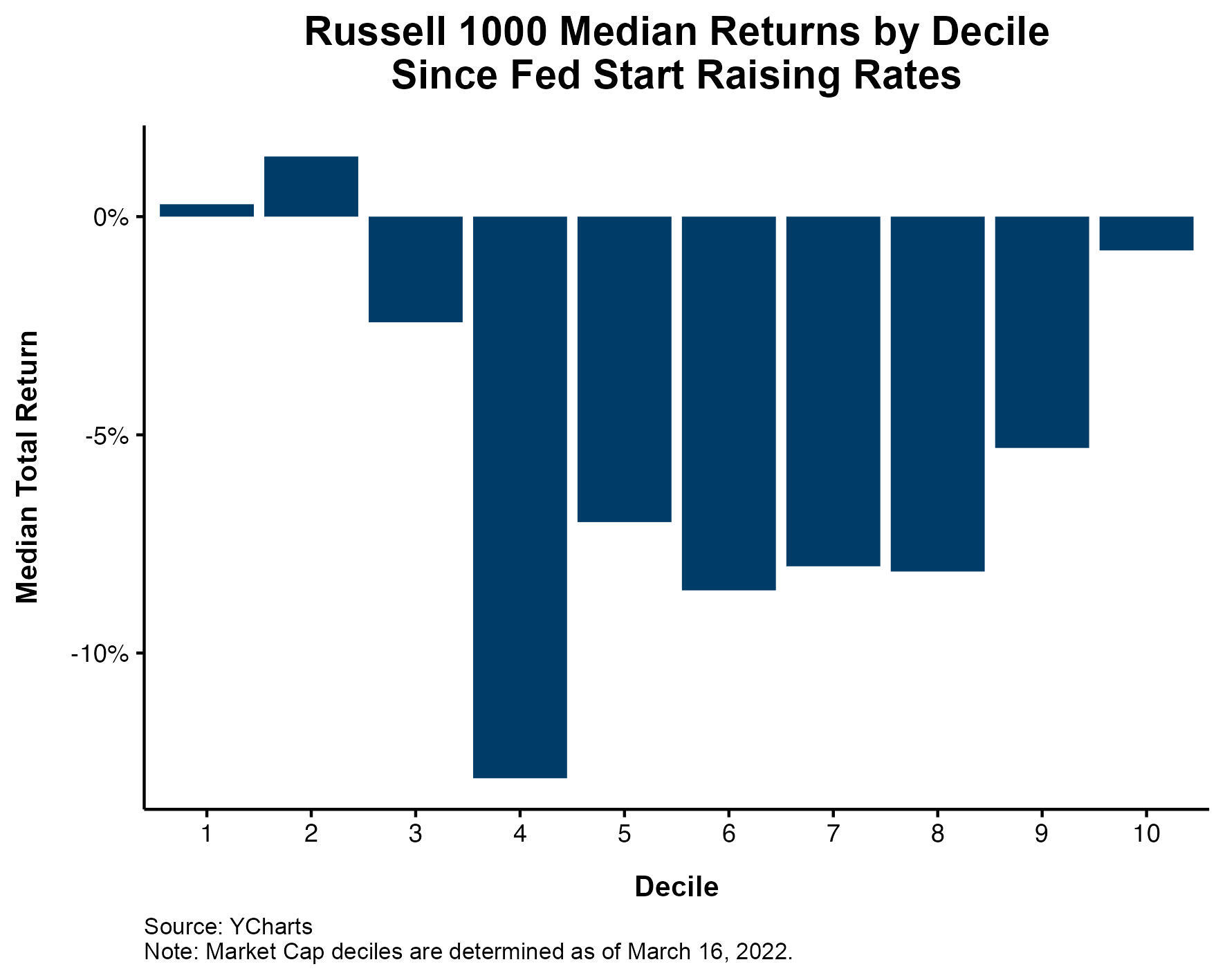

If you dissect the Russell 1000, you can see that the median stock in every decile, save the two largest, has a negative return since March of last year, as you can see from this chart courtesy of Nick Maggiulli.

The flip side of this is that the stock market is doing pretty okay, considering everything that’s been thrown at it over the past year and a half.

Josh and I will be hitting on this and much more on tonight’s What Are Your Thoughts?

Michael Batnick is a managing partner at Ritholtz Wealth Management. He is the co-host of Animal Spirits, What Are Your Thoughts, and The Compound and Friends. For disclosure information please see here.

Get a Full Investor Curriculum: Join The Book List

Every month you'll receive 3-4 book suggestions--chosen by hand from more than 1,000 books. You'll also receive an extensive curriculum (books, articles, papers, videos) in PDF form right away.