Nobody likes to overpay, whether it’s for food, clothing, a house, or stocks.

The problem is people don’t treat stocks the way they do a car, groceries, or jeans. If a cucumber goes from $2 to $10, you wouldn’t say “wow, I need to buy some before it goes to $20.” You would simply substitute it for another vegetable. However, if a stock rose 400% there are plenty of people who would pile on, anticipating a greater fool will come along after them.

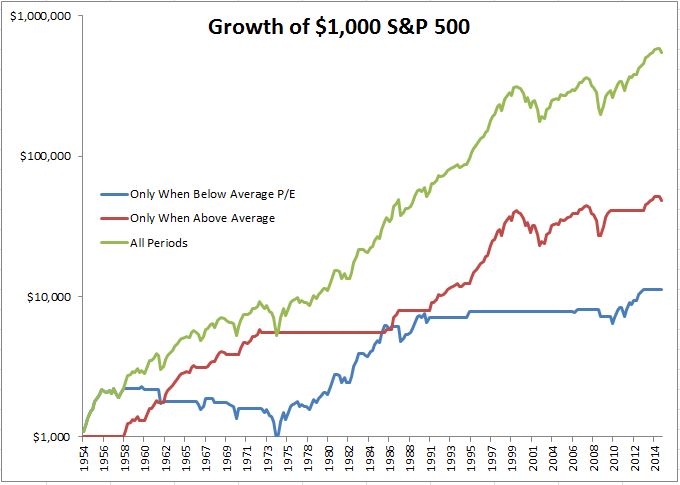

But what if you were able to maintain discipline and not be the greater fool. What if you were able to invest in stocks only as they went on sale?

Let’s conduct a hypothetical exercise. Imagine an investor who only held stocks when they were trading below their average long term price-to-earnings ratio of 16.3. This is hypothetical because of course you would not have known before hand what the trailing P/E was. Be that as it may, let’s say that somebody did possess this power. What would their results be? Well, the chart below speaks volumes. Not only would you have been better investing the entire time, but you would have been better off investing in the S&P 500 when it was expensive versus when it was cheap.

For all periods from 1954-today, the S&P 500 compounded at 10.7%. When the P/E was above average, stocks compounded at 6.5% and they compounded at 4% when the P/E was below average.

The average quarterly return for all periods was 2.9%. The average quarterly return when the P/E was above average was 3.3% and just 2.4% when the P/E was below average.

Does that mean that investing only when stocks are expensive is a good idea? Well clearly not, just look at the chart. In defense of investing when stocks are on sale, returns one year later when they were at a below average P/E was 17%, compared to just 7% when they were above average.

The takeaway is that valuations cannot be viewed in a vacuum. There are all sorts of other important inputs into stock returns; earnings, GDP, interest rates, and inflation, to name a few. Valuations absolutely play an enormous role, but investors who refuse to play ball when they don’t find stocks attractive might be doing themselves a great disservice.

Michael Batnick is a managing partner at Ritholtz Wealth Management. He is the co-host of Animal Spirits, What Are Your Thoughts, and The Compound and Friends. For disclosure information please see here.

Get a Full Investor Curriculum: Join The Book List

Every month you'll receive 3-4 book suggestions--chosen by hand from more than 1,000 books. You'll also receive an extensive curriculum (books, articles, papers, videos) in PDF form right away.

Please run the same kind of analysis for holding stocks only when interest rares are below average vs when above.