The thing about biases is that they’re human, so they’re seen in every walk of life. In who we choose to be friends with, in what news we read, in investing, and in sports.

In Michael Lombardi’s new book Gridiron Genius, which I highly recommend, he talks about all of the biases that can infect a football organization. Lombardi says, “Confirmation bias is absolutely insidious in my field even though it breaks the first rule of scouting: Never begin with the end in mind.” He also talks about what he calls “scouting blinders”, which is the tendency for drafted players to stick around long after the initial evaluation proved to be wrong. Lombardi tells a story about how this affected the great Al Davis. “Like many crimes, the cover-up is even worse than the initial mistake. When it came to players Al Davis discovered, there was no like, only love, and when he loved, he loved forever.”

When we buy a stock, a few biases instantly kick in. We value it more than we did before we owned it (endowment affect), we look for reasons to support our purchase (confirmation bias) and perhaps most pernicious, we anchor to the purchase price.

Let’s look at Amazon as an example. If somebody bought Amazon in 2009, this is what their experience looks like. They see their gains from the initial purchase price each time they open their account.

But with stocks, there are multiple anchors. Another thing we anchor to is the all time high. So we don’t just see how much we’re up from out initial purchase, we see how much we’re down from its highest value.

Anybody who has ever been in a drawdown knows that they’re not viewed in percentage terms, but dollar terms. If you put $10,000 into Amazon in 2009, on eleven occasions, you had a decline that was larger than your initial investment.

Anybody who has ever been in a drawdown knows that they’re not viewed in percentage terms, but dollar terms. If you put $10,000 into Amazon in 2009, on eleven occasions, you had a decline that was larger than your initial investment.

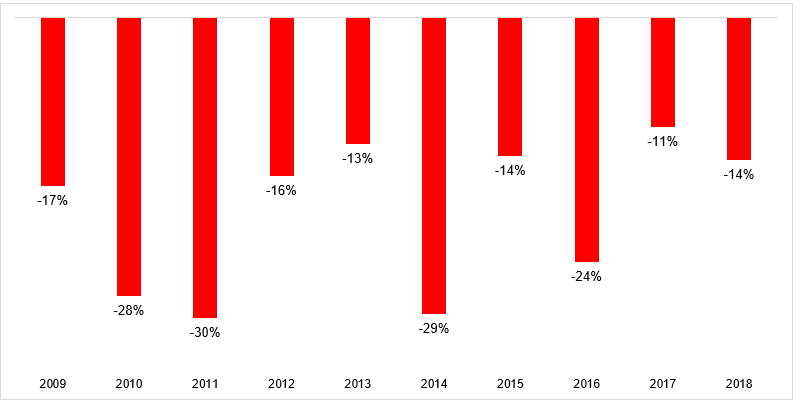

The third and final anchor is January 1st of every year. Each time the calendar turns over, we revert to the YTD performance. As if how long it takes the earth to revolve around the sun has any bearing on anything, but these are how biases work. The chart below shows the max intra-year drawdown for Amazon.  When you think about how easy it is to anchor, and how hard it is to think long-term, you realize how silly the if you invested $10,000 meme really is.

When you think about how easy it is to anchor, and how hard it is to think long-term, you realize how silly the if you invested $10,000 meme really is.

The best way to guard against the anchor is to think about the investment merits today. In other words, if you had to start over, would you still hold it? To do this objectively might be wishful thinking, which is why biases are so difficult to overcome. Just being aware of their existence does not necessarily guard you against falling victim to them. I don’t have any silver bullets here, but I’ll leave you with some wise words from Adam Smith:

A stock is for all practical purposes, a piece of paper that sits in a bank vault. Most likely you will never see it. It may or may not have an Intrinsic Value; what it is worth on any given day depends on the confluence of buyers and sellers that day. The most important thing to realize is simplistic: The stock doesn’t know you own it. All those marvelous things, or those terrible things, that you feel about a stock, or a list of stocks, or an amount of money represented by a list of stocks, all of these things are unreciprocated by the stock or the group of stocks. You can be in love if you want to, but that piece of paper doesn’t love you, and unreciprocated love can turn into masochism, narcissism, or, even worse, market losses and unreciprocated hate.

Lombardi tells some great stories about his time with the legends Bill Walsh, Al Davis, and Bill Belichick. Even if you’re not a football junkie, there’s something in here for you. You can pre-order Gridiron Genius today