If you told me in March that in less than 100 trading days, the S&P 500 would be back near all-time highs, I would not have believed you.

2020 is teaching investors a lesson that should be apparent to all of us who watch the market closely; it is full of surprises.

The best way to plan for surprises is to be ready for a wide range of outcomes.

For example, when thinking about what stocks are going to do over the next ten years, there are four destinations, with an unlimited set of paths.

Maybe we get lower returns, as many, myself included are expecting.

Maybe we get historical, average returns.

Maybe we get the worst returns we’ve ever seen.

Or maybe the next decade looks like the last and we continue to see above average returns.

We should be prepared for surprises, but we shouldn’t let them guide us. When thinking through what the future might look like, it’s helpful to look at the past. The worst returns we’ve ever seen are possible, but are they likely? And based on what? And how bad can it get?

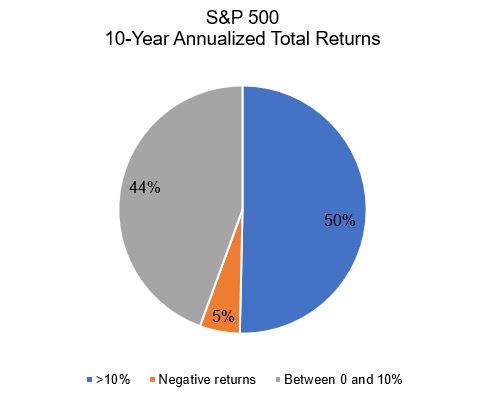

95% of the time, stocks delivered a positive nominal return, and the worst 10-year period ever saw stocks fall 5% a year.

But be careful of taking these numbers too literally, because history only shows us what has happened, not what can happen.

Prior to this year, you would have concluded that the likelihood of the stock market falling 30% in five weeks are zero. It never happened until it happened.

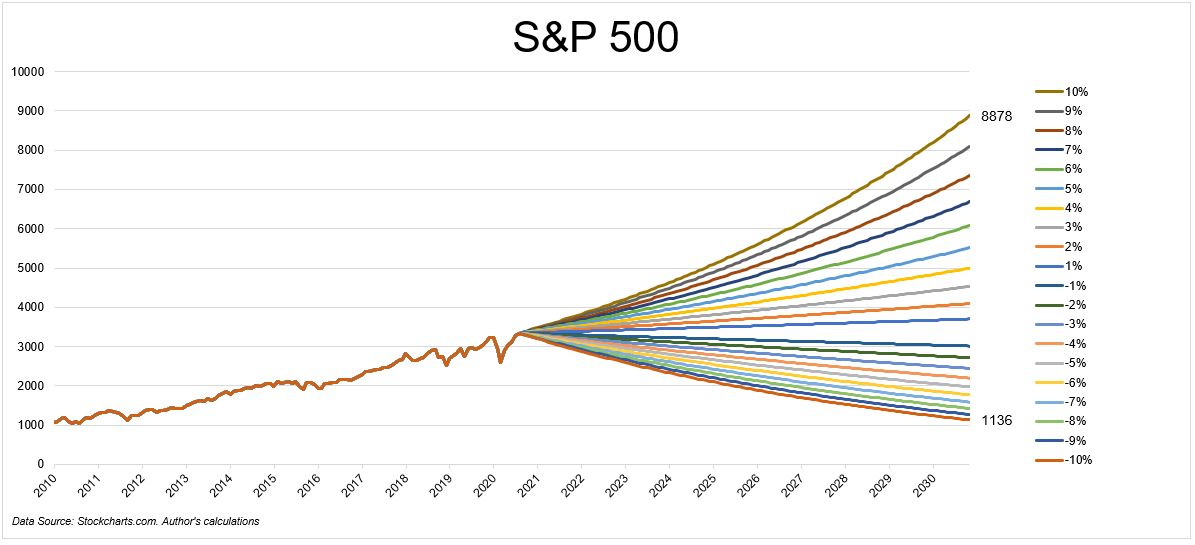

The chart below shows a wide range of outcomes over the next ten years, assuming the market does between -10% and +10% annually for the next ten years.

Stocks have never lost more than 5% a year for 10 years, so some of the lower lines might look completely ridiculous. Okay, and what word would you use to describe a year where the economy closes for four months and the stock market is positive?

Good investing is about preparing for base rates and being able to live with surprises. Easy to write, hard to do.

I’ll give the last words to Morgan Housel, who in his excellent new book, writes:

History is mostly the study of surprising events. But it is often used by investors and economists as an unassailable guide to the future. Do you see the irony? Do you see the problem?

Michael Batnick is a managing partner at Ritholtz Wealth Management. He is the co-host of Animal Spirits, What Are Your Thoughts, and The Compound and Friends. For disclosure information please see here.

Get a Full Investor Curriculum: Join The Book List

Every month you'll receive 3-4 book suggestions--chosen by hand from more than 1,000 books. You'll also receive an extensive curriculum (books, articles, papers, videos) in PDF form right away.