Market predictions are silly. We all learned this a long time ago. But that doesn’t mean they’re completely worthless. Even though forecasts are almost always wrong, they can be entertaining and educational. That’s all I’m trying to do with this post. Entertain and educate. Needless to say, but I have to say it anyway, nothing in this list is investment advice. I’m not doing anything with my portfolio based on these predictions, and neither should you.

Here is my list from a year ago. I got some right and a lot wrong, which is hardly a surprise. I expect my predictions to have a terrible track record, and that’s why I try to ride the market rather than outsmart it. So why am I doing this? Well, it’s fun to look back on what you thought was possible a year ago. When you see that you were so off on some things, it reminds you just how difficult it is to predict the future. I also learn a lot by doing this. I uncovered some things that I didn’t know or forgot I knew. So with that, these are my ten predictions for 2023.

- Bonds hold their own as a diversifying asset

- Tech continues its layoffs

- Jeff Bezos returns to Amazon

- The IPO market remains frozen

- Value Outperforms Growth Again

- Gold makes a new all-time high

- The Housing Market Doesn’t Crash

- International Stocks Outperform

- Bitcoin gains 100%

- Energy stocks continue to outperform

- Bonus. The market avoids a recession, and stocks gain double digits.

Bonds hold their own as a diversifying asset.

I’m usually of the opinion that even if you were given the news in advance, you wouldn’t know how the market would react. 2022 was the exception. If you knew ahead of time that inflation would do what it did, and that the Fed would raise rates seven times to combat it, you would have gotten a lot of things right.

Inflation is poison for bond investors for two reasons. It inflates away the value of the fixed income, and it crushes the price of that instrument as interest rates rise alongside consumer prices. Last year was brutal for the bond market, and to make matters worse, that happened during a year when stocks also got creamed. U.S. bonds have historically done well when stocks got dinged but last year proved once again that very few iron laws exist in finance. This isn’t physics.

The average annual return for bonds since 1976 when the S&P 500 fell on the year (N=8) was 6.7%. Bonds were positive every year stocks fell except for last year when rising yields (lower bond prices) in combination with higher prices drove stocks lower.

The 10-year treasury went from an all-time low in 2020 to the highest levels in over a decade in fairly short order. That was painful, but the good news is we got it over with. You can’t go from 50 basis points to 4% again next year. So, if stocks have another rocky year, bonds should do okay. Even if interest rates were to rise, lowering prices, at least we’ve got the fixed income component to cushion the blow.

Tech continues its layoffs

When Facebook bought Instagram for $1 billion, the company had just eleven employees. Nearly a decade later, it’s pushing 20,000. ‘

One of the most impressive parts of the boom in technology over the past decade is the amount of revenue that flowed through to the bottom line. That all changed in 2022, as outlined in this interesting thread from Jesse Livermore. He shows that the underperformance of FANMAG was largely a result of profit margin compression. With the explosive growth in headcount over the past couple of years, the layoffs in tech that we heard about in 2022 will continue into 2023 at all levels, from startups to incumbents.

What Elon Musk did at Twitter will work as a blueprint for 2023. It won’t be as extreme as what he did, but it will be a green light for other companies to follow similar steps. Last year, 1,013 tech companies laid off 153,160 employees. That trend will continue in 2023.

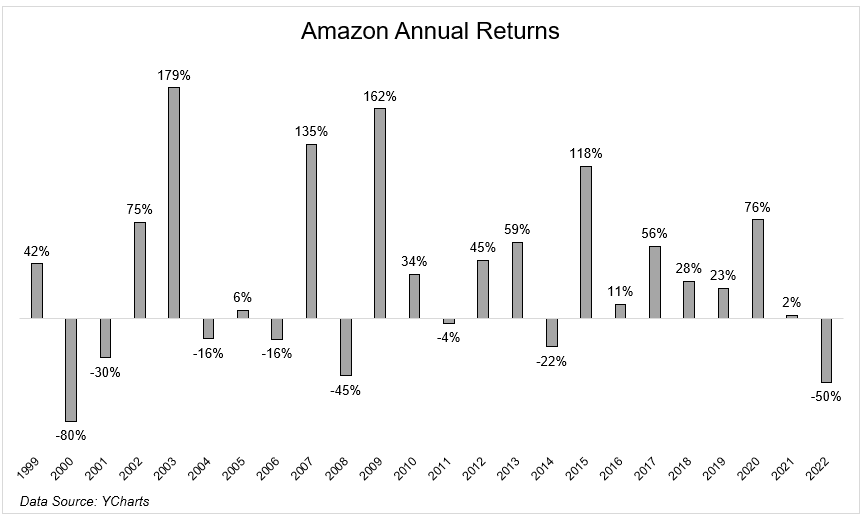

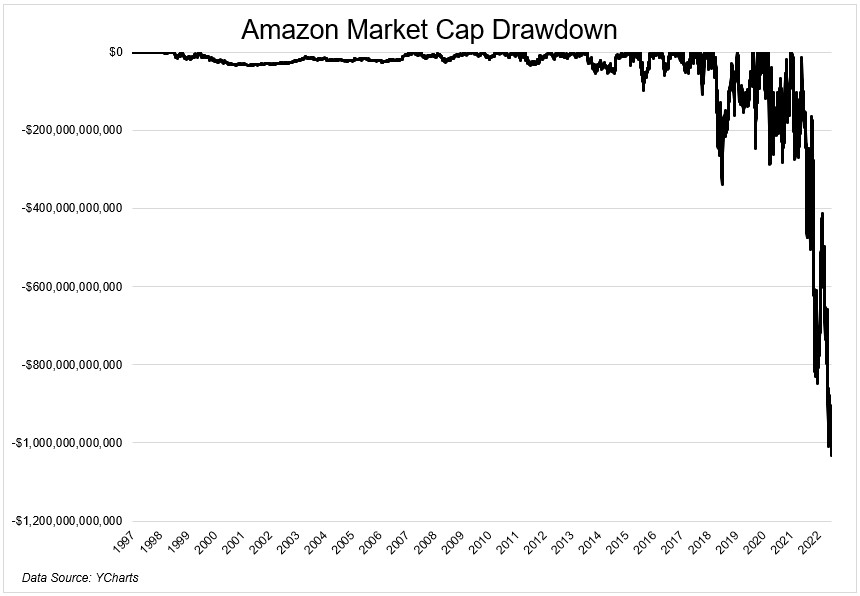

Jeff Bezos returns to Amazon

Amazon experienced its largest share price decline on an annual basis since the dot-com bubble burst.

Yes, Amazon has seen worse drawdowns, but when it peaked during the dot com bubble on its way to a 90%+ decline, it had a market cap of $36 billion. It lost more than $30 billion on multiple days in 2022 and shed $840 billion this year alone. It’s hard to compare this company to what it was back then.

Jeff Bezos spent 27 years at Amazon and has been gone for less than two. In 2023 he pulls a Bob Iger and returns to steady the ship.

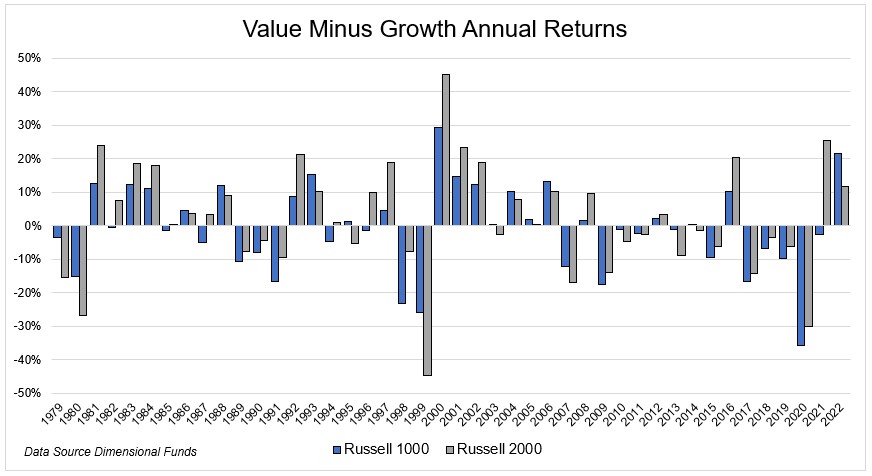

Value Outperforms Growth Again

After a decade plus in the doldrums, value stocks shined bright in 2022. I didn’t remember this, but small value dominated small growth in 2021, posting the biggest year or outperformance since the dot-com bubble burst.

While the outperformance of small value over small growth is near an all-time high, its large-cap brethren still have a ways to go. This trend continues into next year.

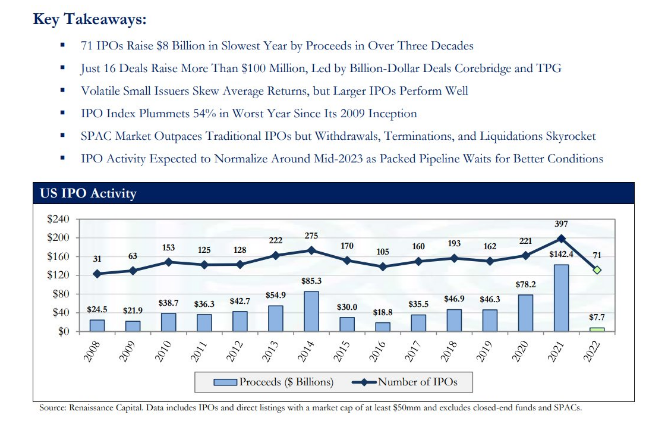

The IPO market remains frozen.

Only 37 companies went public in 2022, raising a paltry $7 billion. This is the weakest activity since the $4.3 billion raised in 1990 and a 94% collapse from the previous year.

There were fifteen tech IPOs that raised $1 billion in 2021. That number went to zero in 2022. That number will remain at zero in 2023. It’s hard to supply the market with risky assets when there is little appetite for risk.

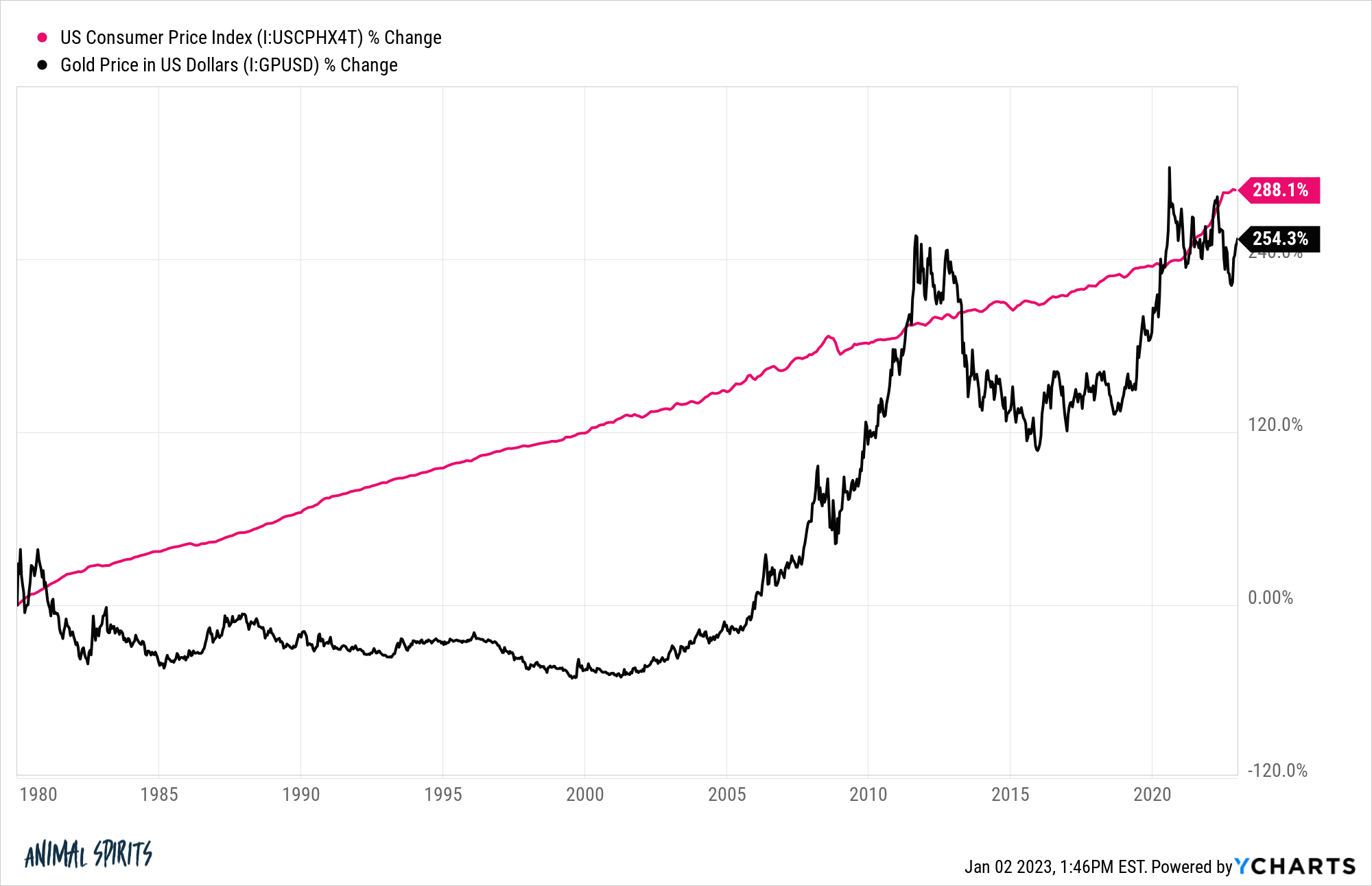

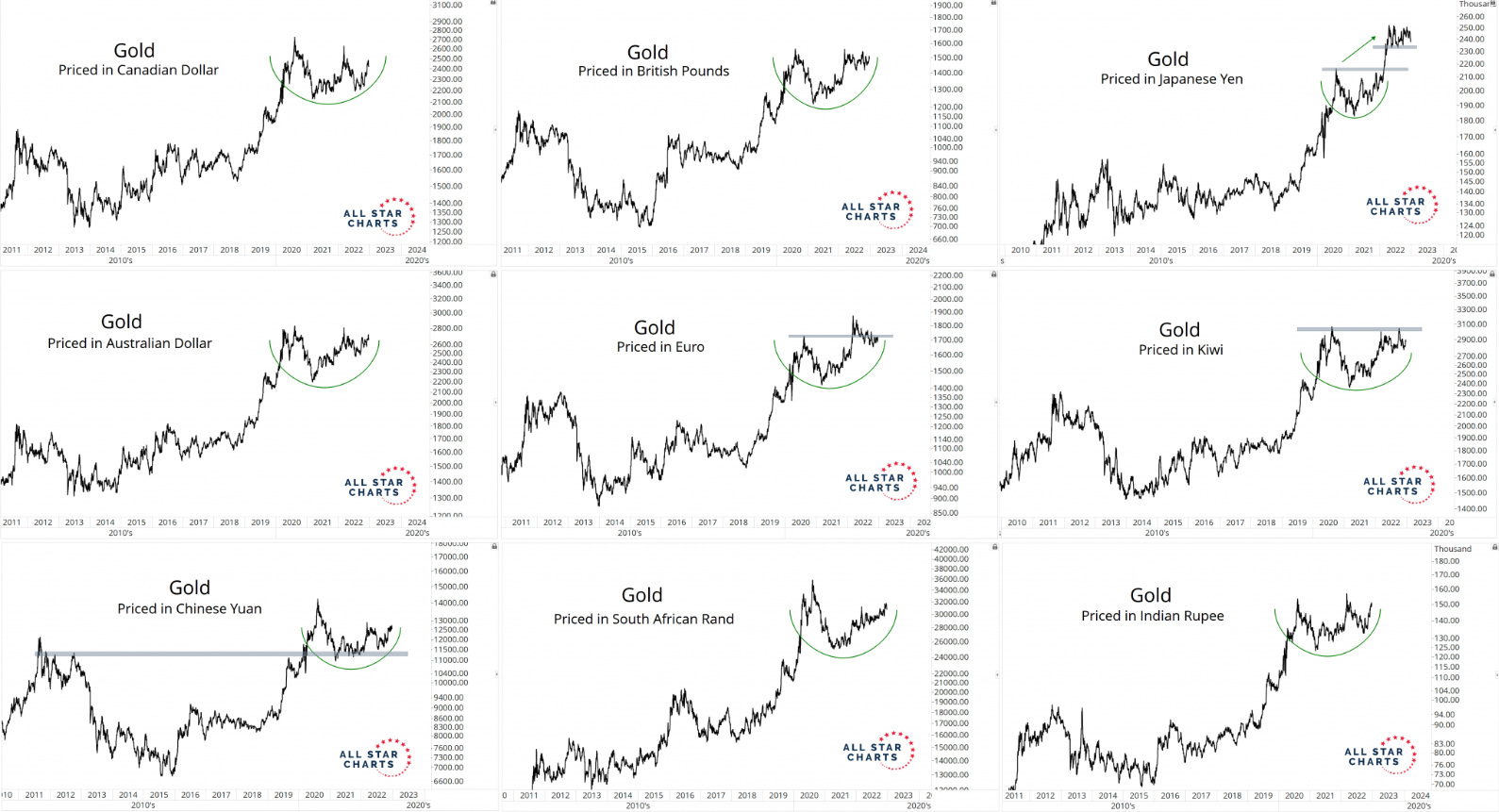

Gold makes a new all-time high

It’s hard to believe, but gold hasn’t outpaced inflation since 1980.

Real returns will stay below their peak, but nominal ones don’t. Gold breaks out and makes a new high in 2023.

Gold has been acting much better lately, ending 2022 at a six-month high. Gold has been disappointing during this inflationary environment, failing to keep pace with it since 2021. But that’s because gold is priced in dollars, and the U.S. dollar has been on a tear. If you look at gold versus other currencies, it looks even better. These killer charts from JC paint a clear picture of where the trend is.

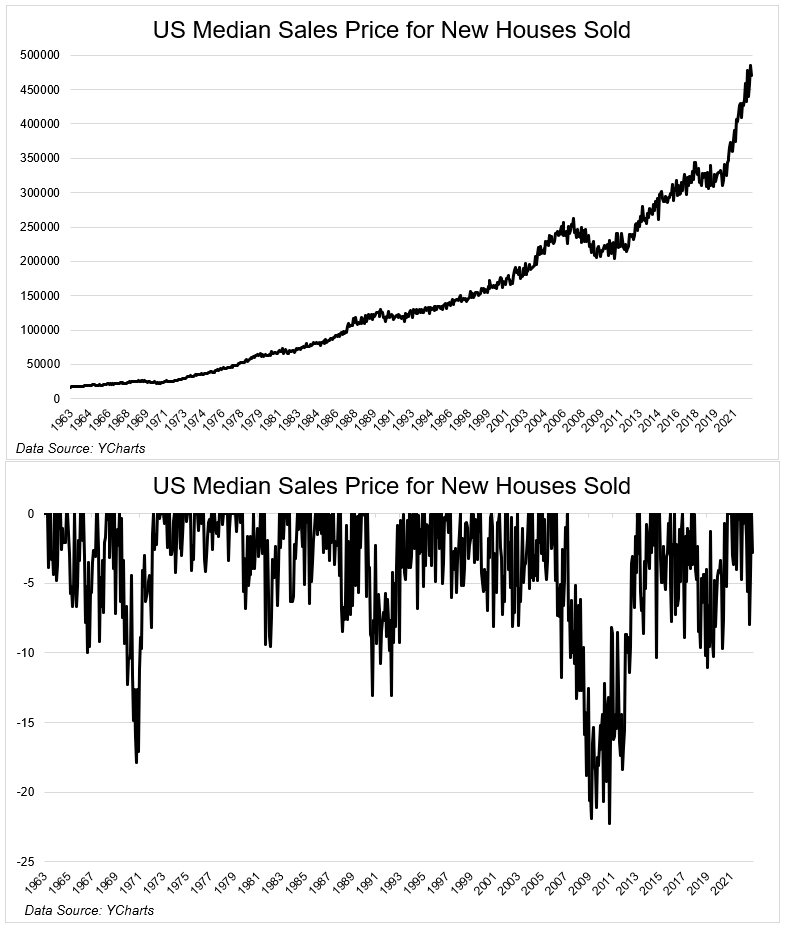

The Housing Market Doesn’t Crash

It would be easy to suggest that a massive decline in home prices is underway. After all, for new home sales to return to their average price in 2019, you’re talking about a 32% decline, which would be deeper than what we saw during the Great Financial Crisis.

But I don’t see that happening. The supply-demand imbalance is structural, with buyers outnumbering sellers by a lot. You see activity picking back up as interest rates have come in over the past couple of weeks. As long as rates don’t shoot back up to 7%, home prices will cool, but they won’t crash.

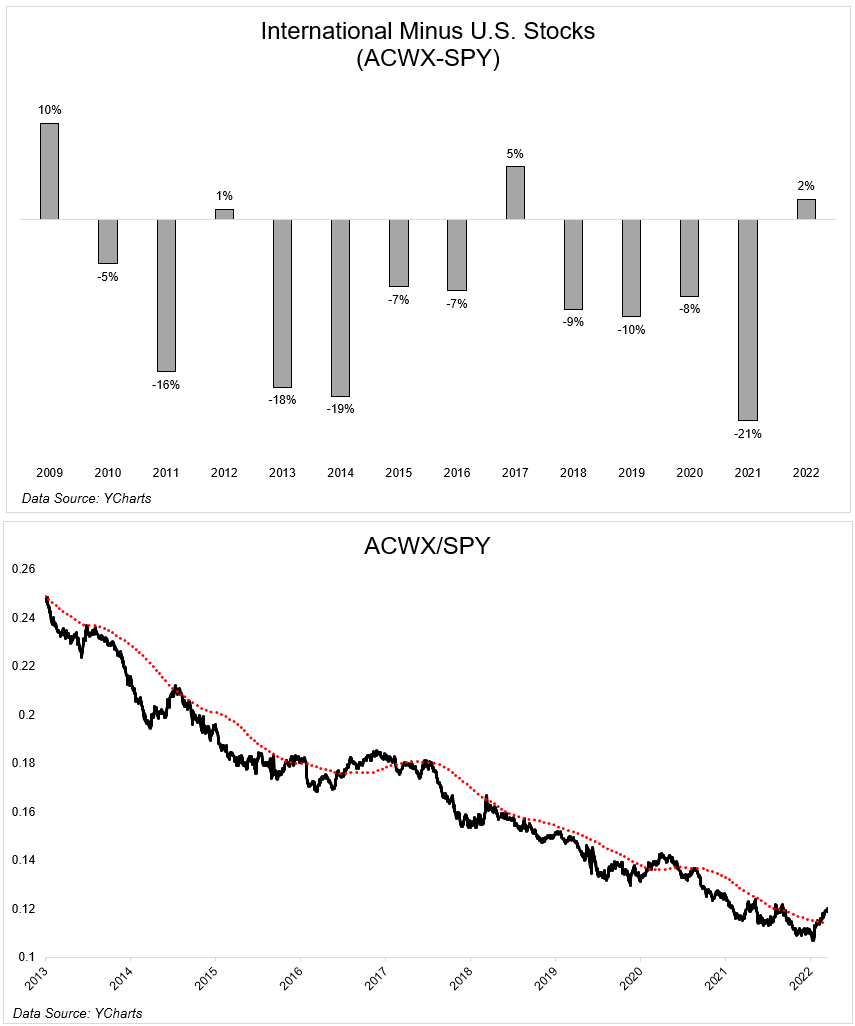

International Stocks Outperform

Diversifying away from U.S. stocks has been very painful for a long time. The S&P 500 has outperformed international stocks (ACWX) by 52% over the last five years and 160% over the last ten.

This might surprise you, but the S&P 500 actually underperformed most of the rest of the world last year, at least in local currencies. But when you include the wrecking ball that was the dollar, the gap shrunk dramatically and reversed in some cases.

The S&P 500 has outperformed for eight of the last ten years. But with the dollar well off its highs and the more value-oriented (less tech-heavy) makeup of international stocks, look for them to have their best year relative to the S&P 500 since 2009.

Technically, international stocks are starting to look better as well. The chart below shows that the ACWX/SPY ratio is further above its 200-day moving average than at any point over the last decade.

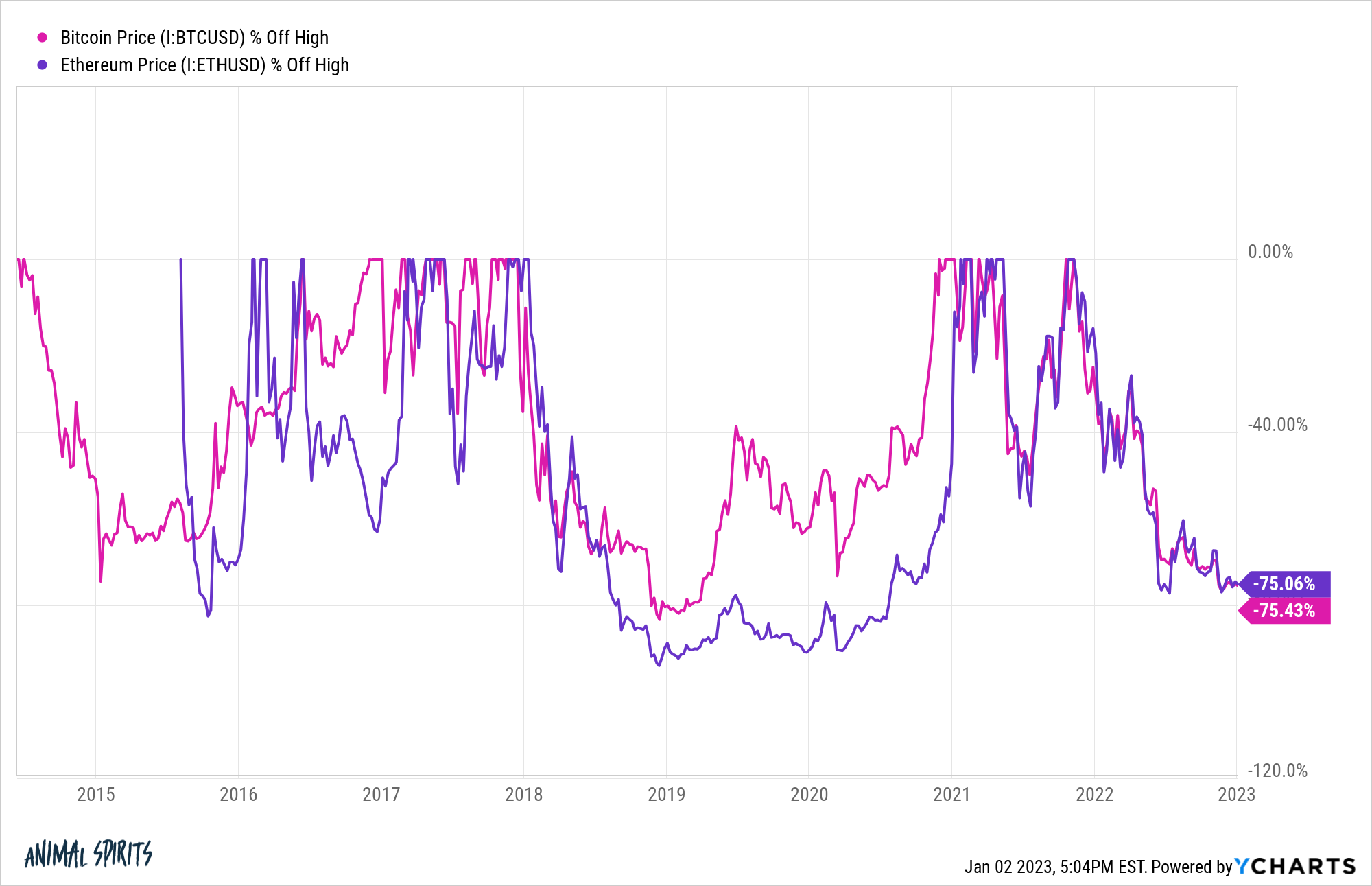

Crypto doubles in 2023

It’s hard to make the bull case for an asset class that feels like it comes with career risk. With all the negativity surrounding the space right now, I’m amazed that Bitcoin isn’t below 10k right now. And maybe that’s what the bulls can hang their hat/hopes on.

Bulls will say that we’ve been here before. Looking at the drawdown chart, yea, prices have seen these types of declines before.

But in every other decline, crypto was just a fringe asset. It still is, but you know what I mean. Like only crypto natives experienced previous drawdowns. So this time is extremely different because buyers who entered during the most recent bull run have been wiped out and, in many cases, will never return.

Crypto is an asset that is based on belief and faith, and they’re both at an all-time low. So how do you recreate a hype cycle after what we just saw? And with the overhang of whatever is happening with DCG and the questions surrounding Binance, it’s hard to be bullish right here. Especially with the fed continuing to remove liquidity from the system. Right now crypto is little more than a high beta asset on steroids. Wait, did I predict that crytpo will get cut in half again, because that’s what this is sounding like. Exactly!

No but for real, this seems like the most improbable prediction on this list and one that few are positioned for. Crypto will double in 2023.

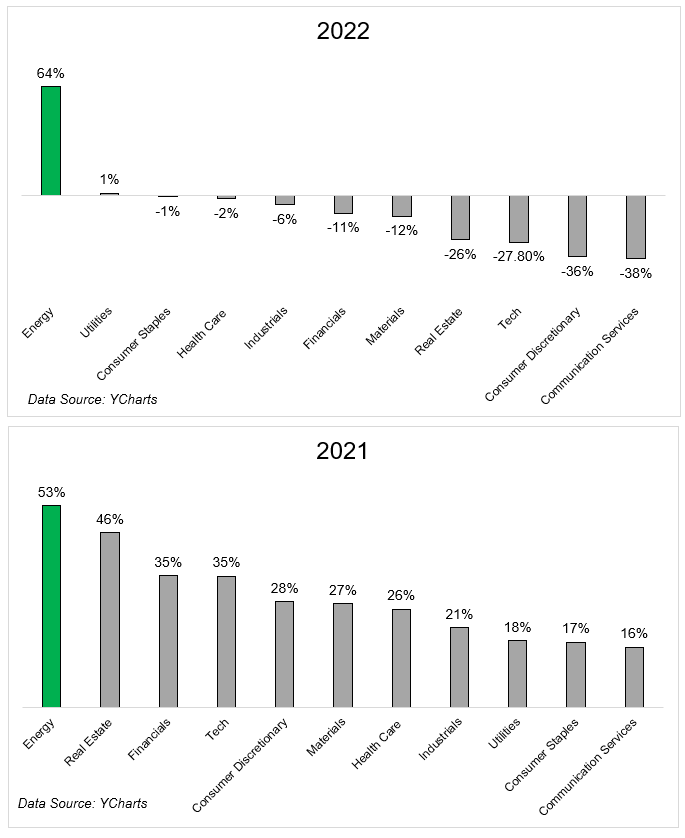

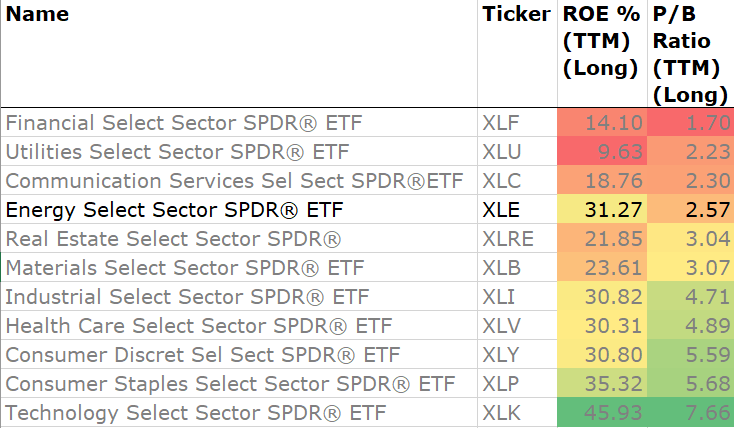

Energy stocks continue to outperform

Energy will be the first sector to threepeat since health care in 1989-1991.

Despite the impressive run, Daniel Sotiroff shared this chart showing that energy stocks are not only highly profitable but they’re also very cheap.

Energy stocks, which fell below 2% of the overall market at their lows, will finish 2023 north of 7% (5.2% currently).

Bonus. The market avoids a recession, and stocks gain double digits.

2023 will be very much like 2022 in the sense that macro will dominate. The biggest risk is hiding in plain sight, and it’s the fed over tightening into a softening economy. With peak inflation hopefully behind us, a consumer that is still in good shape, and an investor class that is negative across the board, it wouldn’t take much in the way of an upside surprise for stocks to take off.

Predictions are only silly if you take them seriously. Especially if you take your own predictions seriously. These are my best guesses as to what happens in the next year, and I look forward to rereading them in twelve months in disbelief that I could be so wrong on so many things. I hope everybody has a happy, healthy, safe, and prosperous new year.