What would happen if stocks crash? What would that do to people’s retirement plans? How would that change the way young people think about stocks? And what would it do to our country?

The cyclically adjusted price-to-earnings ratio now reads 30 for just the third time ever. The two previous times it printed a three handle, not only were future returns lower, but they preceded major market tops that would define a generation of investors.

The chart below shows the CAPE ratio and the S&P 500 (log). This visual tells a lot of stories, but for the purposes of this exercise, I want to focus on the two previous valuation spikes in red, which were followed by two stock market crashes in gray.

The CAPE ratio is great for setting return expectations, but it’s terrible at anticipating the end of a bull market. For example, the CAPE passed 30 in June of 1997 and would ultimately peak at 43.5, two and a half years later. Over that time, the S&P 500 gained 84% (TR) and the NASDAQ Composite gained 228%!

The most reasonable statement one can make regarding the CAPE ratio at 30 is that we should expect lower future returns. And if we’ve learned anything over the last few years, it’s that expected returns do not equal realized returns, and expensive markets don’t have to crash in order to reach some sort of equilibrium. After all, it’s not as if there are 350 instances when the indicator hit 30 and 350 crashes followed. There were only two. Now three. The jury is still out.

Following the election and the rapid acceleration of stocks, a friend of mine took his 401(k) to cash. I have two other friends who recently purchased homes which they’re renting out. They both expect they’ll get a better return from their real estate than they would in the stock market. These are anecdotal observations, but the chart below confirms that Millennials aren’t too enamored with equities. And this is at all time highs. What would another sawing in half of stocks do to my generation? If 2000 was fool me once and 2008 was fool me twice, what would 2019 be? Would we ever trust the stock market again? Should we? Who would want to buy something that just got cut in half three times in twenty years?

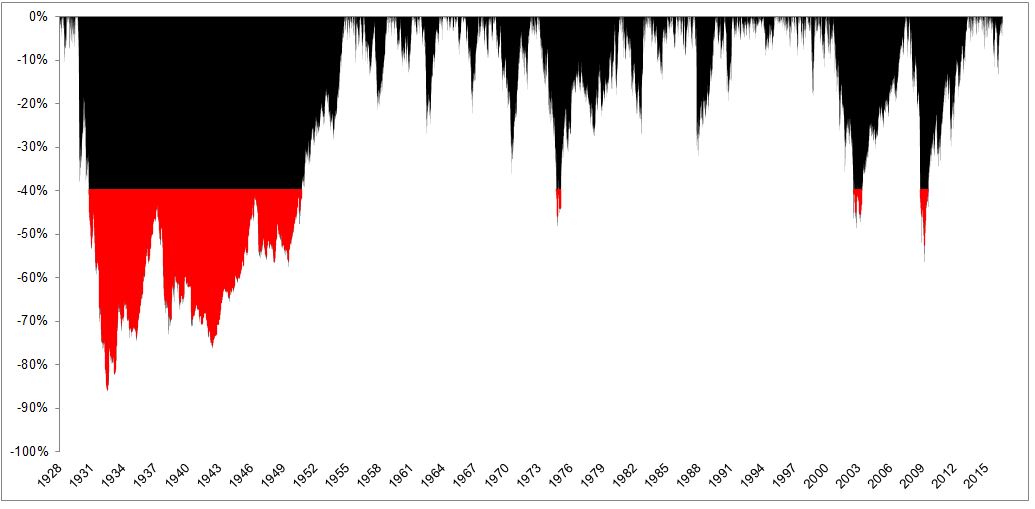

The United States has experienced just six distinct bear markets since The Great Depression: 1929, 1937, 1969, 1973, 2000, and 2008. The chart below shows the instances when stocks were in a 40% drawdown. To see a third crash in two decades would be unprecedented. But the fact that something hasn’t happened tells us very little about what can happen. Political scientist Scott Sagan has the perfect line to address the sort of thinking that prevents us from using our imagination: “Things that have never happened before happen all the time.”

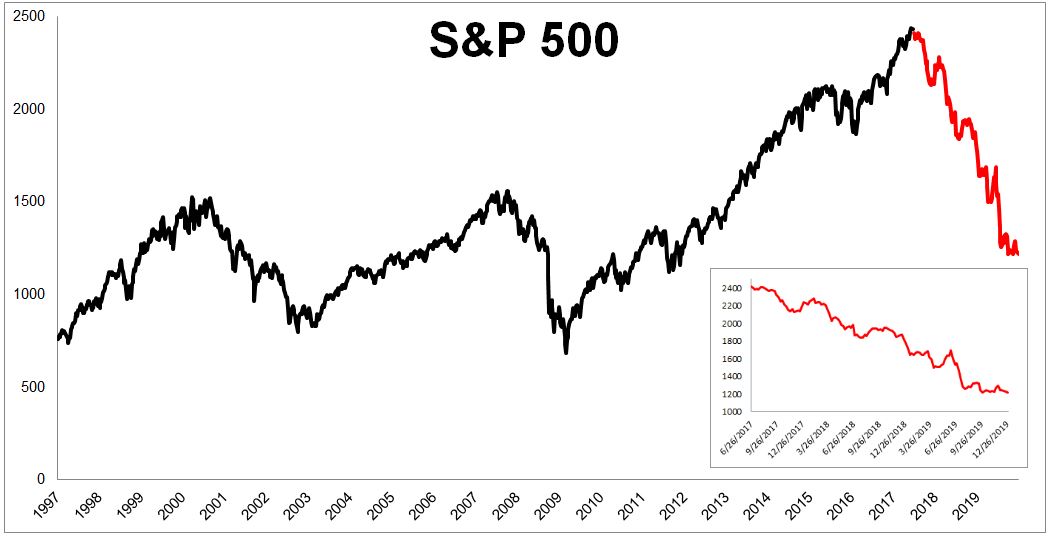

Thinking about stocks getting cut in half is an abstract exercise, so to make it a little more real I created this chart, which shows a 50% decline between today and 2019.

Entering these numbers was an uncomfortable experience. And if just charting a fictional 50% decline made my stomach churn, how will I behave when real money is on the line?

I’m 32 years old. I hope to be investing and remain invested for the next fifty years. I have a long time horizon and I understand how risk works.

But am I fooling myself into thinking I can swallow a 50% drawdown? Am I being too cavalier? Am I complacent? Am I the herd?

I think I’ve put myself in a position to endure a severe market downturn without bailing at the worst possible moment. But I’m also not naive enough to think that’s not a possibility. People much wiser and smarter than me have thought the same, only to have discovered they weren’t as mentally strong as they had previously thought. When the time comes, I’ll remind myself of what Morgan Housel said, “Every past market crash looks like an opportunity, but every future market crash looks like a risk.”

We’ve already experienced two market crashes in the twenty-first century, which is why some people feel that the next bear market will look like the previous two episodes. And while a third crash is 100% possible, I don’t think it’s probable.

Investors always have to be prepared for the nightmare scenario, but let me be perfectly clear. If we are in a stock market bubble, I don’t see it. And I promise I won’t use this post as an “I warned you” if stocks crash. But if this shook you a little, good. As I’ve said before, the time to prepare your portfolio for a storm is before it arrives, not after.