It’s been a mixed bag for factor investors. I suspect this is always the case.

The chart below shows some of the most common factors: value, min vol, momentum, quality, and dividends (I used all iShares products ).

It’s interesting that the two factors that outperformed since July 2013 (earliest common inception date), are min vol and momentum. These are two strategies that rely on past performance and have little to do with fundamental factors like earnings growth or value or anything to do with the underlying business.

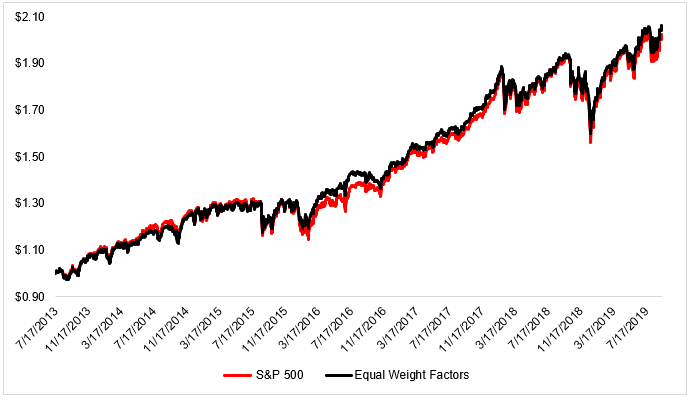

Some factors have done better, others far worse, but an investor that built an equal-weight portfolio of these five factors would have performed slightly better than the market…

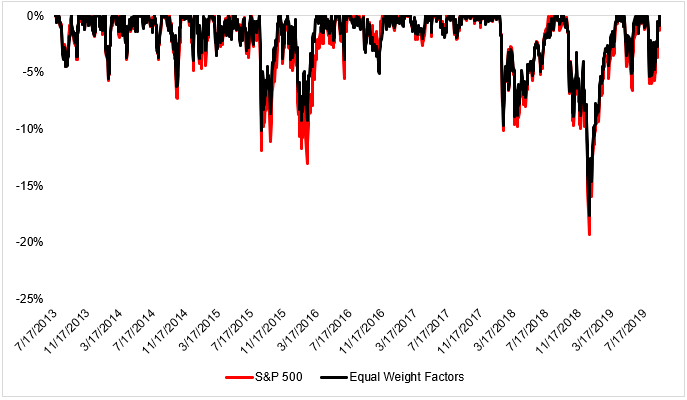

…With a more attractive drawdown profile.

Some will look at these charts and conclude that you should pick the factors you’re most confident in. Some will look for a way to time them. Others will look at these charts and ask, “why bother?” I firmly believe you should do whatever you want.

In the 90s, people would invest in mutual funds and hope for the best. Now investors know, or can know if they do some research, exactly what they’re getting. Transforming alpha into explainable beta at rock-bottom prices has been one of the better developments over the last couple of years in the ETF space.

Michael Batnick is a managing partner at Ritholtz Wealth Management. He is the co-host of Animal Spirits, What Are Your Thoughts, and The Compound and Friends. For disclosure information please see here.

Get a Full Investor Curriculum: Join The Book List

Every month you'll receive 3-4 book suggestions--chosen by hand from more than 1,000 books. You'll also receive an extensive curriculum (books, articles, papers, videos) in PDF form right away.