Investors tend to over-extrapolate. I’ll use myself as an example.

One of my ten predictions for 2023 was that energy would be the first sector to lead the pack for three consecutive years since utilities did in the late 80s.

¯\_(ツ)_/¯

Not only did this not come true, but the opposite is happening. Energy is the second-worst performing sector YTD. Energy isn’t the only thing that bears no resemblance to the prior year. 2023 is laden with extreme turnarounds.

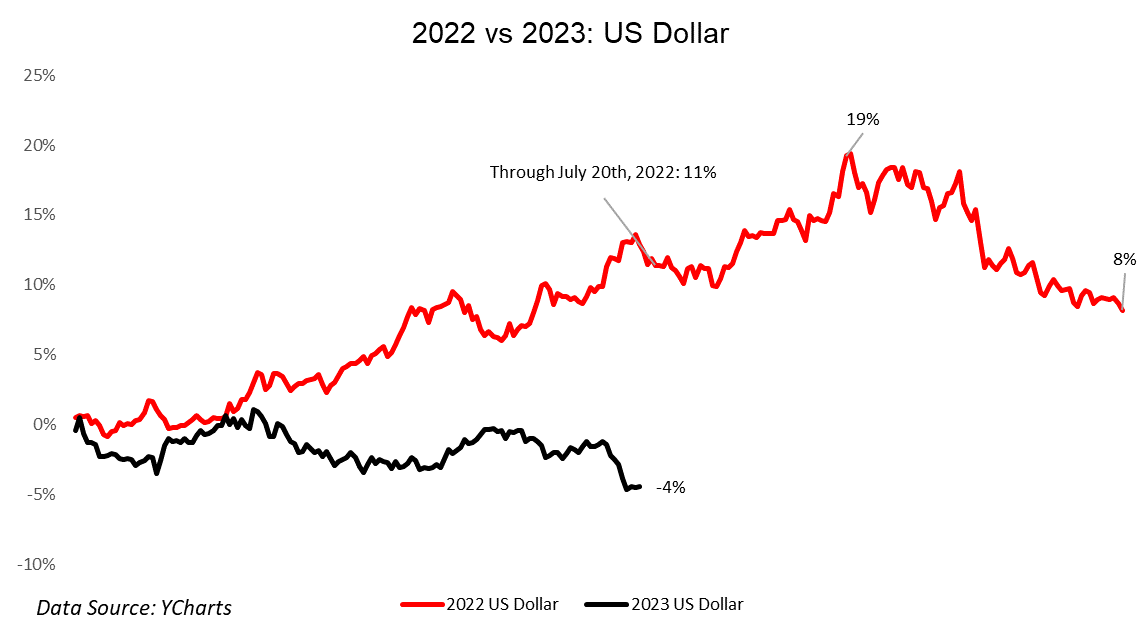

The U.S. dollar was a wrecking ball in 2022 as money flowed into the safest of safe havens. This is more of a risk-on year, and the dollar is going the other way. I’s currently down 4% on the year.

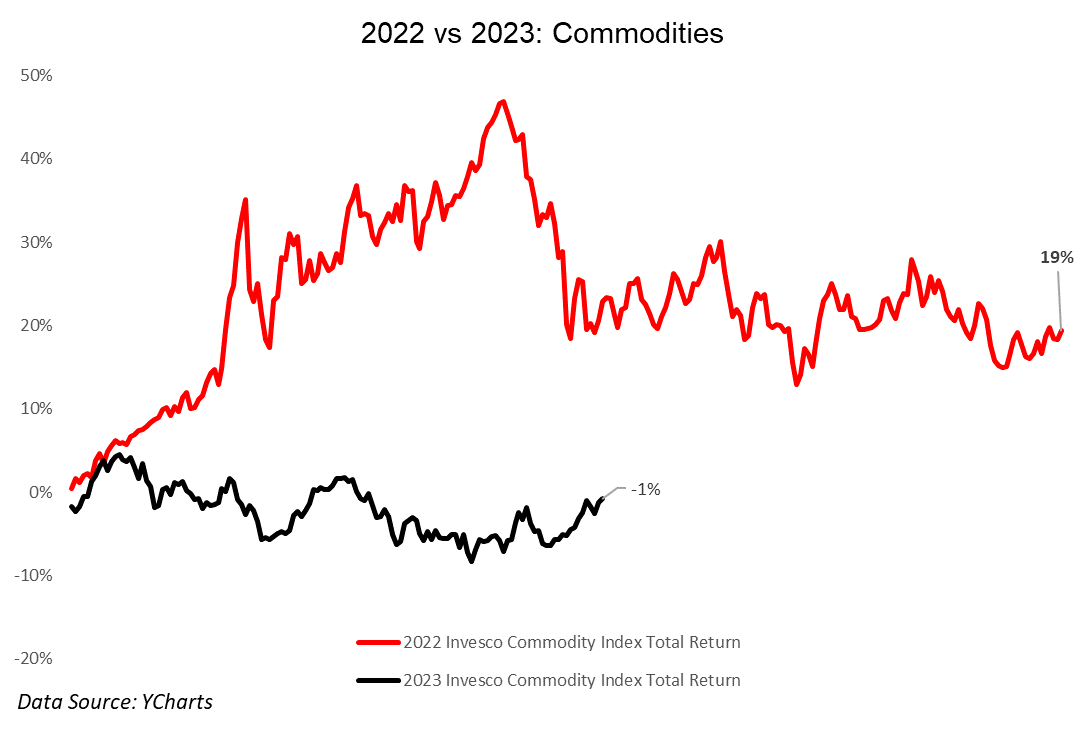

Global commodity prices soared in 2022 when Russia invaded Ukraine. That is unwinding and then some. The asset class has fully round-tripped.

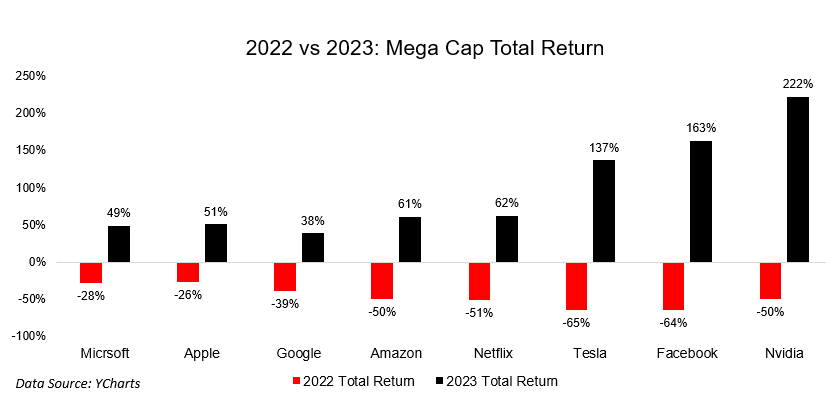

Interest rates and inflation killed growth stocks last year. Interest rates haven’t reversed, but the performance of growth stocks has. There is plenty of room for debate as to why this is happening, but the numbers are what they are. The mega-cap tech stocks are undoing much of the damage done in 2022.

Value stocks were the darling of last year. Growth stocks got killed, and they were flat. This year is the exact opposite.

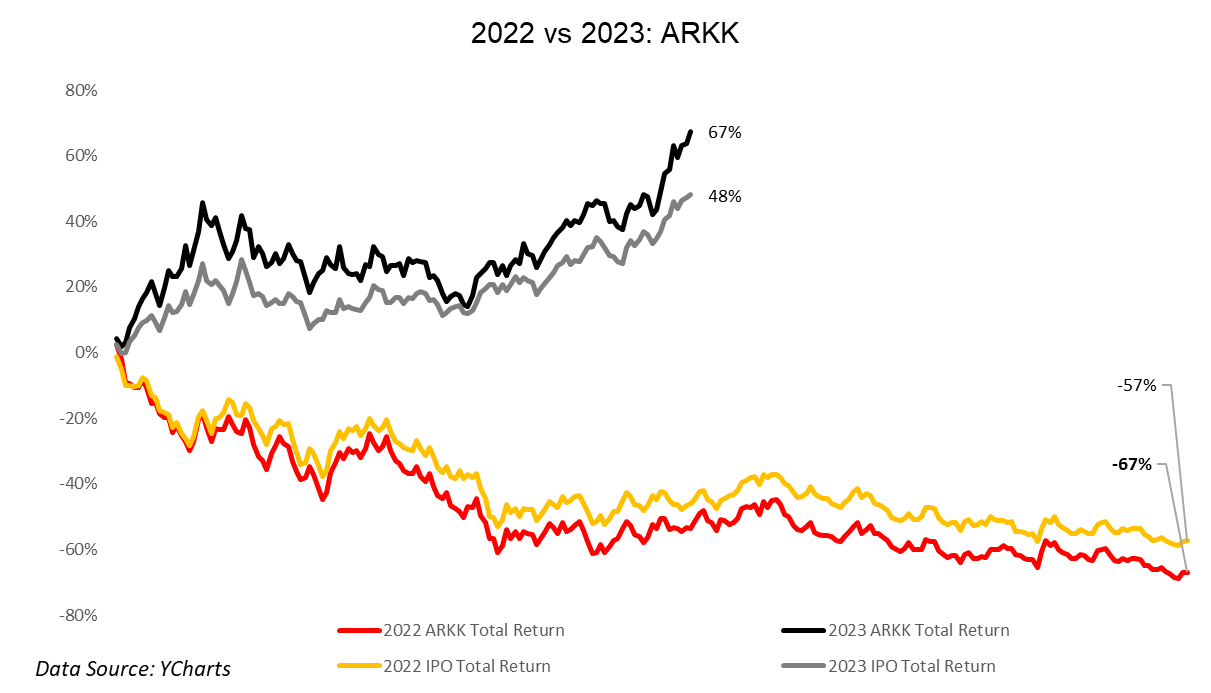

You’re seeing the same story play out in some of the most busted up names of 2022, IPO and ARKK. Their turnarounds are remarkable.

It’s normal to think that what’s happening today will happen tomorrow and the day after. Trends can and do last longer than you might think, but once they turn, it’s easy to be caught off guard. If you’re buying and selling individual names and sectors, remember that past performance is no guarantee of future results.

Michael Batnick is a managing partner at Ritholtz Wealth Management. He is the co-host of Animal Spirits, What Are Your Thoughts, and The Compound and Friends. For disclosure information please see here.

Get a Full Investor Curriculum: Join The Book List

Every month you'll receive 3-4 book suggestions--chosen by hand from more than 1,000 books. You'll also receive an extensive curriculum (books, articles, papers, videos) in PDF form right away.