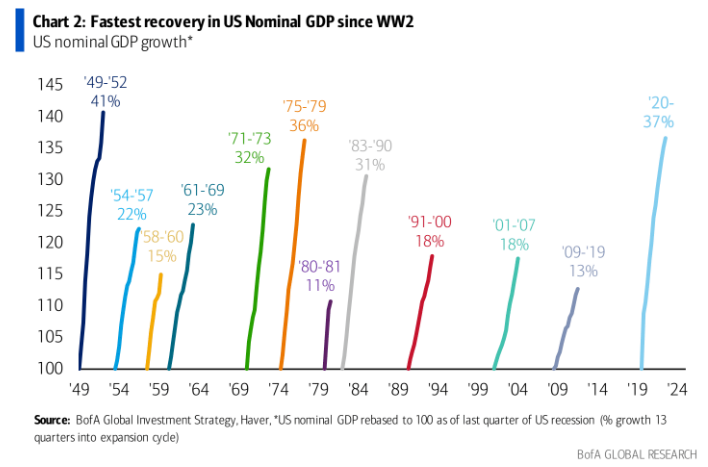

The nominal recovery in GDP since the pandemic recession has surprised almost everyone. We just experienced the strongest economic recovery since the end of World War II.

Last October when the stock market bottomed, 60% of economists expected a recession in the next twelve months. They were following the standard playbook of inflation up, rates up, asset prices down, and economic activity down.

Not even twelve months later, and nobody is talking about a recession anymore.

The first chart in this post showed nominal GDP growth, which you are rightly thinking, “show me real numbers. Strip out inflation, and how much growth is there really?” I’m glad you asked.

The Atlanta Fed GDPNow estimates that capital “R” real GDP will be 5% for the third quarter.

These estimates aren’t perfect, but they’re not terrible either, with an absolute error of 0.83 percentage points.

So how did everyone, from economists to CFOs, hedge fund managers to individual investors, get things so wrong?

There are two main reasons*, and they both boil down to the same point; higher interest rates aren’t impacting corporations or consumers as much as we feared.

The fed could have hiked til kingdom come, and they did, but it doesn’t matter what rates are today if you already locked in rates when they were low. And that’s exactly what corporations did during the pandemic.

Even with fed funds at the highest level it’s been in 20 years, corporate net interest costs are at a 60-year low.

With input prices (inflation) falling, companies were able to preserve their margins and more importantly, preserve their employees. And without layoffs, you can’t really have a recession. Which brings me to the consumer.

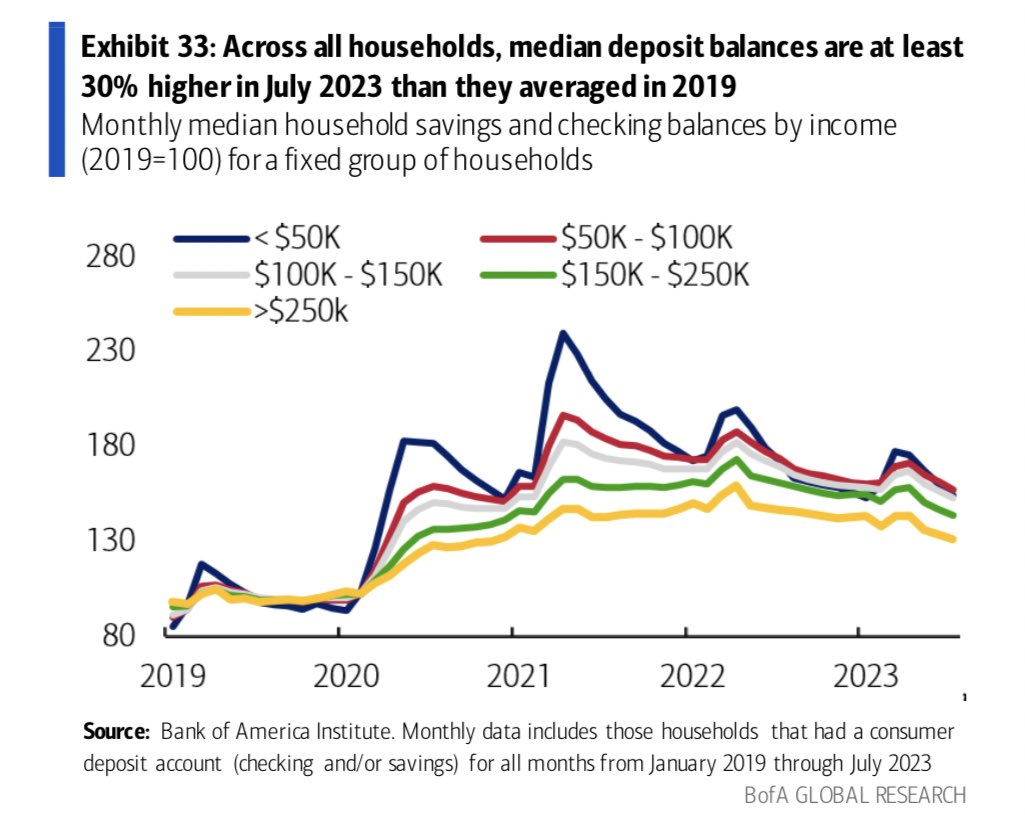

We learned this morning that retail sales grew at a 0.7% clip, well above the 0.4% expected reading. I think many of us underestimated how long it would take for the excess savings to burn off. All of that stimulus which was largely responsible for inflation is paradoxically keeping us out of a recession. People are still spending.

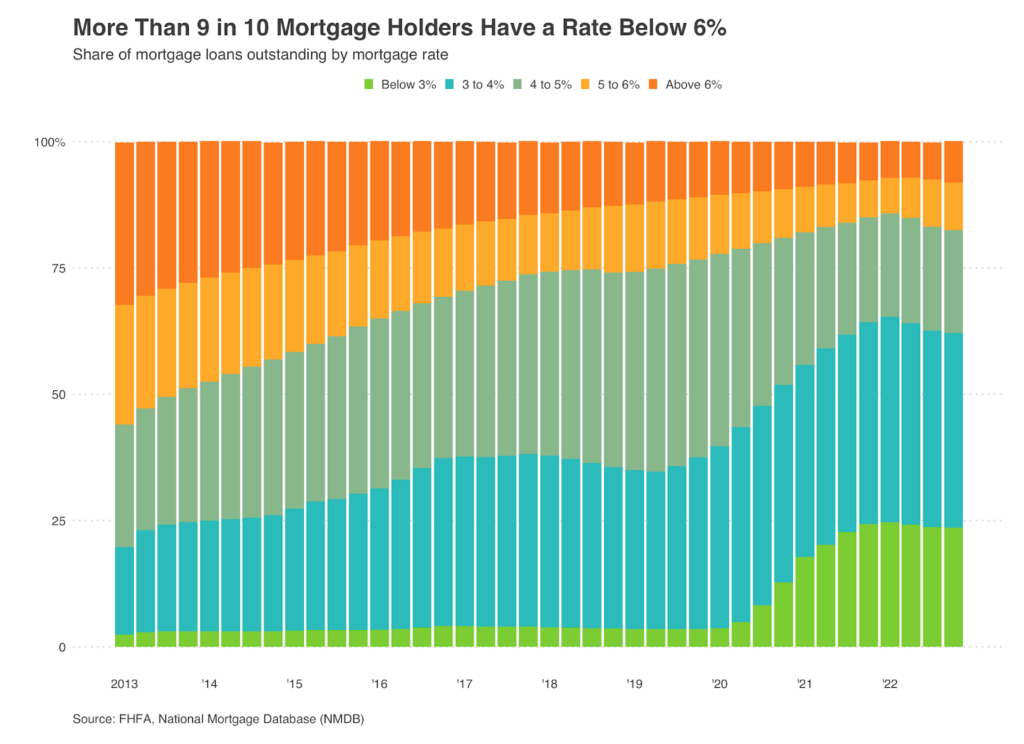

And it’s not just corporations that locked in low-interest rates. Consumers did too. 82% of homeowners have a mortgage rate below 5%.

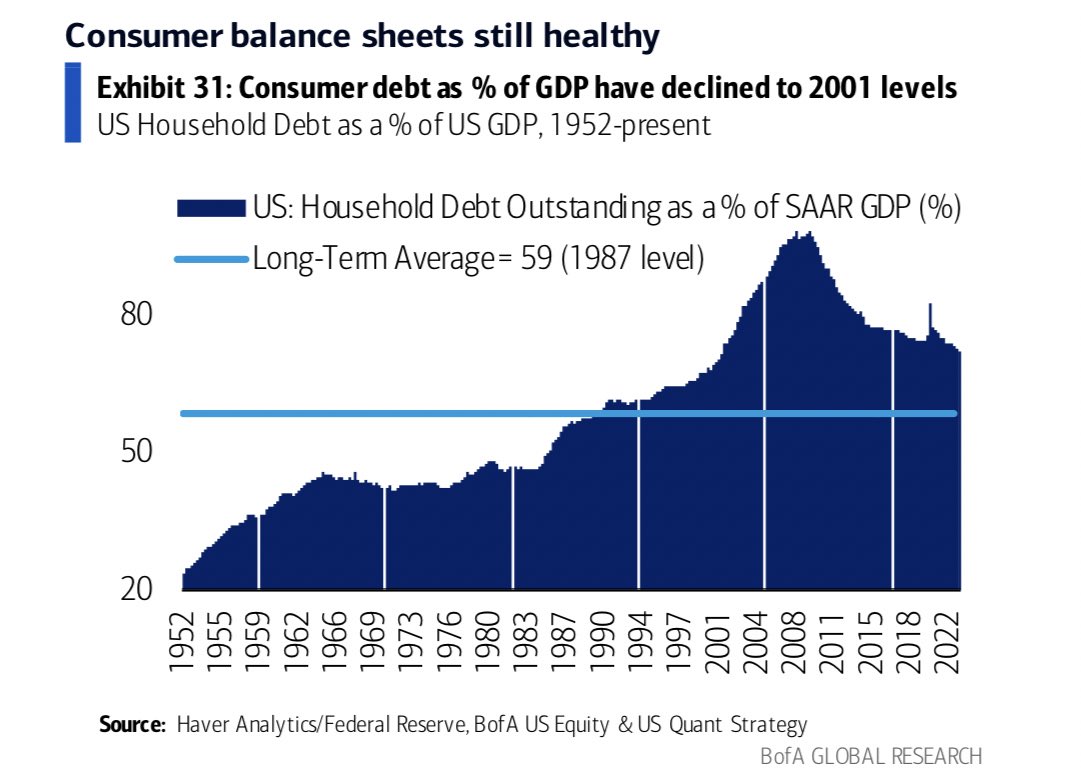

And because homes are most people’s biggest asset, and liability, household debt as a percentage of GDP is at the lowest levels since 2001! All while the fed is aggressively raising rates!!!

And so there you have it**. Higher interest rates were supposed to tank the economy, except this here economy isn’t nearly as exposed to higher interest rates as everybody thought.***

*There are a million reasons why we didn’t go into a recession.

** I know it’s more complicated than that

***I am not making a forecast, or saying that higher rates won’t eventually matter. The point of this post was to explain how we got to where we are today